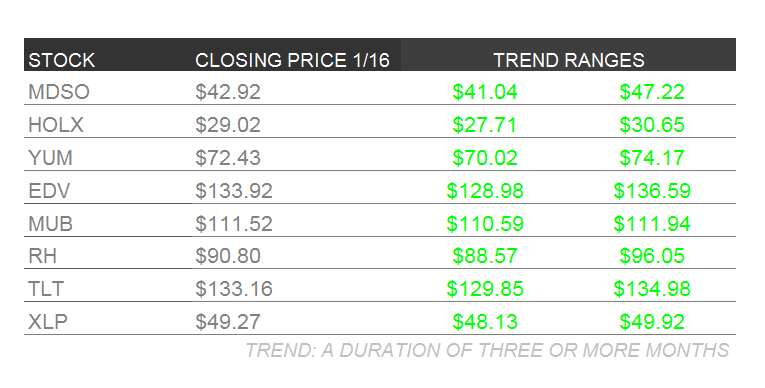

Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Currency War? It's game on as Switzerland roils markets around the globe.

IDEAS UPDATES

MDSO

We presented our bullish thesis on Medidata Solutions to institutional clients on a Best Idea Long call yesterday. While stock performance has been disappointing since we added it to Investing Ideas, there has been no change to our fundamental bullish thesis and intermediate valuation target of $65. We would remind subscribers that MDSO is a small-cap, growth company that often exhibits higher volatility (higher beta) than the broader market.

Medidata’s revenue is derived from the # of active clinical trials and the share of those trials that are being conducted on Medidata’s cloud-based platform. What we are seeing when we track the number of trials first received (leading indicator for new trials), is a substantial acceleration in growth through 2014. This pickup in growth and activity more broadly, is consistent with the positive commentary we heard from management on earnings calls for much of the year.

Macro Monitor identified these clinical trial data series as having an extremely high correlation to the y/y rate of change (ROC) in application services revenue on a two-quarter lead. As you can see from the image below, theses series (which drive our model) point to a material acceleration in revenue growth through the first quarter of 2015. When we convert this growth into dollars, the results are estimates that are much higher than consensus. While management has not formally announced an earnings date, we believe they will report in the first week of February (same period as last year).

TLT | EDV | XLP | MUB

Long Bond, Long Money

Another week, another big bag of cash delivered to investors on the long side of the long bond:

- TLT: up +1.6% WoW

- EDV: up +2.2% WoW

- MUB: up +0.4% WoW

- XLP: up +0.3% WoW

Contrast those returns with that of the S&P 500: down -1.2% WoW.

For 2015, the gap between the TLT and the SPY is cavernous; even a former offensive lineman like myself can fit through the spread without turning sideways:

- TLT: up +5.8%

- SPY: down -1.9%

Reviewing our Investing Ideas update from last week:

“If the DEC Markit and ISM Composite PMI data is of any indication, the preponderance of DEC high-frequency growth data will continue to slow as we progress throughout the month of January.”

Much like its SEP counterpart which precipitated the 10/15 swoon in both stocks and bond yields, the DEC Retail Sales print stole the show as it pertains to this week’s domestic high-frequency growth data:

- Total YoY: +3.2% from +4.7% in NOV

- Total MoM: -0.9% from +0.4% in NOV

- Control Group (i.e. the portion of retail sales that feeds directly into GDP) YoY: +3.2% from +4.3% in NOV

- Control Group MoM: -0.4% from +0.6% in NOV

“If the DEC Average Hourly Earnings data from Friday’s Jobs Report is any indication, the trend of reported disinflation will continue when we get the DEC CPI data next Friday”:

- Headline CPI YoY: +0.8% from +1.3% in NOV

- Headline CPI MoM: -0.4% from -0.3% in NOV

- Core CPI YoY: +1.6% from +1.7% in NOV

- Core CPI MoM: unchanged from +0.1% in NOV

Reviewing our 12/19 note titled, “DOES YOUR VIEW ON RATES INCLUDE THE RISK OF A “REFLEXIVE DEFLATIONARY SPIRAL”?”:

“The buy-side is perhaps even more bullish on rates (i.e. bearish on Treasury bonds) at the current juncture. The net SHORT position of 215k 10Y Treasury note futures and options contracts is the widest net SHORT position since April of 2010. On a TTM Z-Score basis, which we use to show deviations that are typically indicative of crowded trades, the buy-side hasn’t been this net SHORT of long-term Treasuries since March 2012, October 2011 and April of 2010. The subsequent draw-downs in the 10Y Treasury note yield from those peaks in bearish sentiment are -99bps, -45bps and -160bps, respectively.”

