This note was originally published at 8am on January 15, 2015 for Hedgeye subscribers.

“Stars can’t shine without darkness.”

-Unknown

It is indeed the contrast that draws one’s eye towards something that is different.

Every once in a while in Independent Research we earn an opportunity to see that light develop before consensus does. God willing, the search for macro stars is what has my two feet on the floor each morning of every risk management day.

While it would be convenient to skip over the #deflation part of an epic central planning experiment, unfortunately that’s not the way the cycle from day to night works. There will be darkness before America’s free market economy can shine again.

Back to the Global Macro Grind…

Don’t forget that I had the lowest grade in my freshman creative writing course @Yale. “So”, I’m still working on it (thanks for bearing with me over the years!). I’d love to go back to New Haven and slap some hash-tags on my English Lit prof’s desk.

While I probably don’t deserve a Ph.D. (or a perma bull II vote) for this, I’ve always said that un-elected central market planners would perpetuate the next crisis. That’s #on this morning – follow the interconnected risk:

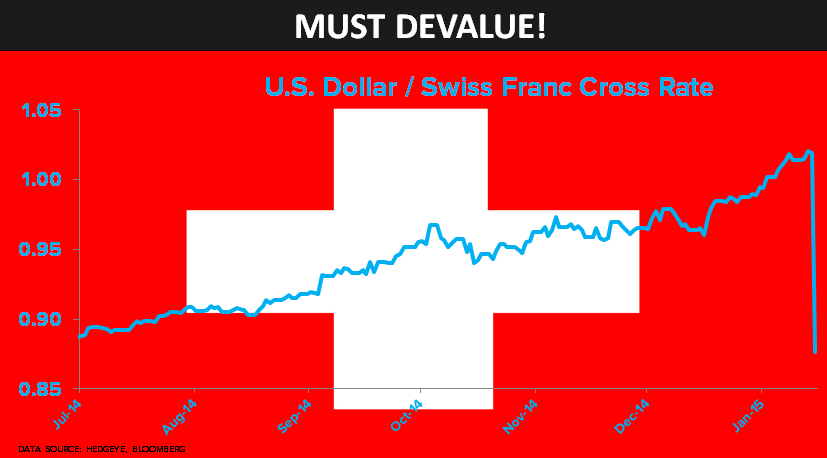

- SWISS – there’s CTRL+Print, then there’s panic – and this is rightly A) freaking people out and B) equating to a massive margin call on levered FX trades – Swiss cut by 50bps (to neg -0.75%!) and cut the wire loose on their exchange rate? (Richemont -11.2%, Swatch -8.5%, UBS -7.2%, Adecco -7.9%, Credit Suiss -8.2%, Julius Baer -7.5%, ABB -7.4%) #nice

- OIL – follow the #Deflation Dominos – Yens, Euros, Francs panic/burn > Up Dollar > Crashing Oil > Spreads blow out in High Yield Energy > Energy States lose moneys and jobs > Financials and Industrials follow (late-cycle rolls) > Fed doesn’t hike … this was the call I made in our Macro Themes Deck for Q1, reiterating it this am

- FINANCIALS – yesterday’s drop in JPM was its biggest since 2011. Volume was huge. Remember 2011? Financials worst perf #divergence vs Utilities, ever. XLF already -5% for the YTD and the Regional Banks are in the midst of a 10% draw-down since that no-volume all-time SPX high on December 29th (2090)

“So” how are you feeling about some of our #Quad1 US equity long ideas now? After seeing the US stock market drop in 10 of the last 12 trading days, I’m thinking some of those look a tad early!

What’s really cranking for us are these #Quad4 Deflation ideas (Long #TLT!). And that makes complete sense to me, because:

- In Q1, globally #Quad4 doesn’t bounce to #Quad1 anywhere but in the USA

- USA is still coming to grips with the #Quad4 slowdown that happened in DEC and Q4 of 2014

Slowing? Yeah, that “everything is awesome” LEGO gas station thesis that everyone and their brother in long-only USA equity land ended up being almost as fictional as the movie. At -0.9% month-over-month, that was a big US Retail Sales miss.

It wasn’t recessionary, and that wasn’t our call anyway. It was simply A) slower in rate of change terms (both sequentially and on a 2yr comp basis) and, more importantly, B) way worse than the Old Wall was prepped for.

Go back and read their tweets. My boy Lavorgna was tweeting in sync with Bloomberg/CNBC’s new editorial JV macro team that the US economy was “booming” and that it was a “closed economy, unaffected by the global slowdown.”

Then they got Swissy’d.

Don’t you hate when that happens? When an un-elected Swiss dude wakes up in the morning and whacks his country’s stock market for a 7% down day and takes out Zervos’ spoooz at the knees?

Yes, I am going to call these people out by name this time. Oh, right – I did last time too. And, no, it’s not “mean” or unprofessional. It’s what someone with a spine needs to do, or our profession will never be held to account and evolve.

Due to the countless conflicts of interest associated with the aforementioned brokers, banks, and advertisers, the consensus complacency about risk remains the greatest risk to your country, children, and their future stars.

Our immediate-term Global Macro Risk Ranges are now (I’ll give you all 12 Big Macs in our Daily Trading Ranges report from this morning – in brackets is our intermediate-term TREND views):

UST 10yr Yield 1.78-1.97% (bearish)

SPX 1991-2031 (bearish)

SMI (Swiss Index) 8471-9016 (bearish)

FTSE 6230-6467 (bearish)

VIX 19.27-22.51 (bullish)

USD 91.48-93.11 (bullish)

EUR/USD 1.16-1.19 (bearish)

Yen 116.43-119.12 (bearish)

Oil (WTI) 44.43-48.97 (bearish)

Natural Gas 2.74-3.31 (bearish)

Gold 1213-1245 (neutral)

Copper 2.45-2.71 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer