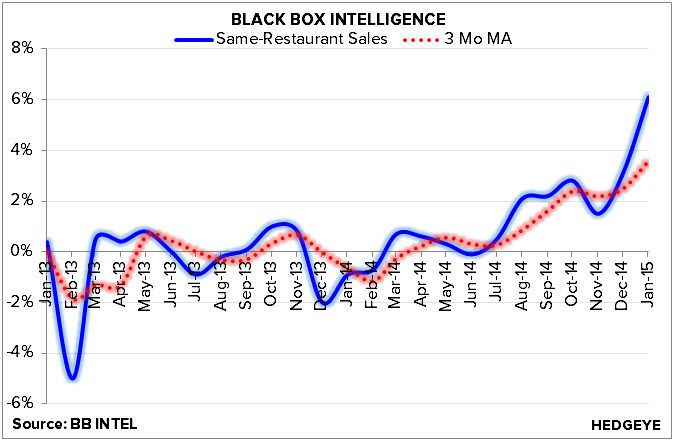

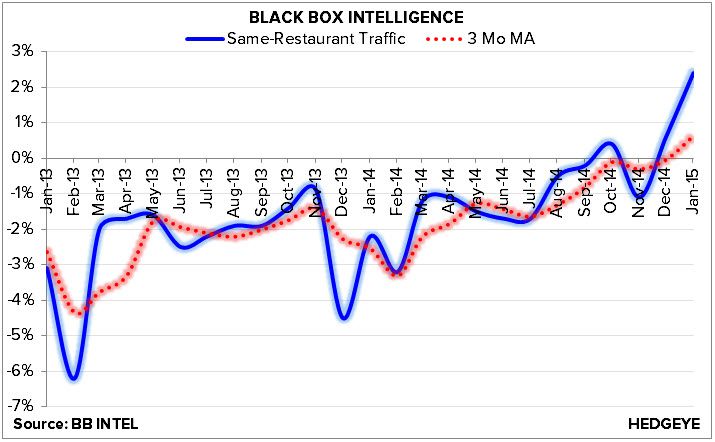

Black Box reported January results that were the strongest in over six years. While the majority of this strength is being attributed to a mild winter compared to a year ago, the underlying trends suggest a marked improvement across the industry. Easy comparisons through February should keep restaurant stocks, particularly fast casual concepts, afloat barring any dismal earnings results. But, with the data this strong, we expect management teams to have a very upbeat outlook for 2015 – despite some inflationary pressures on their cost of sales and labor lines. All told, expectations for the year will be high, which means the opportunity to create alpha will widen when sales trends reverse (tough comparisons in 2H15).

Restaurant same-store sales increased +6.1% as traffic increased +2.4% during the month. These numbers were up 300 bps and 180 bps, respectively, on an absolute sequential basis and up 210 bps each on a two-year average sequential basis.

A number of things (stronger traffic, lower gas prices, higher consumer confidence) has given management teams the confidence to take pricing recently and consumers the ability to increase their spend. To that extent, average weekly sales per restaurant increased +2.5% per restaurant over December 2014. This is important, considering the aforementioned pressures managers will face in 2015. Beef prices are expected to be the largest headwind on the commodity front, while ACA and pressure on staffing (accelerating wage and salary growth) will be headwinds on the labor front.

The extent to which restaurant sales remain strong will determine whether or not restaurants will be able to offset these pressures but, currently, there’s no denying the favorable outlook. We expect sales to continue to remain robust throughout February given the easy comparisons.