WHERE'S THE MARGIN GOING?

October 12, 2009

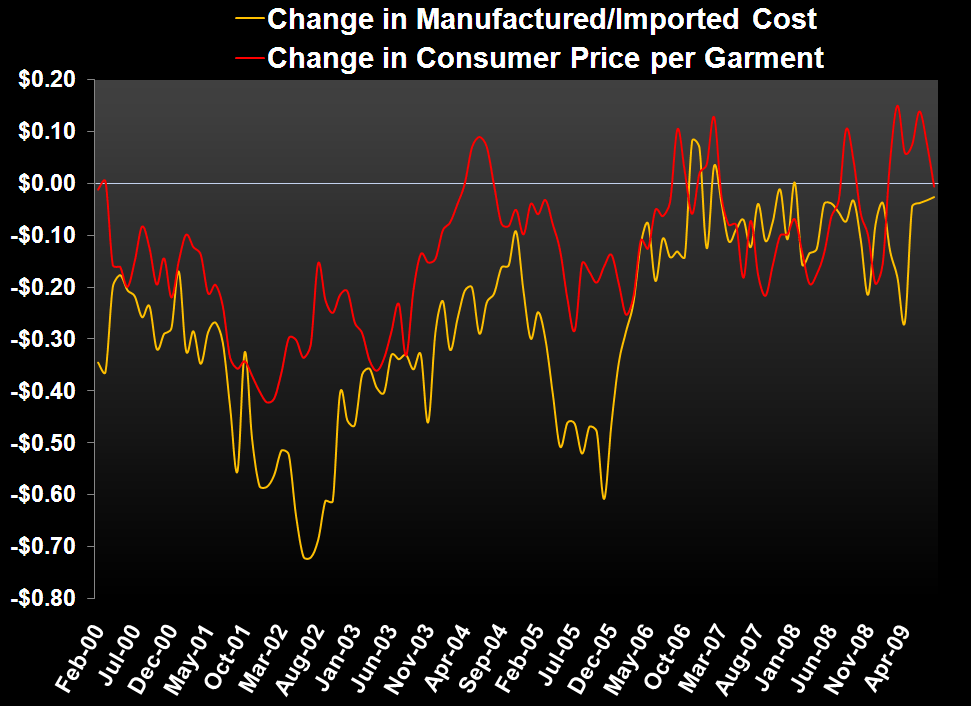

TODAY’S CALL OUT

There’s a notable call out in reconciling the latest apparel import price data with CPI. The punchline is that after a six-month time period where margin dollars increased, they narrowed meaningfully last month. Still a positive spread – implying that margins are still getting better – but at a far lesser rate. So many people look at CPI and raw material pricing data in yy % terms, but that’s simply inaccurate. Remember that the average retail price for an apparel garment is about $10, while the import price is about $3.50. So a 1% change in retail price equates to about a 3% change in import price to keep the margin equation in balance. So we measure the actual dollar spread between costs to consumers vs. the industry. On average, the spread is about a dime per garment. That might not seem like much, but at about 30 bn garments per year, we’re talking about $3bn in ‘margin jump ball’ injected into the industry per year – or about 100bp in margin. THAT’s why these stats matter. That’s also why I’m surprised to see that spread go near zero – just at the time (4Q) when the investing world at large thinks that 4Q will be a cakewalk.

LEVINE’S LOW DOWN

Some Notable Call Outs

- Li & Fung is getting louder about acquisitions. Currently the biggest supplier of apparel and toys to US Mass Retail, said it’s considering acquisitions of several U.S. companies with hundreds of millions of dollars in annual sales. The company has a $1 billion acquisition fund, and is eyeing “multi-hundred-million-dollar-sales companies” in the U.S., said President Bruce Rockowitz. Li & Fung may make “a series of acquisitions” within the coming months, and is also looking at companies in Europe and in Hong Kong, he said.

- As some retailers still try to figure out their ecommerce strategies, the effort is now expanding to m-commerce. By the end of this year about 50% of traditional retailers are expected to have mobile websites, up from 20% at the end of 2008. For now the biggest hurdle to mobile commerce is the consumer’s hesitancy to share sensitive credit card or personal information via a smartphone device. Expect credit card network operators including Visa and MasterCard to begin promoting safety and security as they roll out mobile strategies of their own.

