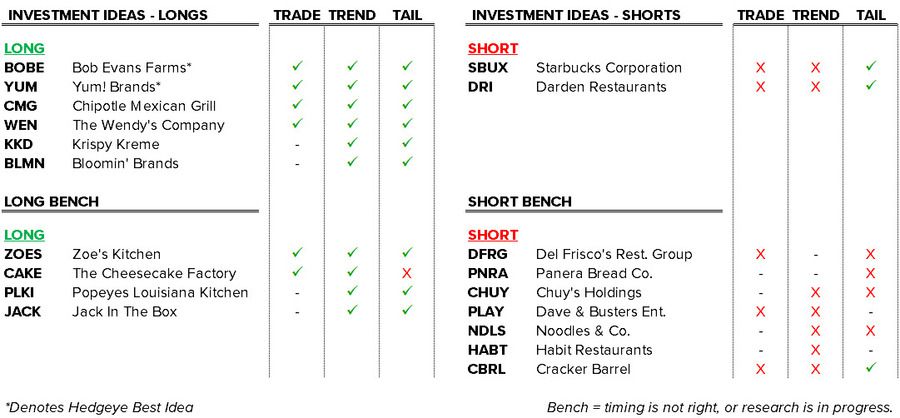

Long List

KKD – Prior to ICR, Krispy Kreme came out and reaffirmed FY15 EPS guidance of $0.69-0.74 and tempered expectations for FY15 EPS with guidance of $0.79-0.85. They also announced that TXRH CFO Price Cooper resigned to become the CFO at KKD. Cooper will succeed Douglas Muir, who has served as CFO of Krispy Kreme since 2007 and announced retirement plans last year.

The KKD story is powerful and one that we believe is being underappreciated by the street as it continues to invest for the future by focusing on 1) accelerating global growth 2) leveraging technology 3) enhancing the core menu and 4) maximizing brand awareness. Management has developed a flexible store model that will allow them to grow units at a double-digit rate for the foreseeable future. FY16 plans call for 11-13% unit growth (10-20 net new domestic units; 95-110 net new international units) and 10-18% EPS growth.

KKD is attractive to us for many reasons including its asset-light model, strong financial profile, compelling unit economics, strong FCF generation, impressive returns on incremental invested capital, feasible growth strategy, and established international presence.

Long Bench

ZOES – Differentiated, young concept that has identified its ‘niche’ in the fast casual category. Out of the most recent IPOs, this is the one we like the best as it is truly a unique concept that largely appeals to educated, affluent women and their families. Despite only having 132 locations in 15 states, ZOES has specifically identified 1,600 locations where the concept could work domestically and has three types of restaurant models to choose from (end-cap; free-standing; in-line). We like ZOES for its management, unique concept, attractive unit economics, impressive comps, and growth potential but are currently hesitant to add it to the Long List due to its rich valuation.

PLKI – Popeyes came out before ICR and pre-announced 4Q global comps of +9.8%, well above consensus estimates, and indicated full-year adjusted EPS would fall in-line with the street at $1.64-1.65 – good for 15% growth.

As many of you know, Popeyes was one of our favorite stocks throughout 2014. CEO Cheryl Bachelder has done an outstanding job since assuming her position in late 2007 and has positioned the company for tremendous domestic and international growth moving forward (double U.S. footprint; untapped international opportunity). PLKI’s commitment to its franchisees is not only admirable, but also paying dividends.

We recently pulled PLKI from our Long List given the current valuation, but are ready and willing to add it back given a notable pullback. The fact of the matter is, this is one of the best run companies in our space and investors have ample visibility into the company and its operations given its asset-light model, diversified revenue steam and stable cash flows.

JACK – JACK was another one of our favorites on the long side in 2014 that we recently moved down to the Long Bench due to the recent run it has benefitted from. We first turned bullish on JACK in early 2012, given the potential inherent in the Qdoba brand. Since then, CEO Lenny Comma has a tremendous job running the company while Qdoba President Tim Casey has successfully reignited comp growth at the brand. Management put to rest any speculation that Qdoba will soon be spun off, due to the fact that the street is (finally) properly recognizing the concept for the growth vehicle that it is.

We still like JACK and believe they’ve identified feasible opportunities to drive margins moving forward (shared services model), but are hesitant to champion the stock at current levels. The stock very well could find itself back up on our Long List at some point, but we’d likely need to see a notable correction first.

Short Bench

DFRG – Del Frisco’s found itself on our Short List in mid-2014 as we found street estimates to be far too aggressive and refused to credit the Grille as being a viable growth concept. To be frank, we we’re waiting for easy comparisons to pass before re-shorting this one, but may have tried getting a little too cute in regards to timing. The stock has been hit hard the past couple of days after revealing soft margins in the Class of 2012 and 2013 Grille restaurants, reaffirming our view that this concept is not ready to grow 38% next year.

Management predictably touted the company’s portfolio of brands, suggesting it allows them flexibility in what they need to do to grow – you likely know where we stand on that. It’s become clear to us that 1) Sullivan’s can’t grow 2) the Grille isn’t ready to grow (and may never be a viable growth vehicle) and 3) the Double Eagle Steakhouse can only grow at a rate of one restaurant per year. With the street looking for 19% and 27% earnings growth in 2015 and 2016, respectively, this is a name that could find itself back up on our Short List in the near future.

