CMG remains on the Investment Ideas list as a long.

Recap

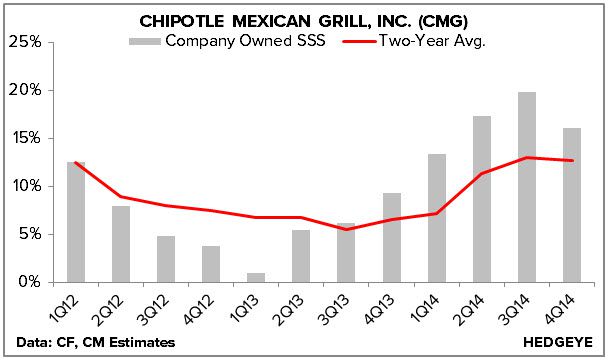

It’s unlikely for a restaurant stock to trade down after reporting same-store sales growth of +16.1% and a $0.05 (or 136 bps) bottom line beat – but that’s precisely what we have here. With a lofty valuation (41.5x NTM P/E; 21.41x NTM EV/EBITDA) and sky high expectations, Chipotle needed to deliver an impeccable quarter to appease the market.

Alas, in the market's eyes, margin pressure and some cautious commentary regarding 2015 same-store sales and cost of sales trends trumped the best in class comp and traffic growth. Cost of sales inflation, primarily due to beef, dairy, and avocado, pressured margins in the quarter and the guide for 2015 was well above consensus estimates (35% vs 34.3% est.) as beef and avocado prices are expected to remain elevated while dairy normalizes.

Management dismissed the notion that cost of sales is an issue as they tend to take a more holistic view of their operating model – as long as restaurant level margins are improving, they are pleased. As an aside, restaurant level margins improved 101 bps in 4Q14 even as cost of sales increased 108 bps. We firmly believe Chipotle should be praised rather than condemned for investing in its food, a phenomenon that the majority of its competitors are reluctant to do.

Source: Company Filings, Consensus Metrix

In our view, there were far more positives in the quarter than negatives and the street is overlooking the strategic investments the company made this year to further improve operating performance moving forward.

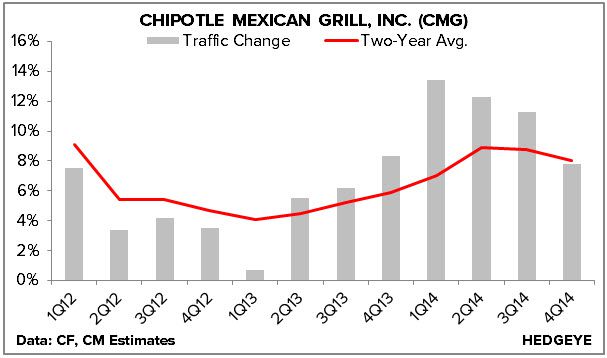

Comp growth was driven by 6.3% price, 2.0% mix, and 7.8% traffic. In addition, throughput picked up again, as CMG increased its peak hour lunch and dinner transactions by three and five, respectively. Its restaurants are now operating at AUVs close of ~$2.5 million, a number which management intends to improve through stronger operating efficiency. To that point, the company has decreased its field leadership ratio from 15 a few years ago to 8 today and has created its own Restaurateur diagnostic tool that helps these leaders identify weaknesses in each of the restaurants they supervise. With these two investments (people, diagnostic and plan tool) in place, 2015 should be a year of continued growth and development in each of Chipotle’s restaurants – better food, better throughput, better experience.

Considering CMG’s bullet proof balance sheet (nearly $1 billion in cash) and improving incremental returns (even at ~1,800 restaurants), it’d be foolish to bet against this stock. It is the best positioned growth company in our space.

Upshot

While we understand the market’s initial reaction to the report, we believe it is important to look past the short-term noise and volatility that sometimes plagues this stock around earnings releases. What’s most important to us is that Chipotle’s brand positioning and relevance has never been stronger. This is not only evidenced by the company’s same-store sales growth, traffic growth, and all time high AUVs, but also by the ever evolving preferences of American eaters. Chairman and Co-CEO, Steve Ells, shed light on this early on in the call:

“For example, our vision is really resonating with teens, millennials, and Generation X. According to industry research, Chipotle is one of the most popular restaurant chains among teens and has been growing in popularity among this demographic. This report from 2014 ranks Chipotle as the third most popular brand among teens, up from number eight in 2013. Gen X consumers were 33% more likely than average to choose Chipotle, with millennials Chipotle was even more popular. With customers in this group 75% more likely than average to choose Chipotle over other restaurants.

We believe that our popularity among these younger consumers is tied to our vision and the growing interest in issues related to food and how it is raised. Our own research shows that these issues are clearly becoming more relevant and important when customers choose where they will dine. Based on our ongoing tracking research, 87% of fast casual diners say they prefer to eat foods that are grown locally, up from 70% in 2011. 86% believe ingredients raised or grown in a more responsible way taste better. That’s up from 76% in 2011. 73% feels important to buy organic for certain food items, up from 61% in 2011 and 69% try to eat meat that has been raised responsibly and that’s up 53% in 2011.”

If there’s a better positioned publicly traded restaurant than Chipotle, we’d like to know about it.