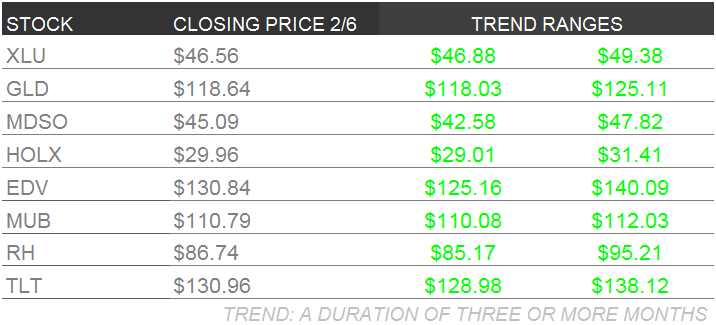

Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

Please note that we added Utilities (XLU) this week and removed Consumer Staples (XLP)

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

HOLX

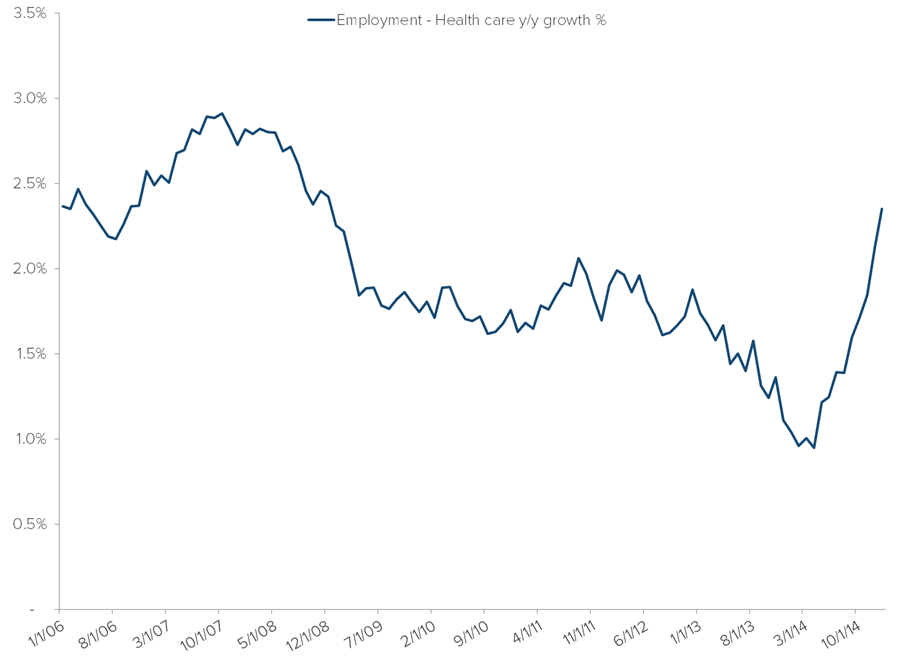

Patient volume in OB/GYN offices is off to a very solid start in January 2015. One of the important things HOLX said on their recent earnings call was that ThinPrep revenue was coming in flat year over year. Physicians continue to expand the interval between Pap tests for their patients, adhering to guidelines issued in 2012, and as a result the demand for ThinPrep (Pap Testing) testing continues to decline year over year. However, as we saw with HOLX, a solid quarter in patient volume, an exclusive deal with a large lab company, and market share gains overseas, can fill the hole pretty quickly as we saw in the quarter. HOLX managed to go from the declining ThinPrep sales they’ve seen for many quarters in a row to flat year over year growth, an important change in terms of how fast the company can grow in the years ahead. Most importantly, we’re bullish on the immediate opportunity for 3D Mammography, which can accelerate company growth overall much easier if the rest of the company can just hold steady.

Will the strong patient volume trend continue? The prospects certainly look good. Friday’s Employment Report from Labor Department showed solid job and wage growth overall, so the patients seem to be doing better. But also, the providers seem to be doing well too. In particular, the growth among healthcare professions continues look very good. If demand wasn’t good in the doctor’s office, we don’t think everyone from Chiropractors to Physician Offices to Hospitals would be hiring at an accelerating pace.

MDSO

Overview

MDSO came up short on our expectations for sales as one of our key drivers deviated materially from actual results. While that key metric failed us this quarter, other drivers related to customer growth and backlog remain on track. Despite not getting our "beat and squeeze", we are not changing our positive view on the company as underlying fundamentals remains in-tact.

Application Services Y/Y % ROC

key drivers

Competitive Wins & Customer Growth

We are encouraged by a recent competitive win that management described as having the potential "to be our second largest platform win". Additionally, 40% of deals in Q4 that were over $1 mill were done with companies below the top 50 pharma. This alleviates concerns over their ability to compete effectively in the small-mid size market given their premium pricing. These metrics also run counter to the short thesis we've heard most often, that Oracle was making competitive inroads after a long period of ceding share to MDSO.