CHUY – Akin to Del Frisco’s, Chuy’s spent some time on our Short List last year and could find itself back on it in 2015 after delivering, in our view, an underwhelming presentation at ICR. For starters, Chuy’s dialed back its expansion plans by one unit to 10-11. Second, and more importantly, Chuy’s scaled back expectations for new unit economics, as it decreased AUV and cash-on-cash return targets for its restaurants (down from $4.2mm and 40%, respectively, to $3.75mm and 30%).

We don’t deny that Chuy’s isn’t an overwhelmingly successful concept in its core market (Texas). We do, however, question the company’s ability to generate similar returns outside of this market. Chuy’s classes of 2012-2014 stores in immature markets have been ~50% less profitable than those in its mature market, but management insists this is a short-term phenomenon and will be corrected by its backfilling strategy.

Chuy’s development strategy, in which it is targeting long-term annual restaurant growth of 20%, calls for 1) the identification and pursuit of development in major markets and 2) “backfilling” smaller existing markets to build brand awareness. If you are long this stock, you are essentially betting that this expansion plan into new markets will go smoothly and that immature markets will mature well. That’s not a bet we’re willing to make and if the stock runs, we’ll be looking to re-short it.

NDLS – Very close to adding this name to our Short List. While it’s an intriguing, proven concept with an experienced management team, its first full-year as a publicly traded company was one to forget and, quite frankly, that’s exactly what the street has done – but we haven’t. Management’s 2014 guidance was woefully off-target and this year’s guidance is similarly unsettling. In 2015, Noodle’s expects to deliver:

- 12-14% unit growth

- 2.5-4% same-store sales

- ~25% earnings growth (consensus at 27%)

To be clear, the chances of this happening are slim. Yes, industry sales are currently strong, but we’d be foolish to expect this trend to continue throughout all of 2015. And, if our memory serves us correctly, the company is coming off a year in which it delivered 0% earnings growth. For the street to assume the company will grow earnings 27% and 30% in 2015 and 2016, respectively, is mind-boggling. We don’t see NDLS hitting its numbers this year, which suggests the stock is even more expensive than investors think. Trading at 56x an inflated forward earnings number, management has no room for error.

HABT – The Habit Burger Grille is a better burger concept with an impressive history of same-store sales, unit, revenue, and adjusted EBITDA growth. We like the operations-focused management team and believe the company has a strong enough infrastructure to support its growth. All-in-all, it’s an impressive concept. But, it’s a small concept and it plans on growing rapidly (over 20%+) for the foreseeable future.

Aside from an egregious valuation, what concerns us most about HABT is the declining returns on invested capital it expects to realize during its expansion. While existing units are generating average unit volumes of $1.7 million and 40% cash-on-cash returns, management expects new units to generate average unit volumes of $1.5 million and 30% cash-on-cash returns – and there’s no guarantee these numbers don’t move lower as Habit begins to saturate markets. It’s a viable concept that’s in the early innings of an aggressive expansion plan; one that typically doesn’t come without a fair amount of hiccups. When you’re stock is trading at 257.26x forward earnings, you can’t have those.

CBRL – We actually think management is doing a good job running this company and did a good job articulating the Cracker Barrel story at ICR this week. CFO Larry Hyatt outlined the company’s properly aligned strategic priorities: 1) extend the reach of the Cracker Barrel brand to drive traffic and sales 2) optimize average guest check through the implementation of geographic pricing tiers 3) apply technology and process enhancements to drive operating margins and 4) further grow the store base with the opening of 6-7 Cracker Barrel stores.

Cracker Barrel has rightfully been the direct beneficiary of the recent decline in gasoline prices (86% of its stores are off of highways), but we fear the stock may have gotten a bit ahead of itself. Family dining chains, in general, have done quite well lately as they generate comps momentum, but it’s unclear how long this will last. It’s not easy for us to poke holes in the Cracker Barrel story right now and 2015 EPS growth of 9% looks achievable. However, we can’t justify paying 21x forward earnings for a chain that is growing ~1% per year and has historically traded closer to 14x. It’s on our Short Bench until we identify a catalyst, one way or the other.

PLAY – The re-emergence of Dave & Buster’s brings back memories of the old, “big box” company that failed miserably as a public company. Will things be different this time around? Our inclination is to be very skeptical of the company’s growth trajectory, but there’s no denying that they are putting up compelling numbers. The PLAY model generates $10.3mm in AUVs per unit, with approximately 50% of its revenues from its restaurant and 50% of its revenues from its entertainment offerings ($5mm “Eat and Drink” revenue; $5.3mm “Play and Watch” revenue).

On the surface, PLAY’s valuation looks reasonable – trading at 10.7x EV/EBITDA. However, we have issues with this valuation metric considering it uses an inflated EBITDA number (the company has come up with its own definition of EBITDA) that adds back pre-opening costs, which we view as a real cost of doing business – particularly for a growth concept. Although the set-up for the first quarter looks fine, we’ll be keeping a very close eye on this one in 2015.