- In an effort to get a jump start on the competition as well as the hype surrounding Black Friday, Toys R Us is expected to be open on Thanksgiving Day. Healthy competition and media attention is certainly part retail landscape, but there has to be some line drawn as it pertains to employee satisfaction. We wonder if any other retailers will follow, leaving their employees with just Christmas and Easter as the only two holidays guaranteed to be off.

- A reminder that the next U.S census is approaching and it will be measured as of April 1, 2010. As always, the census will have implications for all kinds of issues and businesses, including retailers. This massive “research” project which will examine the composition and demographics of the U.S population is expected to cost $15 billion to complete. Results will begin to be made public in spring 2011.

MORNING NEWS

-U.S. Imports Fall in August, Trade Gap Narrows - Textile and apparel imports to the U.S. continued their long decline in August, with Vietnam posting the only increase among major suppliers. The Commerce Department’s Office of Textiles & Apparel said Friday industry imports fell 9.8 percent to 4.2 billion square meter equivalents in August compared with a year earlier. The total volume of imports of textiles and apparel to the U.S. in August was the highest for any month this year, but in year-over-year comparisons imports have been declining since February 2008. Apparel imports fell 6.4 percent to 2 billion SME and textile imports dropped 12.7 percent to 2.2 billion SME. Imports of textiles and apparel from China dropped 0.7 percent to 2.1 billion SME in the month compared with August 2008. Apparel imports from China increased 9.1 percent for the month to 961 million SME, while textile imports from China fell 8 percent to 1.1 billion SME. <wwd.com>

-Argentina: Threat of tannery closures recedes as companies accept lower level activity - Information obtained from the Argentine Tannery Association CICA indicates that the threat of tannery closures has receded since the height of the financial and business crisis in the country last January. Tanneries are still well stocked with hides, mainly salted and in storage, as the kill was accelerated in reaction to the worst drought in 60 years which killed thousands of head. The premature kill of smaller animals has led to a reduction in larger hides for upholstery and with many smaller hides now available, tanneries are reorienting their business towards footwear production. The collapse in car sales world-wide has forces tanneries to diversify and change strategy instead of having all their eggs in one "automobile" basket. <fashionnetasia.com>

-European Commission Calls on Hungary to Change its VAT Reimbursement - The European Commission has called on Hungary to modify the relevant provisions of its VAT legislation which preclude Hungarian taxable persons from claiming reimbursement of input VAT where the underlying supply has not been financially settled by the taxable person. The request takes the form of a reasoned opinion, the second step of infringement procedure enshrined in Article 226 of the EC Treaty. The Hungarian VAT Act grants taxable persons the option to choose between carrying forward their excess VAT (which results from deductible VAT exceeding payable VAT in a tax period) to the next tax period or immediately claiming the refund of it. <ibls.com>

-McCarthy Puts Under Armour on the Offensive - Two months after taking over as captain of Under Armour’s footwear business, Gene McCarthy is drawing up a playbook that aims to offset the company’s weak sneaker sales. While the Baltimore-based company made big bets earlier this year on the debut of its running shoe, footwear revenues fell 19% in the second quarter, leading to major markdowns on inventory. Under Armour will report third-quarter results later this month, but analysts do not expect footwear figures to be much better. To combat that, McCarthy — who previously served as co-president of Timberland and worked for two decades as a Nike executive, with a stint at Reebok in between — said he is focused on building up the company’s design talent so its footwear has a “distinct design language unique to our brand.” McCarthy is also in the process of overhauling sourcing and development and is fine-tuning footwear distribution. <wwd.com>

-LVMH to Freeze Hiring, Salaries in 2010 - LVMH Moet Hennessy Louis Vuitton SA plans to freeze hiring and salaries in 2010 after a stagnation in sales and earnings this year, La Lettre de L’Expansion reported, without saying how it got the information. The company’s wines and spirits unit is showing a sales decline of 42 percent, La Lettre said. Overall 2009 revenue will rise 0.2 percent and net income will gain 0.1 percent, the newsletter said. LVMH is planning an acquisition in perfumes and cosmetics, according to La Lettre. <bloomberg.com>

