Recent Notes

01/20/15 Post-MLK Day Mashup: SBUX, MCD on Tap

01/23/15 SBUX: Closing Best Idea Short

Events This Week

Wednesday, January 28th

- EAT earnings call 10am EST

Thursday, January 29th

- SONC Annual General Meeting

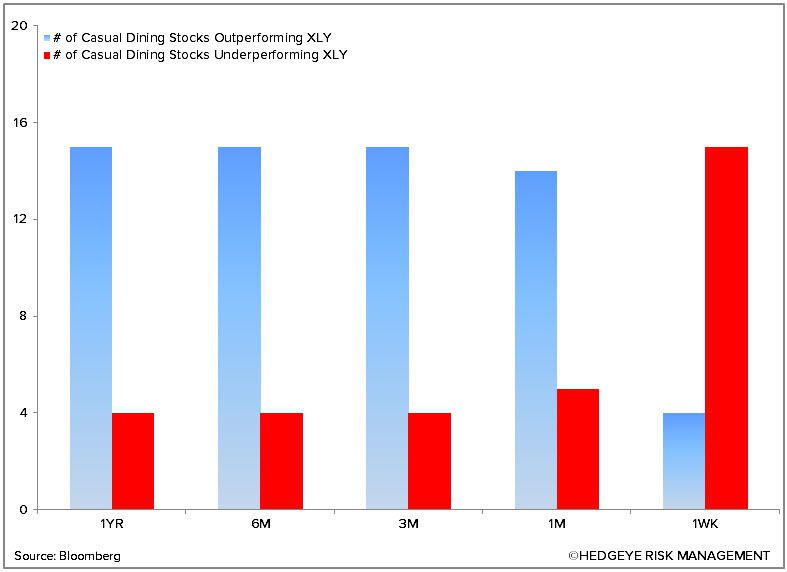

Chart of the Day

Recent News Flow

Tuesday, January 20th

- BJRI upgraded to buy at KeyBanc with a $52 PT.

- CAKE upgraded to outperform at William Blair.

- CHUY Vice President of Operations Southeast, Frank Biller, has resigned from his position. Mr Biller will remain with the company in an advisory role.

- EAT downgraded to hold at Wunderlich with a $65 PT.

- PNRA downgraded to hold with a $185 PT.

Wednesday, January 21st

- MCD FY15 and FY16 estimates reduced at Janney, citing its latest franchisee survey.

- RUTH completed the previously announced sales of Mitchell's to Landry's.

Thursday, January 22nd

- COSI CFO Scott Carlock resigned to pursue other opportunities. Richard Bagge will serve as interim CFO, while the company works with an executive search firm to find a new full-time CFO.

- JBFCF Philippine's largest food company, Jollibee Foods said it is keen to buy a U.S. quick-service chain worth at least $1 billion and may partner with a PE firm to do so. We believe KKD, JACK, PLKI, SONC, WEN, LOCO and FRGI are all in play.

- JMBA announced the expansion of its Whole Food Nutrition and Fruit & Veggie smoothie lines with the introduction of two new flavors: Amazing Greens and Greens 'n Ginger.

- SBUX announced that current board member Kevin Johnson will assume the vacant position. Schultz noted that, while Johnson’s responsibilities will mirror Alstead’s, he will be more heavily involved on the digital side of the business than his predecessor. Johnson formerly served as a President at Microsoft and, more recently, as CEO of Juniper Networks.

Friday, January 23rd

- BLMN announced that director, and former Bain managing director, Mark Nunnelly provided the company with notice of his resignation, effective February 15, 2015.

- CBRL Senior Vice President of Strategic Initiatives, Edward Greene, notified the company that he plans to retire from his position around November 2, 2015. The firm is conducting a search for a new Senior Vice President, Marketing.

Sector Performance

The XLY (+3.2%) outperformed the SPX (+3.0%) last week.

Quantitative Setup

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

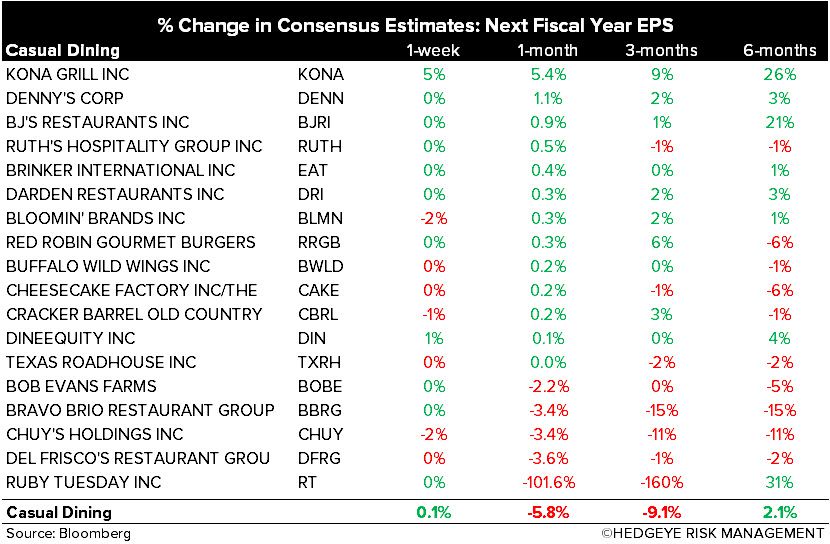

Casual Dining Restaurants

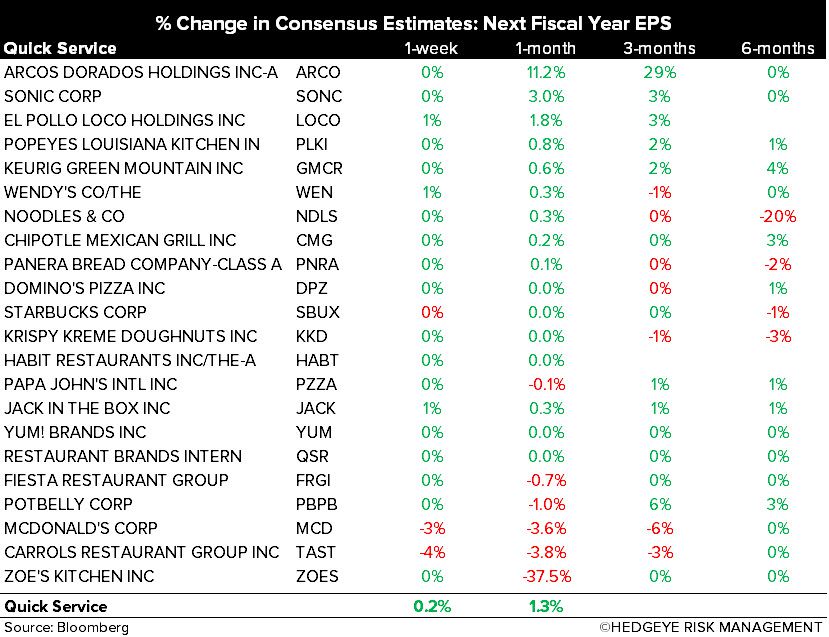

Quick Service Restaurants