Decision day is now FINALLY behind us: ECB President Mario Draghi left rates unchanged but delivered the “drugs”, delivered “more cowbell”, delivered the QE biscuit, however you want to put it.

Here’s a quick overview of the minimal details disclosed on the €1.1 Trillion QE package (beating market expectations of ~€600 Billion).

- The ECB expands purchases to include bonds issued by Eurozone central governments, agencies, and institutions in the secondary market against central bank money

- In theory, the institutions that sell the securities can use the funding to buy other assets and extend credit to the real economy

- Combined monthly asset purchases is set at €60 Billion

- The program will include the ABS and Covered Bond purchase programs issued last year

- The purchases are intended to be carried out until at least September 2016 and until the ECB sees a “sustained adjustment in the path of inflation” towards its goal of 2%

- The sharing of losses (pooled) will equate to 20% of the program

Our Take-Aways:

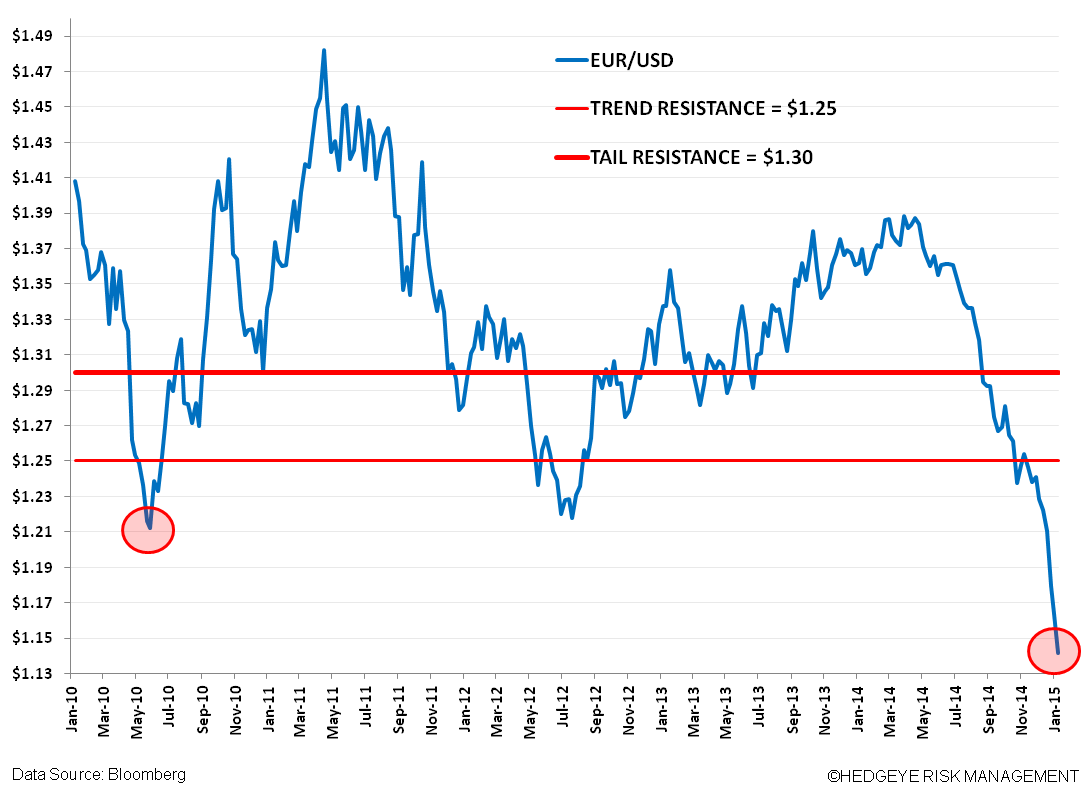

- The package signifies the Bank’s intention to maintain a weak EUR/USD [although Draghi would never state this publically]

- We think there “isn’t a hope on this side of central planning hell” that Draghi gets 2% inflation which should help solidify a weak EUR/USD and guarantee an extension of this existing package and future QE packages (sound familiar to Federal Reserve measures?). Additionally see our chart below on the correlation between the EUR/USD and oil

- Economically we do not see the Eurozone escaping the #deflation trap on Draghi’s QE wand and expect the feedback loop of the “necessity of certain member states to carry out country-level reforms” to persist (resulting in no improvement) over the medium to long term

- The lack of shared (pooled) losses is likely a nod to the German camp (which itself was against QE from the start)

Shorting The EUR/USD: Head’s You Win; Tail’s You Win

As we outlined in our note More Cowbell! A Roadmap Ahead of the ECB’s Thursday Meeting we called for a scenario of shorting the EUR/USD with the byline “Head’s You Win; Tail’s You Win”. Intraday following Draghi’s remarks the cross has been down as much as -1.6%, pressing the $1.14 level. In short, Draghi DID in fact deliver the drugs, and we foresee a combination of forces maintaining downside pressure on the cross:

- The package is both 1) above market expectations of ~€600 Billion and 2) above Draghi’s claim last year to expand the ECB’s balance sheet by €1 Trillion

- The move in the EUR accurately reflects a region plagued by deflation and stagnation

- We expect a stronger USD and weaker oil to continue pushing the EUR lower

- We expect anticipation about the need for future QE packages to push the EUR lower

- We expect an ECB bent on the export fruits of a weak EUR (backed by the Germans) will continue to perpetuate weak EUR/USD policy given the Bank’s lesser ability to impact the inflation rate

Matthew Hedrick

Associate