KEY POINTS

- PROHIBITIVE COST STRUCTURE: One of the major reasons why P hasn’t expanded internationally past Australia/New Zealand comes down to cost. There isn't a royalty-setting board internationally, meaning P would need to negotiate on an individual label/country basis on licensing rates, which the company currently deems as "prohibitively expensive".

- LOWER MONETIZATION POTENTIAL: Much smaller international ad budgets vs. a much larger internet population means each International user is worth considerably less than a domestic user. In short, sell-through would prove more challenging, and Ad RPM would be inherently limited.

- TOO MUCH RISK AT HOME: We don’t believe there is a viable and material international opportunity for P outside of potentially Australia/New Zealand. But even if there was, any further expansion would be dependent on a favorable outcome on Webcaster IV. As we’ve mentioned previously, anything short of a best case scenario on that front could derail P’s entire business model.

PROHIBITIVE COST STRUCTURE

The international opportunity is something the sell-side has been touting for some time, but has yet to come to fruition for P outside a small venture in Australia & New Zealand. One of the major reasons is cost. According to P’s filings, the company suggests that international expansion could be prohibitively expensive and not commercially viable.

One of the major reasons is that is there is no statuary licensing entity comparable to the CRB internationally. That means P would have to enter into direct license agreements with performing rights organizations/copyright owners in order to stream music; something it hasn’t been able to do domestically that would likely prove more difficult/costly on a individual label/country basis. We can debate the merits of whether P will ever be able to negotiate reasonable royalty rates, or we can point you to the bigger issue…

LOWER MONETIZATION OPPORTUNITY

We initially published this analysis for TWTR, but it applies to P as well. In short, the international user is worth considerably less in terms of per-capita advertising spend, which is the source of ~80% of P’s current revenues.

The math is fairly simple. International digital advertising spend is considerably lower than that of the US, but there are considerably more international internet users. In turn, the ad monetization potential is considerably less for each international user than it is for domestic users; making sell-through on those listener hours tougher to achieve, and the ultimate RPM (revenue per thousand listener hours) that much lower.

TOO MUCH RISK AT HOME

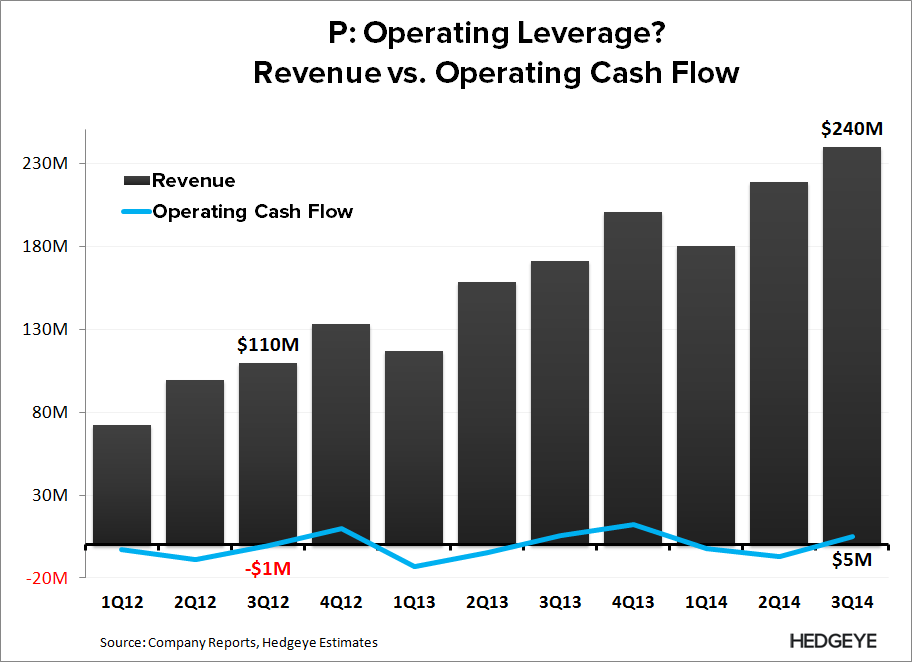

It’s important to remember that P is a marginally profitable company (at best), that hasn't been able to achieve operating leverage to date. P’s model can barely support its domestic operations, so any further international investment would just lead to heightened cash burn.

More importantly, Webcaster IV remains a overhang into 2016. The major point of contention is P’s ad-supported royalty rate, which applies to roughly 90% of its listener hours, of which, P is monetizing less than half of them. P and SoundExchange are worlds apart on what they are seeking, so anything short of a best-case scenario for P could derail its entire business model. That likely means P would have to to curb usage, either through more stringent listener caps or market exits altogether. See the note below for more detail.

P: Webcaster IV = Powder Keg

01/13/15 02:49 PM EST

We don’t believe there is a viable and material international opportunity for P outside of potentially Australia/New Zealand. But even if there was, P isn’t likely to expand internationally unless it receives a favorable outcome on Webcaster IV. And even if that were to happen, expansion would be a slow process that wouldn’t start until 2016 at the earliest, with monetization more likely a 2017 event at the very earliest. Long-story short, we wouldn’t bet on the international story.

Let us know if you have any questions, or would like to discuss further.

Hesham Shaaban, CFA

@HedgeyeInternet