This note was originally published at 8am on January 08, 2015 for Hedgeye subscribers.

“All fixed patterns are incapable of adaptability. The truth is outside of all fixed patterns.”

-Bruce Lee

For those of us who embrace the non-linearity and uncertainty of Global Macro markets, how good is that quote? I can’t believe it took me this long into my career to find it. The more I read, the less I realize I really know.

Non-fixed market patterns. They are dynamic and constantly testing consensus narratives. Some of the best Bayesians in our profession get this. While they aren’t in the business of providing us their #process, they do make a lot of money front-running market truths.

“In 1993, Renaissance Technologies hired away from IBM a Bayesian group of researchers… searching for nonrandom patterns that will help predict markets, RenTech gathers as much information as possible. It begins with prior knowledge about the history of prices and how they correlate with eachother…” –The Theory That Would Not Die (pg 237)

Back to the Global Macro Grind…

What an excellent start to 2015! It’s been years since I’ve seen so many great long and short ideas across the Global Macro universe. If your portfolio mandate is diversified and flexible (across asset classes), I think you can have a crusher of a year!

Pardon? Yep, those who have been chasing single-factor #MovingMonkey models aren’t quite down with my optimism. But hey, I’m an optimistic guy – I’ve always thought that those who evolve their #process and adapt the fastest will ultimately win.

At 1PM EST today I’ll review our Global Macro Themes for Q1 of 2015 (ping sales@Hedgeye.com if you’d like access). In customary hash-tag style, our current themes are as follows:

- Global #Deflation: Amidst a backdrop of secular stagnation across developed economies, we continue to think cyclical forces (namely #StrongDollar driven commodity price deflation) will drag down reported inflation readings globally over the intermediate term. That is likely to weigh heavily upon long-term interest rates in the developed world, underpinning our bullish outlook for U.S. Treasury bonds (TLT, EDV, ZROZ, etc.)

- #Quad414: After DEC and Q4 (2014) data slows, in Q1 of 2015 we think growth in the US is likely to accelerate from 4Q, aided by base effects and a broad-based pickup in real discretionary income. We do not, however, think such a pickup is sustainable, as we foresee another #Quad4 setup for the 2nd quarter. Risk managing these turns at the sector and style factor level will be the key to generating alpha in the U.S. equity market in 1H15.

- Long #Housing?: The collective impact of rising rates, severe weather, waning investor interest, decelerating HPI, and tighter credit capsized housing in 2014. 2015 is setting up as the obverse with demand improving, the credit box opening and 2nd derivative price and volume trends beginning to inflect positively against progressively easier comps. We'll review the current dynamics and discuss whether the stage is set for a transition from under to outperformance for the complex.

While commercializing my research and risk management process will continue to take time, after 7 years of doing this from an independent research provider perspective, I think we’ve made significant progress.

They key word in that statement is we.

Our Macro Team is not only up to 6 analysts at this point – they have matured into a very cohesive unit of selfless grinders who not only work very well together, but question one another’s premise, so that we keep finding ways to front-run consensus market truths.

As legendary Macro maven Ray Dalio likes to ask, “what is the truth?”

Well, on yesterday’s US stock market bounce:

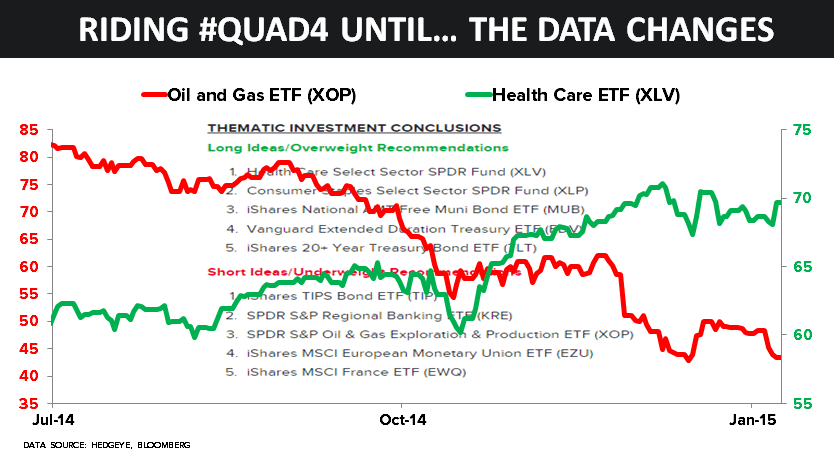

- Healthcare (XLV) led the rally +2.4%

- Consumer Staples (XLP) wasn’t far behind at +1.7%

- And Energy Stocks (XLE) continue to suck wind (+0.2%)

And, if all you do is US Equities, that’s precisely the Macro Playbook (ask sales for our daily note on that with Top/Bottom 5 ETFS, long/short) we have for you while we are still in #Quad4 reporting season (December and Q4 GDP data all gets reported in January).

As we roll out of that into Q1, we think you should be tilting to early-cycle (LONG) and late-cycle (SHORT). I’ll explain both asset-class-rotation and catalysts/timing as best I can on our 1PM call today. We hope you can find the time to dial in.

If I’m wrong on the timing and patterns of behavior born out of my macro calendar catalysts, I’ll do the only thing a humble servant to Mr. Macro Market knows – adapt to the prior, so that I can best position for the next posterior.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.91-2.12%

SPX 1195-2046

Nikkei 16884-17488

YEN 118.11-121.27

Oil (WTI) 47.22-52.63

Gold 1195-1225

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer