THE QUALITY/JUNK TRADE COUNTDOWN...

OCTOBER 9, 2009

TODAY’S CALL OUT

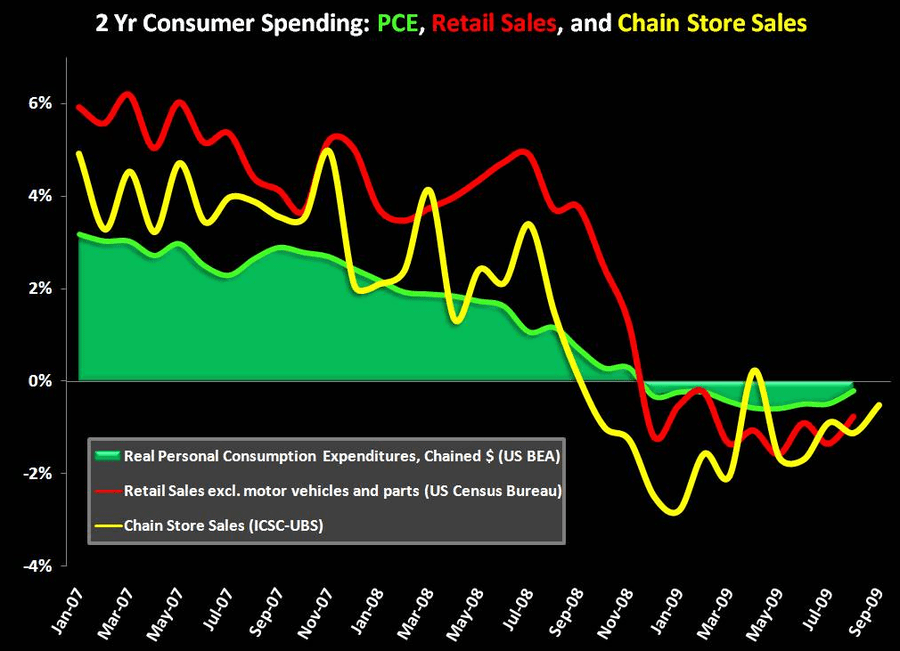

With all the noise from SSS having passed, let’s see what it REALLY means as it relates to the underlying trend in consumer spending. As a reminder, let’s keep in mind that Personal Consumption is about $10 trillion. Retail sales is only $3.7 trillion. Chain store sales is about $500 billion, and yes that number continues to shrink as more retailers opt out of reporting monthly numbers to the National Retail Federation. While this is hardly an original thought, the bottom line is that underlying trends are getting better on both a one and 2-year basis. The latter is particularly important given that it blocks out noise associated with weather, fashion, etc… In looking strictly at the math – which has not been a bad bet of late – we’ve got another three months of this. Then we need a stronger consumer to keep the trajectory going. Are you willing to make that bet? I’m not. I’m sticking with those companies that are proactively managing their businesses to win regardless of the underlying consumer climate. That’s when the winners will be more apparent. I continue to believe that there will be a meaningful quality/junk bifurcation trade in 1Q10.

LEVINE’S LOW DOWN

Some Notable Call Outs

- Absent in yesterday’s partnership announcement between JC Penney and Liz Claiborne was any mention of the small, but high profile menswear collaboration with John Bartlett. While the line was well received by the fashion world, it too will be shuttered as the Liz Claiborne and Claiborne wholesale brands convert to a licensed model.

- Earlier this summer we passed on a blog post from Fashionista suggesting that LVMH was shopping DKNY. Now the same blog is suggesting the company has had enough with its smaller, money losing fashion brands, Celine, Loewe, and Kenzo. Supposedly DKNY is also still for sale but so far there have been no serious offers. We have no track on this French luxury powerhouse, but with media power shifting to the blogosphere we can’t rule this one out.

- While sales in early September were expected to and did get a boost from Labor Day timing, it’s also worth noting that week 5 was also a strong week. Most retailers reported strength at the end of month, which likely coincides with the beginning of the extreme volatility (weakness) that began to permeate the malls at this time last year.

MORNING NEWS

-Yohji Yamamoto Inc., a Japanese distributor of mens and boys clothing, has filed for bankruptcy protection with the Tokyo District Court - Japanese investment company Integral Corp. released the news Friday by issuing a press release stating that it will finance the fashion house’s restructuring efforts. Yohji Yamamoto, which was rumored to be suffering, has called a press conference for Friday evening in Tokyo. A spokewoman declined to comment at press time. <wwd.com/business-news>

-US Retail Sales See First Rise In a Year - US retail sales have seen the first rise since the financial crisis of September 2008. September’s sales were up 1.1% on the same month last year, according to the Retail Metrics comparable sales index. The rise was attributed to stronger autumn fashions, more aggressive promotional activity and a particularly weak comparative performance when the markets collapsed last September. Fashion retailers that beat expectations included Limited Brands, owner of lingerie chain Victoria’s Secret, which saw a 1% rise in sales despite analysts predicting a 2.4% drop. Teen clothing chain Aeropostale saw a 12.7% sales rise. The US luxury market is still in decline with department stores such as Neiman Marcus and Saks reporting double digit declines. <drapersonline.com>

-Obama Allies Continue Laying VAT Groundwork - Despite President Barack Obama's "firm pledge" not to raise "any form" of taxes on families making less than $250,000 per year, the President's advisors and Democratic allies continue to float the creation of a Value-Added Tax (VAT). "It's getting more and more obvious that President Obama and Democrats in Washington, D.C. are laying the groundwork for a VAT," said ATR President Grover Norquist. "Apparently not content with violating his tax promise several times during the healthcare reform debate, President Obama now wants to tax every purchase made by every American -- including those earning less than $250,000." <prnewswire.com>

-Levi’s Third-Quarter Profits Fall - Falling sales in the U.S. and European markets coupled with rising costs led Levi Strauss & Co. to a 41.2% earnings slide during the third quarter. For the three months ended Aug. 30, the San Francisco-based denim giant saw earnings decline to $40.7 million, compared with earnings of $69.2 million during the same period a year ago. Selling, general and administrative expenses rose $7.4 million, or 1.9%, to $396 million. <wwd.com>

-Skechers USA Inc. announced that the company is expanding into Mexico - The Los Angeles-based company has entered into a deal with Leon, Mexico-based footwear company Grupo Charly to exclusively license and distribute the brand in Mexico. Grupo Charly will use its manufacturing resources in Vietnam to produce the collection, according to a statement. Men’s and women’s shoes will hit key retailers in Mexico this year, and children’s product will debut in 2010. Additionally, Grupo Charly plans to open a minimum of 10 Skechers retail stores in Mexico by 2014, with the openings beginning next year. Pushing a major expansion initiative, the brand announced earlier this week its upcoming move into India, and other deals for distribution in Chile, Malaysia and Brazil have already been inked. <wwd.com/footwear-news>

-Gap Inc. plans to move its Manhattan offices downtown without downsizing the staff - The San Francisco-based retailer is consolidating its two New York creative offices into a 200,000-square-foot space at 40 Worth Street in TriBeCa, putting the creative teams from the Gap and Banana Republic divisions — including designers, technicians and production personnel, as well as some business functions that support the corporate office — under one roof. The teams will be phased into the new site starting next year and finishing by the end of 2012. Gap says there are financial benefits in combining in one place over the long term but the short-term, however, will incur costs associated with the move. <wwd.com/business-news>

-Ferragamo Plans to Open Stores in Mongolia, Turkey in 18 Months - Salvatore Ferragamo SpA, whose shoes are worn by Jennifer Lopez and Zhang Ziyi, plans to open stores in Mongolia, Turkey and Egypt to tap rising demand for luxury goods in emerging economies. The Florence, Italy-based company may start stores in those locations in the next 6 to 18 months, adding to planned ones in China and the U.S., Chief Executive Officer Michele Norsa said in an interview in Hong Kong. The board meets today to review 20 projects that may lead to the opening of as many as 10 stores globally next year, he said. <bloomberg.com>

-Majestic Athletic Airs First Network TV Commercial - With the start of the MLB (Major League Baseball) Divisional Series, Majestic Athletic will be airing its first network television commercial. Majestic’s spot is one of few product ads that feature actual MLB on-field footage. The ad promotes Majestic's new replica jerseys launched early this year. The new replica offers a significant improvement by incorporating official fonts for player names and numbers. <sportsonesource.com>

-Dina Lohan launching her own line of footwear called 'Shoe-han' - Another member of the Lohan clan is getting into fashion. Last week, Lindsay Lohan made her debut as "artistic adviser" for the French fashion house Emanuel Ungaro. Now, according to EOnline.com, her mother Dina will sell her own line of foot wear. The forthcoming, and very affordable, collection will be known as Shoe-han. No, this is not a joke. The shoes represents a collaboration between one of the world's most controversial stage mothers and a Long Island-based company called "I Love My Shoes." <nydailynews.com>

-Christian Lacroix, which is in administration, receives a formal purchase offer from Ajman sheikh - The offer from Al Hassan Bin Ali Al Nuaimi, in cooperation with the couturier, must still meet the approval of the commercial court here. However, the Paris administrator told Agence France Press it is “likely” to meet approval because it would preserve jobs and pay third-party debts. A date for a hearing has yet to be fixed, but is expected around Oct. 20. It is understood Bernard Krief Consulting and Financière Saint-Germain also have submitted bids. <wwd.com/business-news>

INSIDER TRANSACTION ACTIVITY:

LIZ: Doreen Toben, Director, purchased 5,000 shares ($25k).

NILE: Diane Irvine, CEO, sold 6,000 shares ($366k) after exercising the right to buy 6,000 shares, roughly 16% of total common holdings.

PETM: Jaye Perricone, SVP Real Estate, sold 10,000 shares ($220k) after exercising the right to buy 10,000 shares, nearly 24% of total common holdings.

GIII: Deborah Gaertner, President of Women Sales, sold 4,000 shares ($64k) after exercising the right to buy 4,000 shares, nearly 14% of total common holdings.

PETS: Bruce Rosenbloom, CFO, sold 3,000 shares ($60k) after exercising the right to buy 3,000 shares, roughly 12% of total common holdings.

PERY: Cory Shade, General Counsel, sold 2,000 shares ($34k), roughly 31% of total common holdings.