Chinese Auto Industry executives are worried about swelling capacity. They should be.

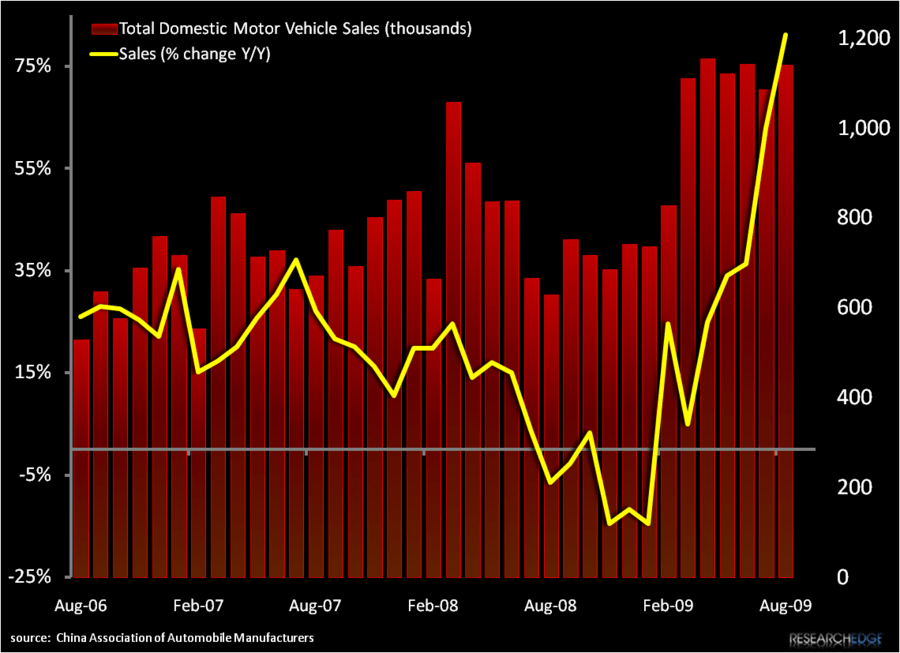

The CEO of China Auto Logistics was quoted yesterday saying that the 40% increase in auto sales in China this year, which has brought the total new cars sold to over 1 million per month, was a “one-time event”. We agree with this assessment. The stimulus measure which drove these sales, particularly the tax incentives for rural buyers, created a lot of “replacement” sales: farmers and rural tradesmen trading up from ancient vehicles. The pace of those types of buyers coming to market should decline as we head into next year, but as the euphoria of the stimulus fades and “real” demand kicks in, we expect auto sales growth to continue at a healthy pace even if it looks weaker on a year-over-year basis compared with this year’s flood of purchases.

The critical question now is whether a moderation in the pace of sales growth will reveal excess capacity after a massive wave of investment by domestic and foreign JV producers. Any supply glut could create a chain reaction through the industrial complex. Officially, the National Development and Reform Commission estimates domestic automotive industry capacity utilization at 80% with a drop to 70% projected by 2013 as more new plants come on line.

