Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

Please note that we added Gold (GLD) this week and removed Yum! Brands (YUM).

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

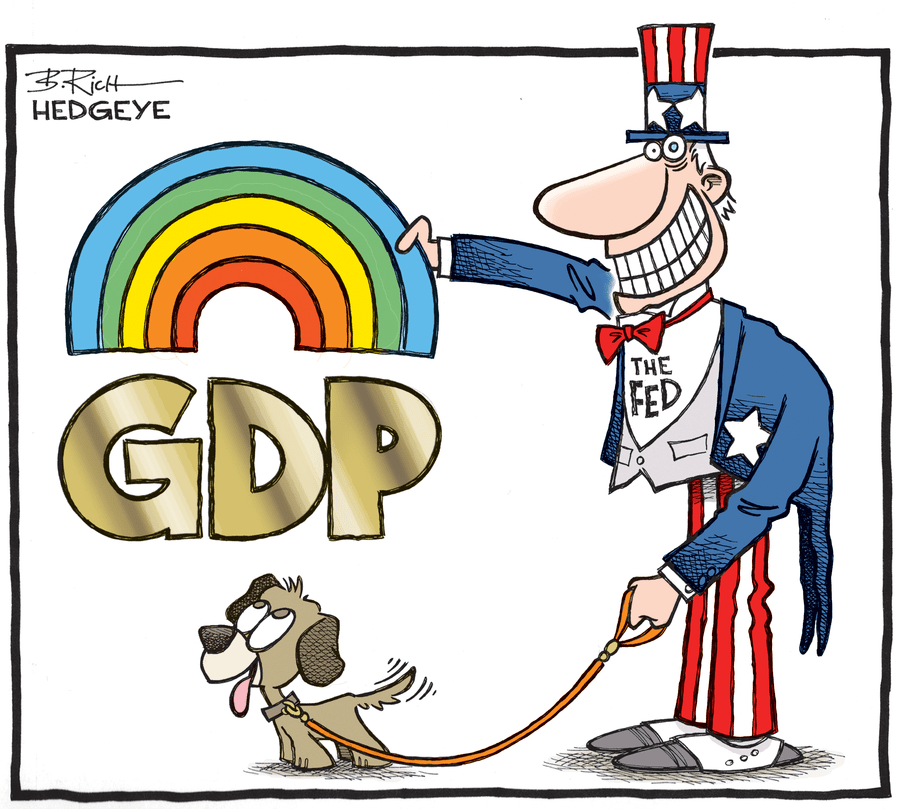

CARTOON OF THE WEEK

2014 full year GDP growth was +2.4%, not 5%. Our call was y/y growth peaked in Q4 of 2013, and it did.

IDEAS UPDATES

GLD

Gold completed its BEARISH to BULLISH TREND REVERSAL and we’re adding it back on the long side for 2015. We sent out our first buy signal in GLD on Tuesday. Keith added to that position in Real-Time Alerts on Thursday ahead of Friday’s GDP print (which missed expectations).

TREND DURATION = 3-Months or More

*Our real-time alerts product notifies subscribers of the exact time and price we are managing our exposure to our top investing ideas.

------

Dollar Down, Rates Down = #StrongGold

Bad economic data warrants an easier Fed, and Friday’s GDP print did in fact miss q/q annualized:

- Sequential (q/q) GDP annualized printed +2.6% for Q4 vs. consensus expectations of +3.0%

- Synching Friday’s print with our internal GROWTH, INFLATION, POLICY model, full-year 2014 GDP printed +2.5% vs. Hedgeye, Central Bank, and consensus forecasts of +2.4%.

March 18th is the next Fed catalyst, and we expect that they’ll announce a reversion from the plan to raise rates in June. The depreciation of the EURO and YEN against the dollar have already moved on their respective catalysts. The Fed has the next move, and we are front-running the foreseeable shift in policy.

We like an allocation to gold against our other macro positions and will look to buy on short-term pullbacks within the BULLISH TREND set-up.

