Who says that September is a seasonally slow month? 57% y-o-y revenue growth suggests otherwise.

The hot streak we saw in August continued throughout the month of September. September revenues were up 57% with VIP revenues leading the charge with 71% y-o-y growth, Mass grew 27% and slot revenue increased 24%. A pick up in the growth rate is no surprise since September 2008 was the first easy comp where y-o-y growth turned negative. The easy comps will continue through June 2010.

September is typically a seasonally slow month for many reasons including back-to-school season and junkets and players saving dry powder for Golden Week. However, it seems that this September didn't experience that seasonal slowdown due to a number of factors including easy comps, looser visa restrictions, stock market rally, new supply additions, and stimulas pumped into the chinese economy. While still early in the month, indications in the press suggest that the strength we saw over the last two months is continuing in October.

The rising tide lifted all ships in September, however MELCO and SJM seemed to be the greatest beneficiaries of this hot month. See below for details on y-o-y performance and market share changes.

Y-o-Y Property Observations:

LVS table revenues up 8%

- Sands was up 10%; with 13% growth in VIP win and 5% growth in Mass

- VIP RC decreased at Sands (~28%), however hold comparisons were very favorable

- Venetian was up 6%; all the growth came from Mass which was up 15%

- VIP RC (Rolling Chip) was up 12% but hold was down

- Four Seasons was down sequentially from August but still more than doubled revenues from last year to $28MM

Wynn table revenues were up 16%

- Mass was down 9%, offset by a 23% increase in VIP

Crown table revenue grew a whopping 244%, with both properties exhibiting strong results

- Altira was up 39%, however September 2008 was a very easy comp given the sub 2% hold

- Hold was below normal at Altira, around 2.6%

- CoD continued to ramp with total revenues growing 32% sequentially to an estimated total of over $145MM

- Unfortunetly Mass ramp continued to be slow, we estimate $18MM

- VIP RC grew 5% sequentially, despite September being a seasonally weak month

- September was another good hold month for the property

SJM continued its winning streak, with table revenues up 87%

- Mass was up 40% and VIP was up 125%

- L'Arc opened September 21rst with roughly 100 Mass and 50 VIP table

- SJM revenues should continue to stay strong with the addition of Oceanus in either Dec or early Jan

Galaxy table revenue was up 57%, mostly driven by a 70% increase in VIP win

- Starworld continued to perform well with table revenue up 74%, soley driven by 92% increase in VIP revenues

MGM table revenue was up 42%

- Mass revenues grew 30%, while VIP grew 47%

- Sequentially results were 34% lower than July & August, partly due to sequentially lower hold (which was still materially better than what MGM held in Sept 2008)

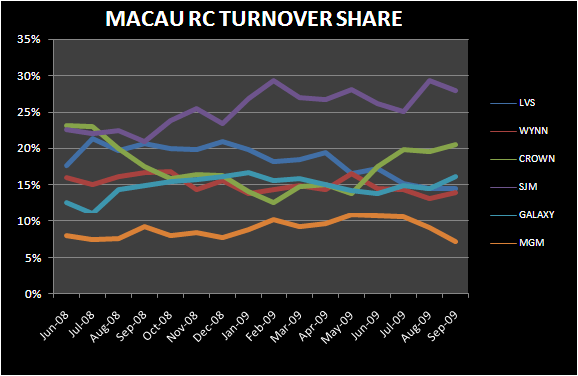

Market Share:

LVS' share decreased to 20% from 24% in August

- Sands' share increased to 8% from 7% in July

- Venetian & FS' share decreased to 11.3% to its lowest share month since March 08 from 17.1% in August

- However, all the share loss was in lower margin VIP which plunged from 16.5% to 8.9% sequentially

- Mass share was flat m-o-m at 18.5%

WYNN's share increased to 13.8% from the low's of 12.6% in August

Crown's market share was 17.5%, up from 16.2% in August

SJM's share increased for the second month in a row to 31.5% from 26.4% in August

Galaxy's share eeked back to where it was in July to 10.6% from 10.1% in August

MGM's share decreased to 7% from 10.5% in the prior month