This note was originally published at 8am on January 23, 2015 for Hedgeye subscribers.

“I consider that all that I have learned of any value to be self-taught.”

-Darwin

I disagree with Darwin on that. In both my formal Ivory Tower econ education and my Wall Street experiences, I’ve found tremendous value in learning what not to do. Believing gravity-bending-linear-economists and their forecasts tops the list.

In markets and economies there are plenty of theories, but there are also realities. My self-teachings come from both books and Mr. Macro Market – not what some un-elected ideologue is trying to jam down my throat.

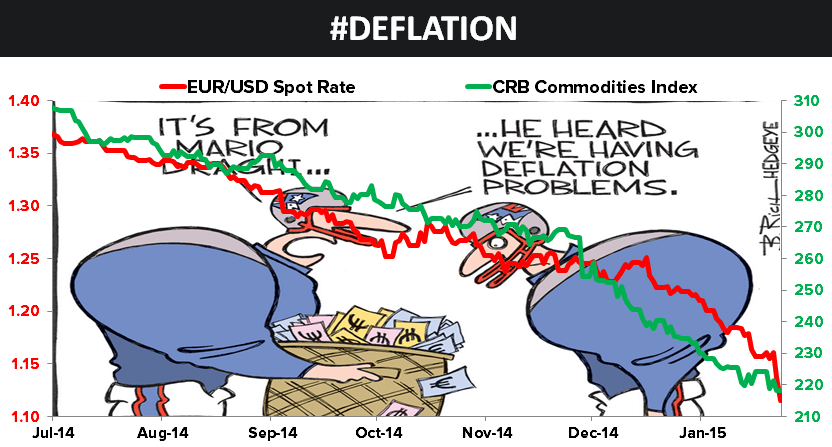

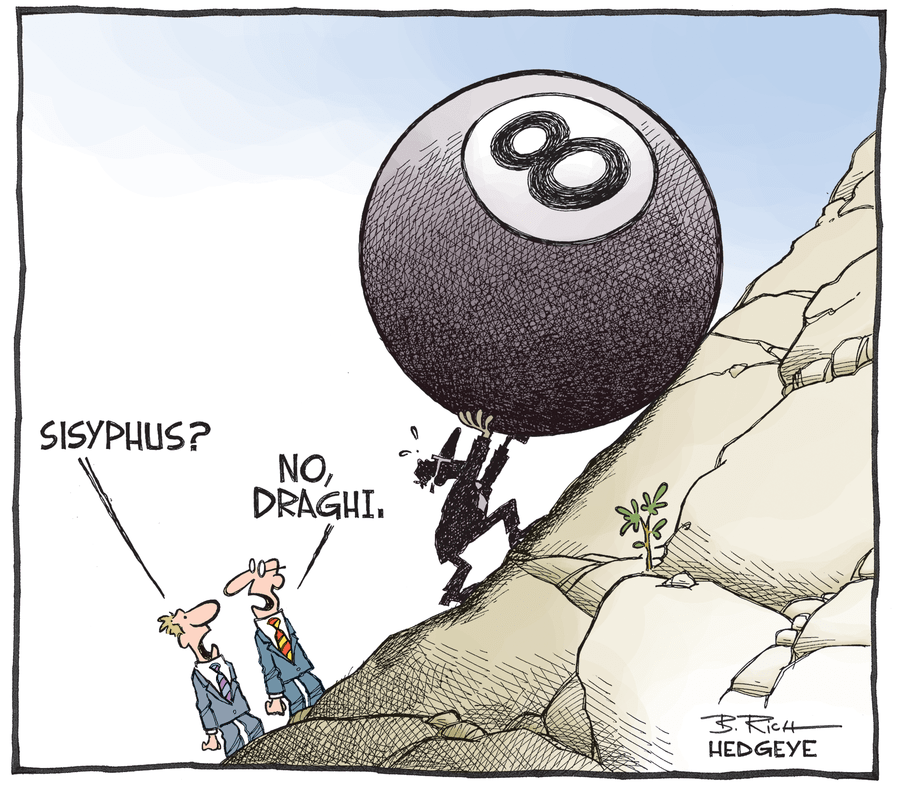

Pardon the terseness of that. I’m sick and in no mood to pander to what most financial media did yesterday as Mario Draghi provided 2008 like “shock and awe” to currency and equity markets, but only perpetuated #deflation risk in doing so.

