“….the delicate balance across the Taiwan Strait will continue to Challenge the wisdom and strength of the government in Beijing”

Su Guaning, President of NTU, quoted in an interview in The Business Times Singapore on how China’s economy will evolve in the coming decade.

The gravitational pull of the mainland is becoming ever stronger for Taiwanese companies in advance of the historic memorandum of understanding on financial supervision that is expected to be signed in November. This is just the latest link between the two states since Beijing seized on the global recession as an opportunity to thaw relations. As “panda diplomacy” has evolved beyond symbolic gestures with the introduction of direct trade and travel and direct investments by PROC companies, the pace of development has quickened.

In the past month the number of Taiwanese firms seeking to take advantage of the accord by establishing partnerships on the mainland have grown rapidly, with prospectors ranging from the Taiwan Stock Exchange and leading brokerage Fubon Securities opening discussions with Shanghai counterpart to Sanyang Industry’s partnership with Chinese bus manufacturer Xiamen King to develop modern coach line vehicles for the mainland market.

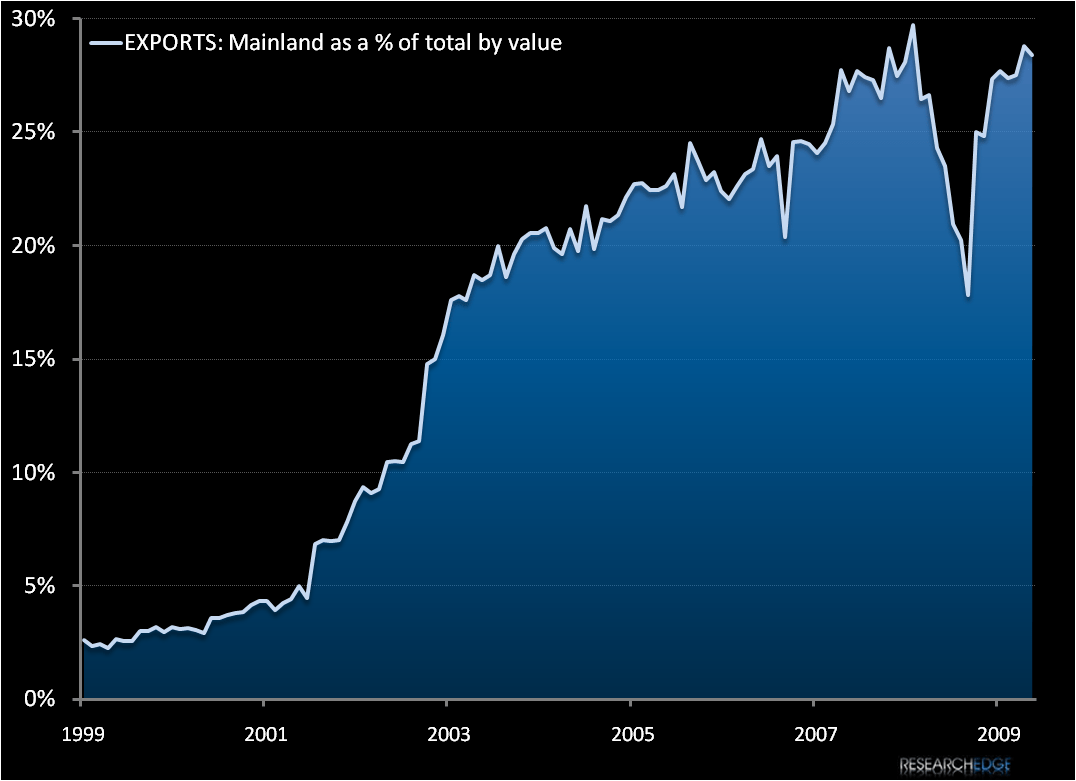

Rising from only 3% of total exports a decade ago to nearly 30% of the total today, the rising mainland consumer base has become THE critical growth market for Taiwanese technology and communications firms. This closer relationship is driving more than just exports, YTD the TAIX has traded with a strong correlation to mainland equities, racking up an R2 just shy of 90% YTD (see charts).

As the economic ties continue to draw the island nation closer to Beijing, it is important to note that the political and cultural obstacles remaining are immense. Officially the PROC government regards the island as a rebellious district rather than a separate state (let alone sovereign nation). A recent reminder of the long standing military tension was the conviction of US DOD employee James Wilbur Fondren two weeks ago. Fondren had been passing on sensitive pentagon documents from 2004 to 2008 regarding strategic planning for joint US/Taiwanese joint defense to a Taiwanese citizen posing as an operative for his government who was in fact an agent for Beijing.

We are long Taiwanese equities via EWT as a tactical play on rising Chinese consumer demand. In the long term, for better or worse, the two economies are intertwined. It remains to be seen if the common economic advantages of the current initiatives will lead to a political partnership equally as equitable.

Andrew Barber

Director