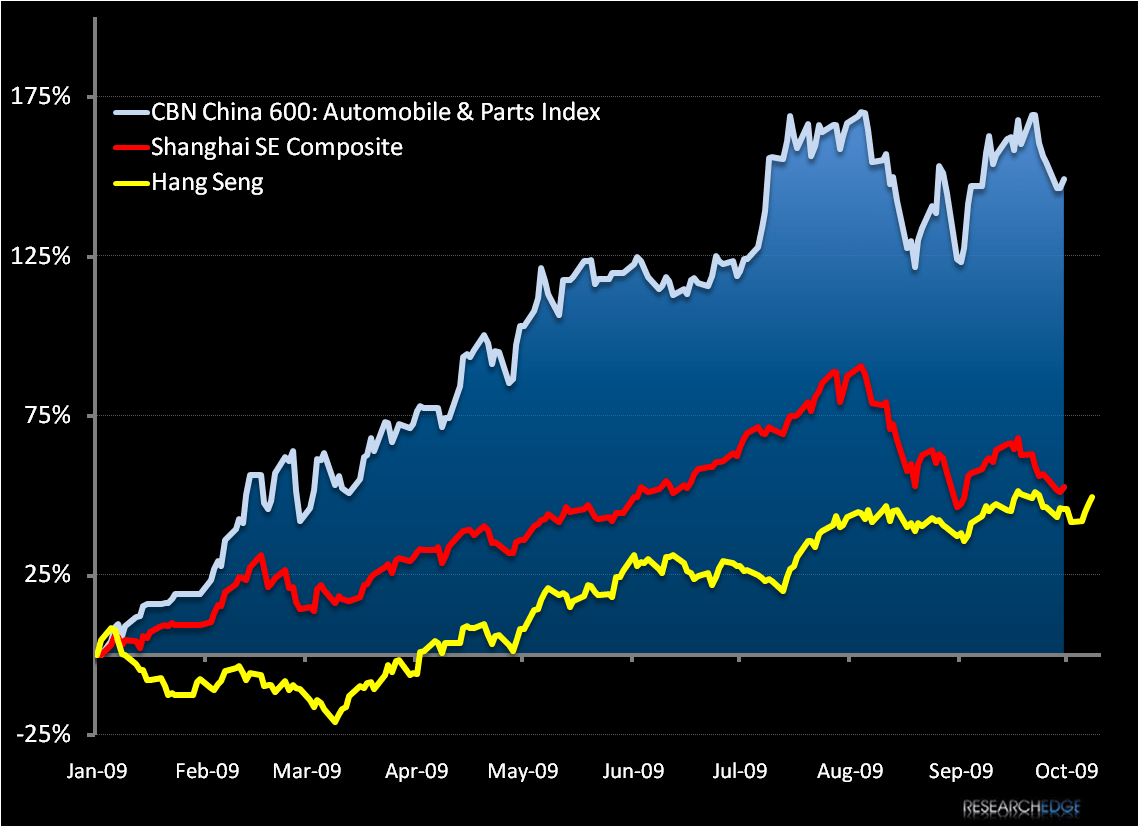

The Beijing plans outlined in Q1 called for consolidation that would alleviate some of these issues by creating a handful of dominant producers who control the entire manufacturing process internally rather than the present diverse network. Any M&A cycle inside the Chinese automotive industry would be a welcome source of capacity reduction, but we see it as unlikely that new efficiencies through consolidation will be sufficient to offset the tide of diminished expectations as monthly sales figures comp to impossibly high 2009 levels. As such, the DBN 600 Automotive Sub Index current level appears likely to be unsustainable in the intermediate term after a 150% increase YTD and we are inclined to shift the group out of our industry focus group for Q4.

Land of Opportunity

The strategies adopted by US and European JVs pursuing market share in the Chinese market have produced predictably mixed results to date, and recent developments suggest that some (primarily the US firms) will continue to flounder.

With under 3% of the total market Ford is playing catch up with the announcement of a third plant with partner Chonqing Changan to be on line by 2012 which will lift total annual capacity on the mainland to 600,000 units. Given the macro factors outlined above, and the fact that the focus segment –the compact market, is so heavily competitive, this growth strategy appears to be too little too late. In contrast, French producer Peugeot Citroen has recently announced that its plan to construct a third facility citing looming excess capacity.

The luxury import segment has become lucrative enough for European manufacturers to start building domestic production facilities –with the Audi/FAW JV reportedly considering a plan to begin complete A3 and A5 production on the mainland. Audi has had great success in China on the heels of Parent VW’s early and successful entry into the market there .

NOTE: Domestic Chinese Markets have been closed for the first 3 sessions of this week in observance of National Day and the Mid-Autumn celebration.

Andrew Barber

Director