Customer Y/Y %

Cross-sell

Customers using multiple products increased to 58% in Q4, with average product per customer ("intensity") of 2.5. This marks an increase from 49% in the prior period and is an important metric to track as cross-selling is critical to supporting long-term growth. Meanwhile, revenue retention among enterprise clients continues to be near 100%.

Product Per Customer

Backlog

We would highlight that management is now reporting an adjusted backlog figure that is inclusive of their estimates for intra-year renewals. In prior quarters, they reported backlog excluding intra-year renewals. Adjusting for this change, backlog growth was +12.9% y/y and below our model estimate. Deal timing impacted the backlog figure as the recent large competitive win was signed in January, as oppose to December. We anticipate an acceleration in backlog growth in 1Q15 as this deal gets rolled into the reported backlog figure.

Backlog Y/Y % ROC

Guidance

After a year of disappointment, a chastened management team may be incrementally conservative. Management is basing guidance on their adjusted backlog which does not include increases in ASPs and potential upsells. Adjusted backlog provides coverage for approximately 85% of the midpoint of '15 revenue guidance of $402 mill (vs. $409 mill consensus).

We find the following metrics as sign of positive momentum going into 2015:

- Annualized bookings in Q4 and full year were up 30% and 22%, respectively

- High proportion of deals greater than $5 million, up 33% y/y in 2014

- Overall transaction size increased by 17% y/y in 2014

- A platform deal and competitive takeaway with the potential to become the second largest deal in company history.

TLT | EDV | XLU | MUB

Punk’d By Late-Cycle Labor Market Strength

Follow the bouncing ball:

- Friday’s JAN U.S. employment report was really good – i.e. showing 2nd derivative improvement on nearly all key metrics, massive revisions to NOV and DEC data and besting the Bloomberg consensus estimate by 29k.

- The U.S. Dollar Index skyrockets nearly a full percent on the release.

- The 10yr Treasury note yield rips nearly +10bps on the release.

- Long-duration bonds (e.g. TLT, EDV and MUB) and bond-like proxies in the equity market (e.g. XLU) end the day deeply in the red.

The Frequentist view of interpreting the labor market won the day and crushed the week:

- TLT -5.3% WoW

- EDV -7.7% WoW

- MUB -1.2% WoW

- XLU -3.6% WoW

That said, however, the Bayesian view of interpreting the labor market is winning the year:

- TLT +4.0% YTD

- EDV +5.4% YTD

- MUB +0.4% YTD

- XLU -1.4% YTD

For context’s sake, those YTD returns compare to +0.00% return for the SPY.

