If the market’s reaction to Brinker’s EPS release yesterday is any indication of what’s to come, look out. EAT, despite delivering a meaningful top line, bottom line, and same-store sales beat, traded down -1.78% on the day. Suffice to say, expectations are high heading into earnings season and those that underperform will likely be punished.

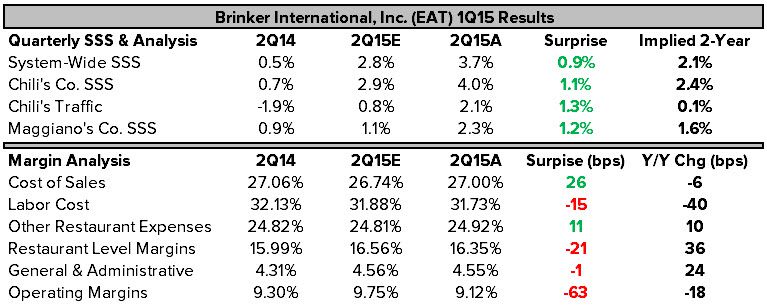

EAT had a strong quarter, but the street was likely disappointed with the lack of leverage in the business model given such strong comps. Cost of sales, in particular, driven by burger meat, cheese, avocado, and salmon, drove some of the margin pressure in the period – but it was still down 6 bps y/y. In 3Q15, Brinker will be lapping a very difficult comparison on this line, suggesting that the 26 bps y/y improvement analysts expect won’t be happening.

Continued sales momentum, labor leverage, and prudent capital allocation should help management offset these pressures, as they maintained full year EPS guidance range of $3.00-3.15, which would be good for 11-16% growth.

In our view, Chili’s culinary vision (Fresh Mex, Tex Mex) and guest experience (service, Ziosk) initiatives are on point and should help play into the company’s goal of changing consumers’ mindsets around the brand. This approach is in contrast to that of some casual dining chains that have turned to a promotional/discounting strategy to drive traffic. While the former may take longer to yield results, it is undoubtedly a more admirable and sustainable approach than the latter. Whether this approach will even the playing field with fast casual or not is still to be determined, but management appears confident in that assertion.

Outside of the well-guided initiatives to drive same-store sales and traffic, Brinker’s capital allocation strategy remains best in class:

- Invest in the business

- Manage debt levels

- Keep some cash on hand

- Return remaining cash to shareholders through dividends or share repurchases

With YTD cash flow from operations at $162 million and over $78.4 million of available cash on the balance sheet, EAT’s capital discipline remains an important part of the story.

The Good

- Revenues of $742.9 beat consensus estimates by 87 bps

- Adjusted EPS of $0.71 beat consensus estimates by 331 bps

- Significant same-store sales beats across the board

- 2% traffic growth resulted in the best two-year average number (+0.1%) since 1Q13

- System-wide rollout of tabletop technology from Ziosk is complete

- Reimage program is 95% complete

- Tabletop gaming revenue and retail revenue led to double digit growth on the other revenue line

- Revenue from tabletop tablets offsets the cost

- Significant labor leverage from higher sales and an adjustment to lower employee health insurance expense

- Maggiano’s posted record high delivery and banquet sales

- Repurchased 1.1 million shares in the quarter for about $60 million

- Repurchased an additional 600,000 shares since the end of the quarter for about $36.2 million

- On the weather front, should provide more upside to comps in 3Q15 than 2Q15

- YTD cash flow from operations is $162.5 million

- Ended the quarter with $78.4 million of available cash on the balance sheet

The Bad

- Cost of sales came in much higher than anticipated due in large part to burger meat, cheese, avocado, and salmon inflation

- Expect continued commodity pressure, particularly in the third quarter which has a difficult comparison

- Restaurant expenses came in above estimates due to tabletop device rentals, credit card fees, and higher pre-opening expense

- Operating margins down 18 bps y/y due to the aforementioned headwinds

- Facing some headwinds internationally