-Marks & Spencer May Speed Up Non-U.K., Internet Retail Plans - Marks & Spencer Group Plc, the clothing retailer fighting two years of declining sales in its home British market, may announce plans for more international stores and an enlarged online offering tomorrow. Finance Director Ian Dyson is scheduled to speak to analysts and investors in London, and Britain’s biggest clothing retailer by revenue has said he will discuss “developments” outside the U.K., without giving more details.

-CVS, Walgreen Have Spot Flu-Vaccine Shortages as Demand Surges - CVS Caremark Corp. and Walgreen Co., the two largest U.S. drugstore chains, are experiencing spot shortages of seasonal-flu vaccines because of increased demand. CVS MinuteClinics in Austin, Texas, and New York ran out of the seasonal-flu vaccine within the past week before restocking, according to calls to 13 stores by Bloomberg News. Calls to eight Walgreen stores in Manhattan on Oct. 5 determined none had it at the time. There are also shortages in the South and Southeast, said James Cohn, a Walgreen spokesman.

Demand for seasonal-flu vaccinations has soared because of public awareness of the H1N1 virus, known as swine flu, Cohn said. Walgreen administered twice as many doses in September as in the entire 2008 flu season, he said. <bloomberg.com>

-Asda is Top Clothing Retailer in Britain - According to TNS data, Asda has become Britain's biggest clothing retailer with its George brand achieving 10.1 percent market share. The growth was driven largely by school uniforms and womenswear. "Our objective was to be No. 1 by volume by 2011, so we're 18 months early," Anthony Thompson, George's managing director, told The Times. <licensemag.com>

-DKNY Jeans set to be launched this month in India -DLF Brands Ltd, the retail and lifestyle division of DLF Ltd, today announced its agreement with Christina Ong’s Club 21 Group, the international licensee for DKNY Jeans, to launch the brand following the successful introduction of the DKNY brand in the Indian market earlier this year. The first two DKNY JEANS stores will be launched in New Delhi in October 2009 at DLF Place, Saket and the DLF Promenade, Vasant Kunj. Both the DKNY and DKNY JEANS brands are owned by Donna Karan International, Inc. and are sold in India under license. <indiaretailing.com>

-eBay India launches Global EasyBuy - eBay India (www.ebay.in), India’s leading eCommerce Marketplace, today announced the launch of Global EasyBuy - The International Online Shopping Destination - which provides Indian shoppers with instant access to an unprecedented 18 million products. Global EasyBuy (www.ebay.in/geb) is aimed at redefining the Indian retail landscape and will provide savvy Indian shoppers access to the world’s hottest labels and coolest brands from the comfort of their home. <indiaretailing.com>

-Chloé Awarded $7.2M in Infringement Suit - A federal court on Friday entered a $7.2 million default judgment against a Los Angeles supplier after he failed to respond to an infringement lawsuit filed by Chloé. According to court documents, Mohammed Alexander Zarafshan, who did business as Alexander Zar, was aware of the 2006 suit and initially gave a deposition in the case, but never formally answered the complaint. A judge can enter a default judgment if a defendant fails to respond within a given time. <wwd.com>

-Trovata, Forever 21 Settle Lawsuit - Trovata and Forever 21 have settled the lawsuit that Trovata brought against the fast-fashion chain alleging it willfully and intentionally copied its designs on seven garments in 2007. The settlement comes just as a second trial was set to begin in the case this Tuesday, Oct. 13. The companies have recently resolved their differences to their mutual satisfaction, without any admission as to liability, and the action has been dismissed. The terms of settlement are confidential. <wwd.com>

-Chanel to Open Shanghai Boutique - Chanel is gearing up to make a splash in Shanghai on Dec. 3, when it will stage a fashion show for a luxury pre-fall collection and open an art-filled 5,160-square-foot boutique in the Peninsula hotel on the historic Bund riverfront promenade. <wwd.com>