Back to the Global Macro Grind…

As we learned in both 2008 and 2011, when central planners move into panic mode, they also perpetuate volatility, across asset classes. That’s mainly because they are trying to artificially inflate (centrally plan) asset prices higher.

In doing so, they open up what we call the risk of the market’s most probable range. What I’ve learned by doing over the course of the last 15yrs is that widening risk ranges tend to lead to rising volatility.

The only way to tone down volatility is for the output of the central plan to actually be believed. So that’s really your #1 risk management question this morning: do you believe that Draghi devaluing the Euro is going to deliver “price stability”?

What does Mr. Macro Market think?

- On the “news”, Euro’s burned to $1.12 vs USD, taking the US Dollar Index to multi-yr highs

- European equities ripped higher, making them some of the best YTD returns in Global Equities at +7-8%

- US Equities had a big up day (SPX 6th + day in the last 15), taking SPX and Russell to +0.2% and -1.2% YTD

- Commodities (CRB Index) deflated -1.3% on the “news”, hitting multi-yr lows

- US Equity Volatility sold off to higher-lows but held both TRADE and TREND duration support

In other words, if you are long France because the economy sucks, you’re killing it! The CAC 40 (France) is now beating the beloved SP500 by +800bps for 2015 YTD. Oh, and #deflation expectations only rose yesterday in the face of Draghi smirking.

When one of the few reporters with a spine questioned the sly Italian jobber on the actual economic impact of his decision to float a number (50B) to the media that he could beat by 10B, he did everything but answer the question.

Do you think a ramp in Belgian stocks to +7% YTD is going to improve the youth unemployment situation in Southern Europe? Or is the story now that crushing the purchasing power of Europeans is the new consumer spending catalyst?

In other European news this morning:

- France’s services PMI for JAN (oui, c’est le service economie, stupide) 49.5 vs 50.6 in DEC

- Germany’s flash PMI slowed again to 51.0 from 51.2

Get used to nothing. Unless it’s different this time, I don’t see Draghi delivering inflation or real economic growth.

Does anything in our Global Macro playbook change post yesterday’s central plan? Not really:

- BEST IDEA: Our best way to play global #GrowthSlowing and #Deflation = long the Long Bond (TLT, EDV, ZROZ, etc.)

- COMMODITIES: while I’m getting interested in Gold, I’ll keep our net allocation to that asset class at 0%

- CENTRALLY PLANNED EQUITY MARKETS: from this time/price, I’d rather buy Weimar Nikkei than Europe

- US EQUITY LONGS: stick with the long early cycle-consumption and yield chasing sectors (XLP, XLV, XLU, VNQ)

- US EQUITY SHORTS: stick with the late-cycle economic and #Deflation ideas (XLE, XLB, KRE, XLI)

Notwithstanding the 2-day ramp in European, US, and Japanese equity beta, the best vs. worst returns (highest absolute, with the lowest volatility = best kind of #alpha people pay for) remain glaring:

- YTD Winners: Healthcare (XLV) +4.3%, Utilities (XLU) +3.8%, Consumer Staples (XLP) +3.6%

- YTD Losers: Financials (XLF) -2.8%, Energy (XLE) -2.5%, Consumer Discretionary (XLY) -1.6%

Put another way, Mr. Macro Market’s self-teachings have set up for one of the best Global Macro investing environments for active managers (long and shorts – over-weights and under-weights) that I can remember.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.75-1.93%

SPX 1989-2066

VIX 16.05-23.03

EUR/USD 1.12-1.15

Oil (WTI) 44.82-49.06

Gold 1260-1323

Copper 2.48-2.61

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer