An analysis of the latest weekly Macau numbers

call to action

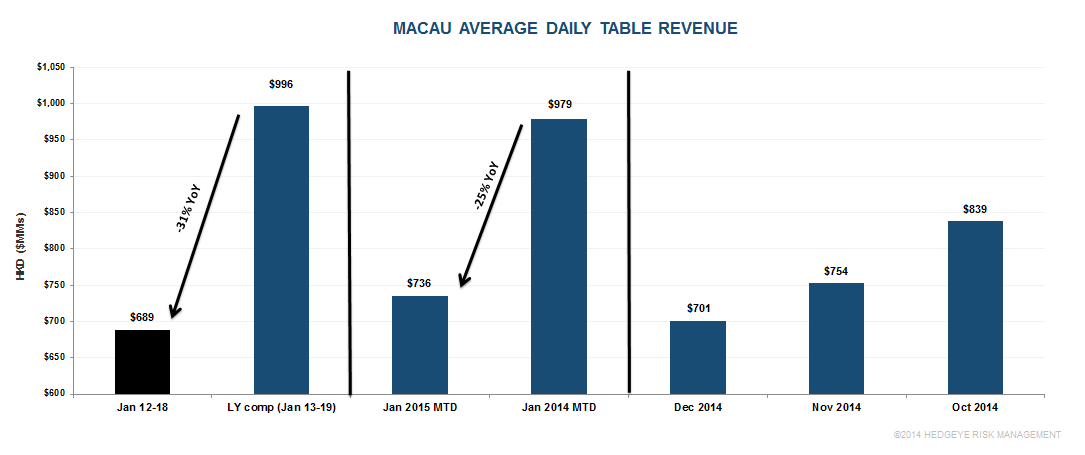

The third week of January displayed continued deterioration in already soft table revenues. We're now forecasting full January GGR to fall 15-21% YoY. That's a bad month but looks even worse when considering that January 2014 is the easiest comparison until June. Despite a basing in the Macau stocks, the fundamentals continue to worsen with no visibility of a turn.

the latest numbers

The weekly numbers are out for last week and they aren't pretty, albeit against a difficult comparison. Daily table revenues averaged HK$689 million, down 31% from the comparable week of last year. Unfortunately, January 2015 faces the easiest comparison (+7% in January 2014) until June, yet table revenues are trending down 25% month to date. Due to an easy comparison in the last week of January, the YoY decline should lessen.

market shares

Wynn Macau, MPEL, and Galaxy continue to outperform here in January. Relative hold percentages are likely playing a role. Wynn may also be benefiting from bad luck the last 2 months which from the player's perspective would mean good luck and a lucky place to visit. LVS is really struggling and we suspect the elimination of phone proxy betting is contributing. We wouldn't be surprised to see LVS and/or Wynn Macau reinstate proxy betting. Stay tuned.

2015 forecast

We don’t expect to see positive growth in GGR until Fall 2015, absent any big hold months.

conclusion

We remain generally negative on the Macau operators but acknowledge the potential for another relief rally immediately following earnings. MPEL looks like a potential winner - or at least a non-loser - this earnings season and remains the only Macau company where we are projecting a beat, albeit very small. We remain below the Street for 2015 for all of the Macau operators, despite the recent estimate reductions.