Since 12/19, the 10-year Treasury yield has fallen -33bps. The median and average of the aforementioned draw-downs (in bond yields) hover around -100bps.

We’re not prophets. We’re not magicians. We’re just a group of reasonably intelligent people with a repeatable investment process and we hope we can continue to add value to yours.

RH

Restoration Hardware announced on its 3Q earnings call the four new Full Line Design Galleries we can expect in 2015. The markets are as follows: Chicago, IL, Tampa Bay, FL, Denver, CO, and Austin, TX.

The Street 'gets it' that the economics in these stores are significantly better than in the legacy 9,000 ft stores. But there are massive questions (and doubts) about the economics associated with a mega-store like what RH built in Atlanta.

Here are some reasons we think RH’s new bigger footprint format makes sense.

- As we outlined in our RH Real Estate Deep Dive, you need to look at market size of every single store -- which we define as home furnishings spend for consumers earning over $100,000. We did that in every single region RH operates.

- Our math suggests that there are 66 existing RH markets that could support locations 45,000 sq. ft. or greater. This assumes 2018 market share of 10%, and sales productivity of $1,200.

- Of these 22 locations, Atlanta is #3 on the list, behind New York and Houston, Chicago 17, Tampa Bay 44, Denver 11, and Austin 34. Our math suggests RH could have a store size as great as 90,000 feet.

- The rent economics work. Relative to RH's existing Legacy properties, we think that occupancy math lines up well as RH transforms its real estate portfolio.

YUM

We believe YUM has an under-leveraged balance sheet, highlighted by the recent Burker King (BKW)/Tim Hortons (THI) merger. We ran through this recently in a presentation for institutional investors back in December.

Here's the bottom line: if YUM were to leverage its balance sheet, it would have the ability to repurchase a significant amount of stock or pay a large special dividend.

As we wrote last week, this is a stock that continues to trade at a significant discount to its intrinsic value, making it one of our favorite long-term buys in the restaurant space. We wouldn’t be surprised to wake up one day to news of a prominent activist buying up shares of YUM. There’s simply too much value here to ignore and the stock’s multi-year underperformance is not going unnoticed. Learn to ignore the day-to-day volatility and prepare yourselves to own this stock for the long haul.

HOLX

We thought Hologic would have a good quarter. They did. Expect it to continue.

HOLOGIC PREANNOUNCES POSTIVE

We thought Hologic would have a good 1Q15 based on stable trends in Pap/Thinprep (table below), positive patient volume trends during the quarter, and breakout 3D Tomo sales. Consensus had come to rest at $632M, the midpoint of company guidance of $625-$635 for F1Q15 (Dec). At the JP Morgan Healthcare Conference this week, HOLX pre-announced revenues of $653M, well above the guidance range.

Most of the beat versus consensus came within Diagnostics at $304M (vs $295M), but Breast Health was also strong at $242M (vs $236M) as was GYN Surgical $84M ($80M). Based on our model, we expect further upside throughout 2015.

s-curve forecast

Using three data points we derive our monthly forecast curve using an s-curve methodology. The analysis minimizes the variance between actual placements (the monthly data charted above) and the prediction curve by adjusting s-curve inputs. The current variance between predicted and actual is currently 0.14%.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

oh canada! target shutters north of border

Closing Canada from a position of strength. Good move. But if former management could be so off on this call, what else could be buried here?

one step back for U.s. & two for energy states

Not a good sign if you make your living in energy states as they continue to see their labor markets decouple from the broader US trend.