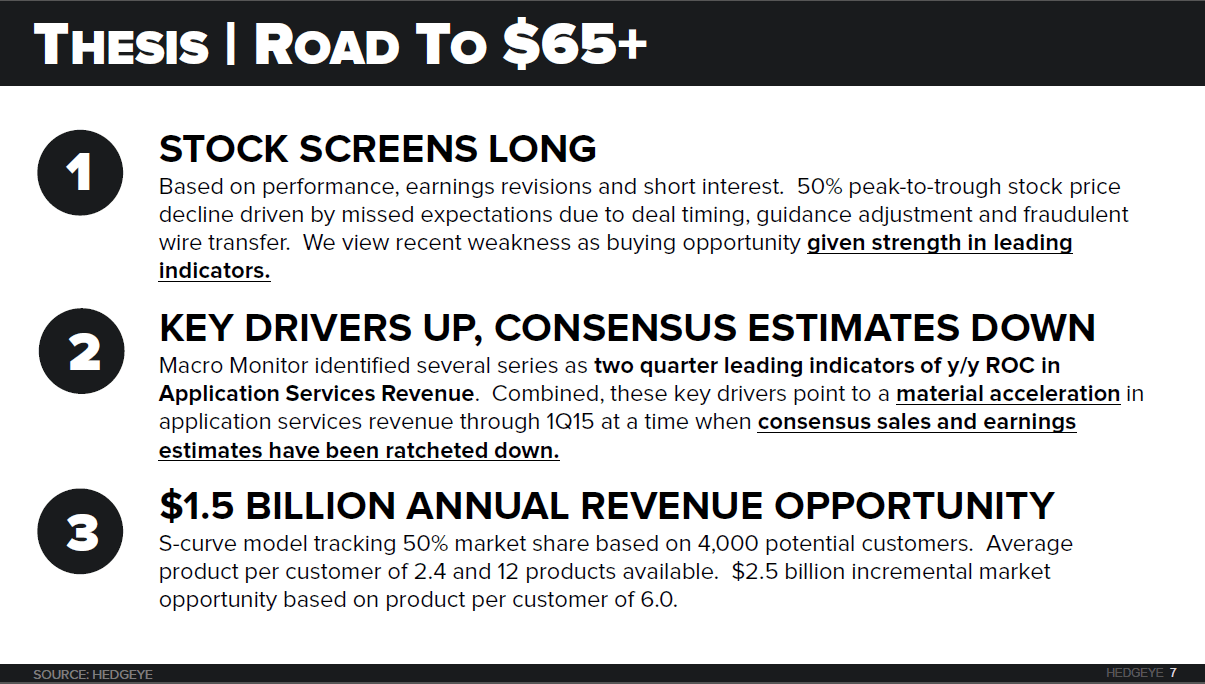

HOLX

Hologic finished the week up +3.8% versus down -2.4% for the S&P 500.

It's up approximately 14% since we added it to Investing Ideas at the beginning of the year, while the S&P 500 is down -3% year-to-date.

HOLX pre-announced a positive F1Q15 during the JPM Healthcare conference earlier this month, but did not update their guidance at the time. This week, the company officially reported earnings and raised guidance above consensus expectations. With this recent guidance raise and positive management commentary, HOLX is very likely heading above $40 sometime in the next 6 to 9 months, with $50 just around the corner. Accelerating revenue and earnings growth, a higher multiple, and earnings power above $2.00 gets us there.

We think this will be the first of several beat and raise quarters.

Earnings Call Highlights

Diagnostics: The most significant change from the quarter was stability in ThinPrep. Thanks to incremental disclosures the company is providing (positive trends tend to make companies more open) it's now possible to actually see the company's Cytology results, which while down in the US, managed to grow modestly year over year. Our OB/GYN survey has been flagging stability in US Pap trends and we will have the January update next week. Our model previously anticipated -10% declines over the next 2 years which will now improve to 0%, a massive acceleration and very accretive for the model.

M&A: When Hologic bought Cytec and Gen-Probe, they were plugging major holes in their businesses. In the first case, slowing/declining 2D mammography, in the second, declines in ThinPrep. While they still have to execute, looking out past peak 3D growth rates likely to occur in 2016/2017 and acting proactively, should be a significant tailwind to the multiple. In prior work we have found topline growth drives their EV/EBITDA and P/E multiples while debt metrics are largely irrelevent.

3D Mammography: Our estimate for Breast Health was too high coming into the quarter. We'll be running our update for US facility counts for January this weekend and reviewing the 10K. We'll refine our estimate and publish the results and update next week. We still believe consensus Breast Health numbers are too low. It was clear from the call that HOLX is taking share from GE, which will increase our out year estimates, and placement rates are accelerating, which we should capture in our survey. How that translates into revenue will be increasingly accurate in our model. Anecdotes regarding aggressive pricing from GE suggest they are acting out of a position of weakness.

Key to our thesis is 3D adoption, which continues to progress into the fast part of the adoption curve.

Transparency: It's always easier to deliver good news than disappointment, and we welcomed the increased details in HOLX's earnings presentation which provided greater detail. In this case a clear narrative supported by data will will go a long way to improving investor confidence and the multiple.

Debt Leverage: We hear the complaint, but think its misguided, that HOLX is over-levered. For such a stable business, with accelerating fundamentals, we think the concern is misguided. Regardless leverage is heading lower, which should allay those concerns.

MDSO

The Hedgeye Healthcare team has no material update this week ahead of Medidata Solutions earnings on Thursday (2/5 pre-market). We reiterate our expectations for the company to beat expectations on both the top and bottom line.

TLT | EDV | XLP | MUB

Editor's note: Our longstanding, non-consensus call on bonds remains the gift that keeps on giving. This January, TLT was up +10% versus the S&P 500 which was down -3%.

Per Hedgeye senior macro analyst Darius Dale:

Our #Quad414 theme is picking up steam with the deluge of this week's U.S. economic data and remains core to alpha generation in 1H15.

Click here to read the full report.

RH

Hedgeye's retail sector analysts have no material update on Restoration Hardware this week.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

Mcdonald's: a new beginning

The first email we received from a client following the news of Thompson’s departure yesterday posed a simple question: “Should I chase MCD tomorrow?”

Riding Strong Through the Actual and arithmetic blizzard of crummy macro data

Whether housing can remain an insular island of intermediate term strength against the burgeoning blizzard of global disinflationary pressure and decelerating domestic Macro data for December is the relevant question.