We received the 4Q growth estimates on Friday so there was little in the way of surprise in the aggregate household spending and income figures for December released this morning. There are, however, a few dynamics worth highlighting in the detail data.

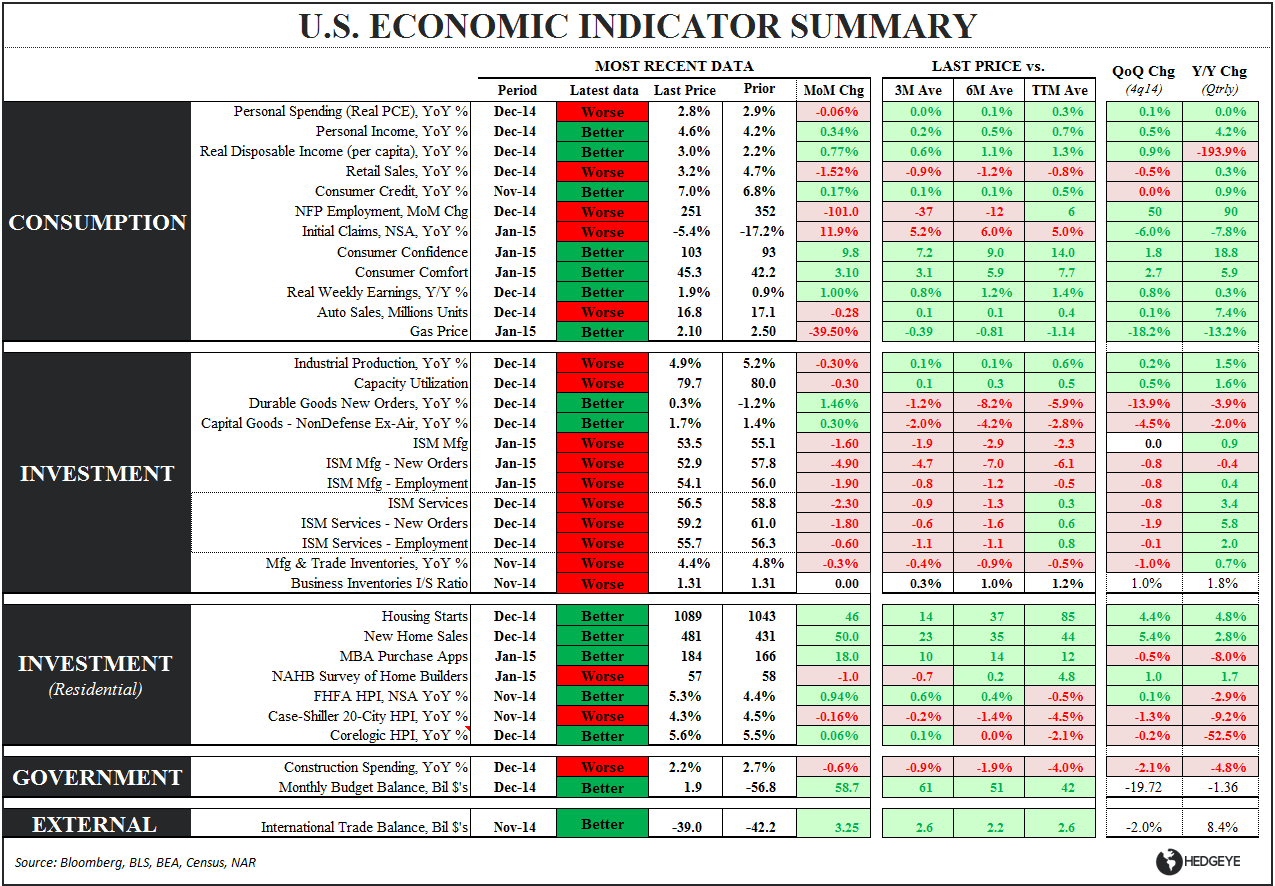

In short: Consumption growth slowed in December alongside a rising savings rate and likely moderation in revolving credit growth. Aggregate Disposable Income growth, meanwhile, continued to accelerate alongside an accelerating employment base and rising salary and wage growth. The annotations in the summary table below highlight these trends.

Spending: Real household spending declined -0.1% sequentially while decelerating modestly on both a 1Y & 2Y basis.

Spending growth slowed across all of Services/Durables/NonDurables with goods spending leading the December slowdown. The rise in the savings rate to 4.9% in December from +4.3% in November was responsible for most of the retreat in spending.

Revolving consumer credit growth broke out of its 3Y slumber in 2Q14 alongside accelerated spending on durables and the two have moved in lockstep the last 6+ months. It’s likely card spending moderates alongside the moderation in higher ticket discretionary consumption.

Income: Aggregate disposable income growth, per capita income growth and salary and wage growth all accelerated on both a 1Y/2Y basis in the latest month. Note, however, that the reported acceleration in December comes against a very easy comp and that compares get decidedly harder beginning in January.