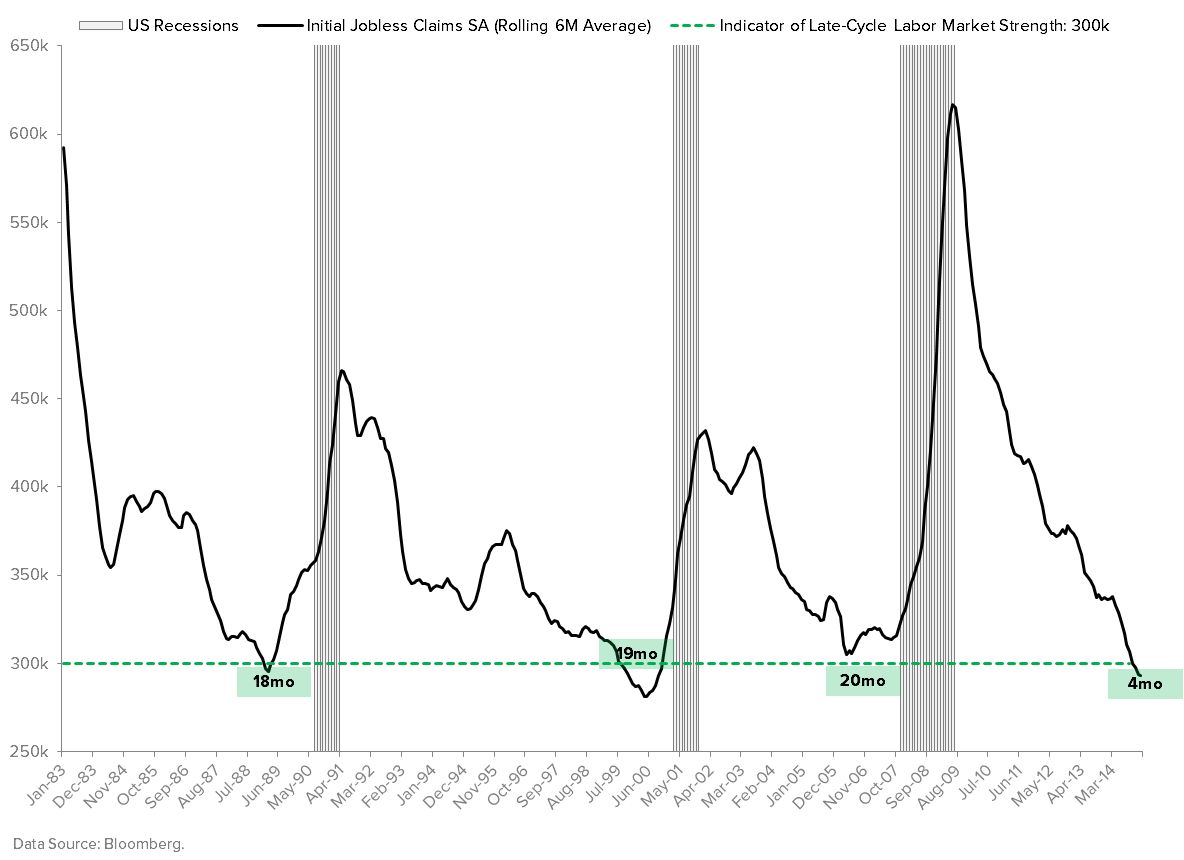

Based on the following chart, us Bayesians are very confident that we will eventually prove correct in our expectation for the labor cycle to negatively inflect and in our forecast for the 10yr Treasury yield to test its all-time lows. Once 300k is breached to the downside on a trending basis in Initial Jobless Claims, that’s as good as it gets for the U.S. labor market.

The question is, however, “How long can the good times roll?”

Frequentists continue to argue quite reasonably that the U.S. labor market – fully loaded with its ~140,000,000 employees – does not turn on a dime. As such, market-based Bayes factors are bound to overshoot any dour intermediate-term outlook for employment growth at various intervals throughout the topping process. That’s exactly what happened when 10yr Treasury yields closed at 1.64% last week.

As Lee Corso would put it, “Not so fast, my friend!”

Keeping with the Frequentist vs. Bayesian debate, Frequentists are likely to “win” the next 4-6 weeks heading into the March 18th FOMC meeting if the prevailing macro narrative has indeed shifted from one of DEC/Q4 #GrowthSlowing to Q1 #GrowthAccelerating – for now at least.

Stay tuned; long bond investors may continue to experience PnL volatility if the [potentially] bond-unfriendly portion of our #Quad414 theme continues to develop according to plan.

RH

For all people asking the question "Why is RH Pre-announcing?"

Here you go...

The company wants to let everyone know that business is a-ok. They are looking at a a comp of 24% compared to the Street at 19%. That translates to 24% sales growth -- the top end of the guided range. EPS is $1.00-$1.01 -- vs prior guide of $0.99-$1.01. All numbers are preliminary -- meaning that they're probably headed a bit higher.

RH is not reporting earnings until late March. The company knows from past experience that large windows of time without financial information given to the Street is rarely a good thing. They're trying to fix that. So, if you're caught off guard by the release...we see where you're coming from. But absolutely don't freak out. This is good news. The story is on track. And the catalyst calendar for 2015 will be explosive.

GLD

U.S. Dollar Down has driven massive counter-TREND moves embedded in macro Correlation Risk over the last few weeks.

This counter-TREND move that started last Wednesday post-Fed meeting provided a look at the big USD reversal risk with every data point. Our asset allocation recommendation has been positioned for a #QUAD4 deflationary slowdown, and we want to hedge that position through the volatile swings we’ve experienced since October.

After a sequential annualized GDP print of +2.6% for Q4 vs. consensus expectations of +3.0%, rates plunged to new YTD lows, and commodities ripped last Friday:

- CRB +2.9% on the day

- 10-Yr yield -11bps to 1.64%

With the tight negative correlations in the commodity space; AND, the existence in a peak multi-year net LONG position in US Dollars of +70,456 futures and options contracts (vs. the 1yr avg of +24,739), we want some exposure to weak dollar asset classes (GOLD) against our negatively correlated macro positions (TLT, XLU, UUP).

Market changes post-Friday’s payrolls number exemplified the necessity to have exposure on both sides of the coin which is why we want you long of GOLD:

- USD +1.10%

- 10-year Rates +11 bps

- Gold -2.5%

Despite the positive Non-farm payrolls report Friday the jobless claims chart below is self-explanatory as a late cycle indicator and suggest we are within 12-months of a recessionary turn. The big reversal in the dollar’s path last week is a wake-up call that big macro correlations in a volatile market are REAL.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

what does crude oil volatility mean to you?

Volatility in oil (and across asset classes for that matter) hit historic lows this summer at the highs in crude oil. The OVX index bottomed in June and reached its highest point yesterday since 2008.

INITIAL CLAIMS: CONCENTRATED HARM MEETS DIFFUSED BENEFIT

While the rest of the country benefits from lower gas prices, those in the energy sector are feeling the squeeze.