Editor's note: This is a brief excerpt from today's Morning Newsletter written by Hedgeye U.S. macro analyst Christian Drake.

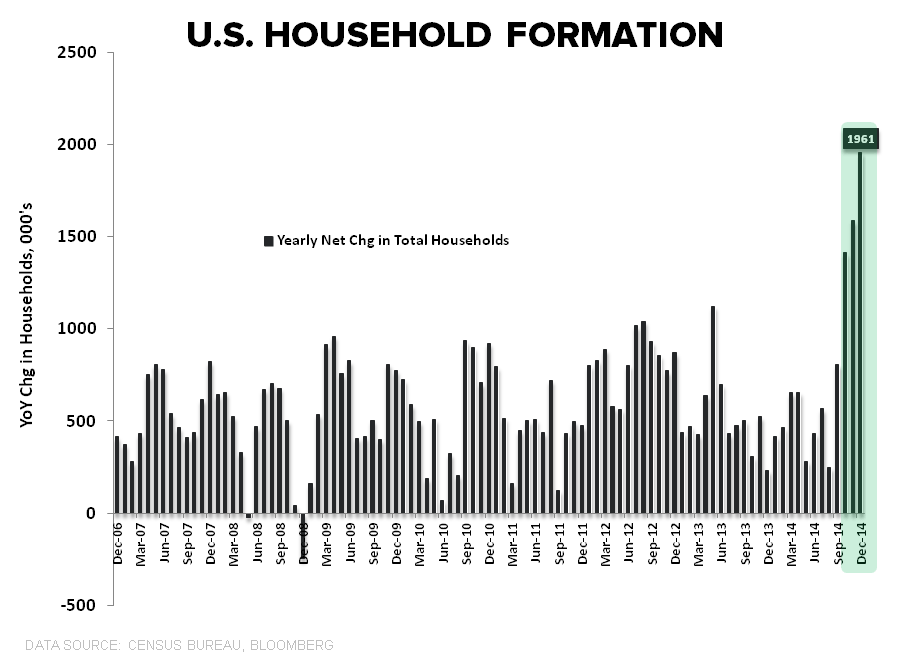

- Household Formation: The same survey data showed household formation was en fuego in 4Q. As can be seen in the Chart of the Day below, the CPS/HVS survey estimated that the total number of households grew by 2.0MM in December vs a year earlier, the largest yearly change since July 2005. On a rate of change basis, year-over-year growth accelerated to +1.4% in 4Q – up from 0.4% growth in the Jan-Sept period and the first material acceleration in 8 years.