HOURLY WAGE vs AGGREGATE INCOME GROWTH: The following, somewhat conflicting trends in Wage growth and Income growth have characterized the better part of the last 6 months:

- Wage Growth: The trend in nominal wage growth in the private sector has been stagnant at ~2% (a bit better for production & nonsupervisory workers) and decidedly soft in December with average hourly earnings growth slowing to 1.7% YoY. Note that the more recent ECI data – a more comprehensive measure of compensation – showed stronger compensation trends than those reflected in the monthly wage figures released alongside the establishment survey.

So, wage growth remains soft, but……

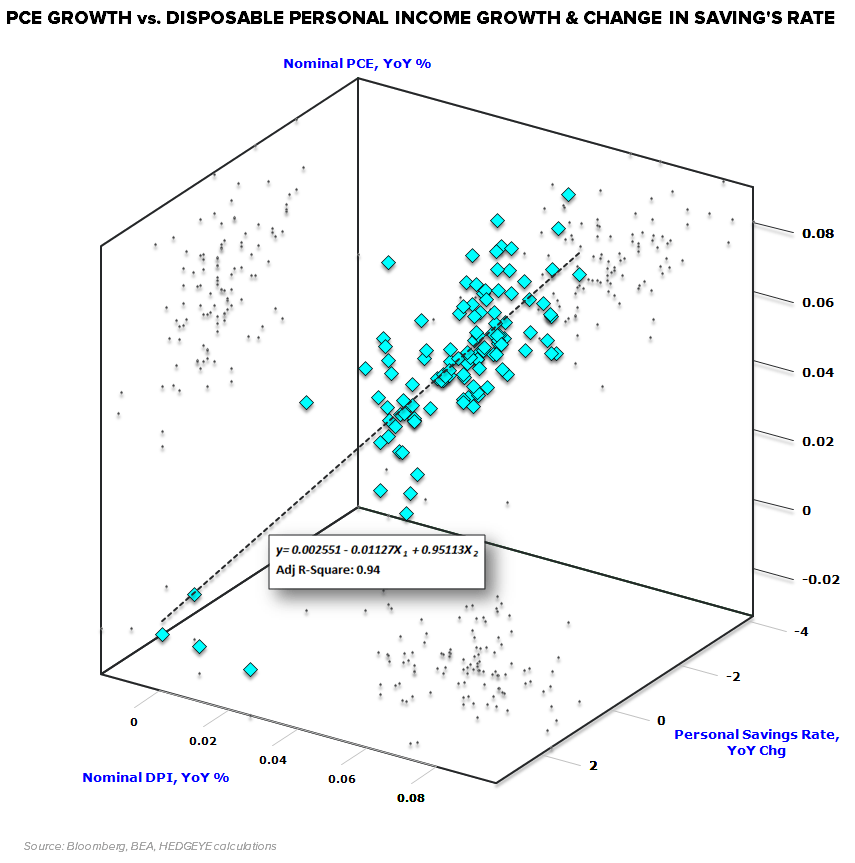

- Aggregate Income Growth: With total employment growth accelerating (ie. an accelerating employment base) in recent months, aggregate personal income growth has been able to accelerate in spite of middling hourly/weekly wage growth. The aggregate figures tell us nothing about distribution effects, but with the highest income quintile supporting the bulk of consumption spending and with the correlation between aggregate income growth and total household spending extremely tight over decades of data, the aggregate figures are the predominant driver of reported PCE growth.

Accelerating salary and wage growth and a rising savings rate are favorable fundamental developments although the rising savings rate mutes the flow through to actual spending growth.

Fundamental positives manifesting as a reported slowdown in household spending - in conjunction with a discrete deceleration in ROW growth – all (further) complicate dynamically allocating capital across asset classes, equity sectors, and style factors.

Consider the typical thought train and level of confliction/cognitive dissonance prevailing in recent investor discussions: OUS is slowing and we’re late cycle domestically. Late-cycle exposure is underperforming significantly alongside negative deflation leverage and the more recent domestic manufacturing data suggest the US is not divorced from the broader global reality. However, select early-cycle exposure could work alongside lower energy prices, TTM underperformance, stable labor market trends and lower rates catalyzed more by global than domestic forces. But, wait, how could early-cycle exposure work when we’re late-cycle, when shale state woes are beginning to pressure what had been accelerating improvement in initial jobless claims data and when while the preponderance of domestic macro data – while still okay on an absolute basis – is slowing on a rate of change basis.

Our rejoinder has simply been to remain long the long bond as both the fundamental data and quantitative setup continue to support it. We also continue to like defensive yield sectors along with select early-cycle exposure such as housing, but not at every time and every price.

Christian B. Drake

@HedgeyeUSA