This note was originally published at 8am on January 12, 2015 for Hedgeye subscribers.

“Disciplinary science has died.”

-Alan Leshner

From a risk management perspective, if something embedded in your #process is dead or dying, you better come up with something better to replace it!

Since 2001, Alan Leshner has been the Executive Publisher of the journal Science. He was cited in a fantastic #behavioral book I just finished reading called The Medici Effect, where he added that “most major advancements involve multiple disciplines.”

George Cowan, from one of the birthplaces of Complexity Theory (the Sante Fe Institute), added that “you need to get scientists to think about things other than their specialty.” (pg 27) This is so obviously true in asset management today. And I think we are so early.

Back to the Global Macro Grind…

Since many US institutional investors still focus exclusively on the US Equity market, there is a lot of frustration out there when it comes to relative performance compared to their US stock market index bogeys.

While I’m obviously sympathetic to what people are paid to do, that doesn’t mean I have to put my head in my hands and capitulate alongside them. I can only re-explain that broadening one’s horizons beyond what the SPY is doing is going to help them win.

If you’ve evolved your process to Cross-Disciplinary Macro you should be killing it right now. There are major asset classes like Long Duration Sovereign Bonds (think TLT) that are going straight up at the same time that others (like Commodities) are going straight down.

If you’re a US Equity only investor (and you’ve expressed the aforementioned position in what we call Sector Style Factors), you should be crushing it too. Look at last week’s S&P Sector level returns:

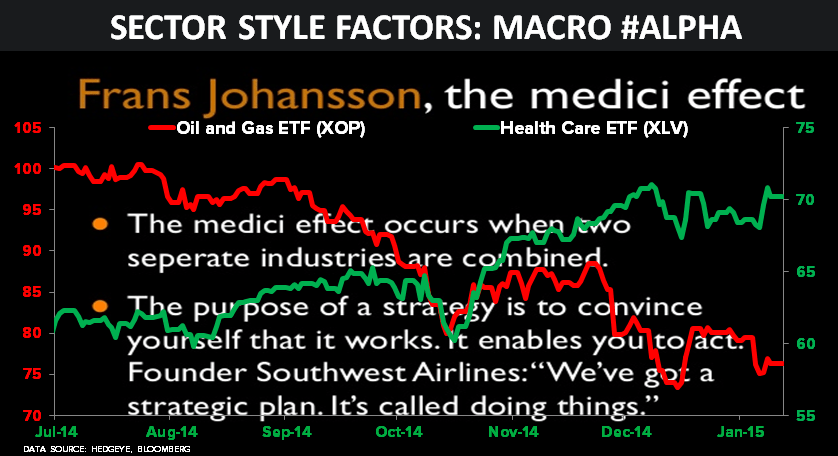

- Healthcare Stocks (XLV) +2.3% week-over-week to start 2015 +2.7% YTD

- Consumer Staples (XLP) +1.6% on the week to start the year +1.3% YTD

- Energy Stocks (XLE) down another -4% last week to -3.5% YTD

- Industrial Stocks (XLI) -1.9% week-over-week to start 2015 -2.1%

- SP500 -0.7% last week to start the year -0.7%

In other words, instead of banging you head against the Old Wall trying to short SPY into a global #GrowthSlowing + #Deflation, all you had to do was be short both of those factors and long the 2 S&P Sectors that literally jump off the page in our Macro Playbook on the long side.

I can recap why Healthcare (XLV) and Consumer Staples (XLP) outperform in what we call #Quad4, but since I have been writing about this since September, there’s no need to be repetitive. Since October, our net asset allocation to Commodities has been 0%.

How about a US equity only “Income Fund”? Here’s the other very basic differential your portfolio should have capitalized on last week:

- US REIT Stocks (MSCI Index) +3.5% week-over-week to start the year +5.0% YTD

- US MLP Stocks (Alerian Index) down another -3.5% on the wk to start 2015 -2.5%

Again, when A) global growth is slowing, bond yields are falling… so you buy stocks that look like bonds… but B) you don’t buy the ones that have two-rocks tied together (Oil + Energy Leverage) like these widely owned and overvalued upstream E&P MLP stocks.

If you run a diversified macro fund, making lower-volatility (and higher absolute) returns was so easy a Mucker could do it last week:

- Long Bond Bulls got paid bank with the UST 10yr Yield down -16 basis points on the wk to -10% already for the YTD!

- Commodities (CRB Index) deflated another -1.2% on the week to start 2015 -1.9% YTD

- Oil (WTI) got slammed another -8.4% week-over-week to -9.4% already for 2015

- US and German 5yr Breakevens (#deflation risk proxies) both dropped to 1.18% and -0.19%, respectively

- European Stocks (EuroStoxx600) dropped -1.0% week-over-week to start 2015 -1.3%

No, there’s nowhere in our playbook that says “buy European stocks on valuation.” And thank god for that as country equity indexes like Italy and Spain dropped -5% and -6% (on the week!), respectively.

If you’re a Global Macro hedge fund, you should be slaying the alpha beast right now. Imagine just being Short Euros, European Stocks, Oil, US Energy and Industrials… with the Long Bond and some Healthcare/Staples/REITs action on the long side?

Sadly, Consensus Macro funds can’t. Here’s where they were position from an options perspective going into the end of last week (CFTC Non-Commercial futures/options positioning):

- SPX (Index + Emini) net LONG position got +31,658 LONGER last week to +170,240 (vs the 6mth avg of +14,575)

- 10yr Treasury Bond net SHORT position got +17,379 smaller last week to -250,163 (vs the 6mth avg of -72,383)

Forget generating alpha, having those levered (options) positions on issued some seriously negative beta. And we’re quite happy you made money on the other side of that, fading the crowd, doing Cross-Disciplinary Macro, Hedgeye-style!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.88-2.07%

SPX 1995-2090

FTSE 6321-6579

VIX 15.69-21.89

EUR/USD 1.17-1.19

Oil (WTI) 46.01-50.99

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer