Wynn Macau will begin trading in Hong Kong tonight and it should be a successful first day. Thanks to some pretty in depth disclosure, we were able to build out a very detailed model. The model is available to clients upon request.

As expected, Wynn Macau’s IPO was a big success, as much as 10x oversubscribed according to numerous articles. The stock begins trading on the Hong Kong stock exchange tonight. According to our quick math, Wynn Macau looked attractive even at the top end of the pricing range (see: “WYNN MACAU IPO: CHEAPER THAN IT LOOKS” published on 9/29/09). Now that we’ve had some time to pour through the offering circular, we thought that we would share some further thoughts with you.

Our thoughts are broken into two sections: Projections and Fun Facts (for the other model geeks out there).

PROJECTIONS:

While our revenue model didn’t change, Wynn Macau provided loads of details on their cost structure, most of which we incorporated into our EBITDA calculation. Our new EBITDA estimates are net of royalty fees and corporate allocations and take into account the new commission caps. We assume the annual caps provided on page 127 of the preliminary circular for our corporate allocation calculations. We also assume that Wynn will pay an “all-in” junket commission rate of 41% (vs. the maximum of 44%).

Based on our estimates, Wynn Macau priced at 16x 2010E EBITDA and 15x 2011E EBITDA, which we believe is equivalent to an 11x and 10x tax adjusted multiple. Once Encore is complete, WYNN Macau should generate FCF in the range of HK $3.5BN and have zero net debt by the end of 2011.

FUN FACTS:

As we already mentioned, Wynn Macau’s circular provides a plethora of detail on the business and the cost structure in particular. Below is some supplemental information that we found interesting.

Promotional expenses:

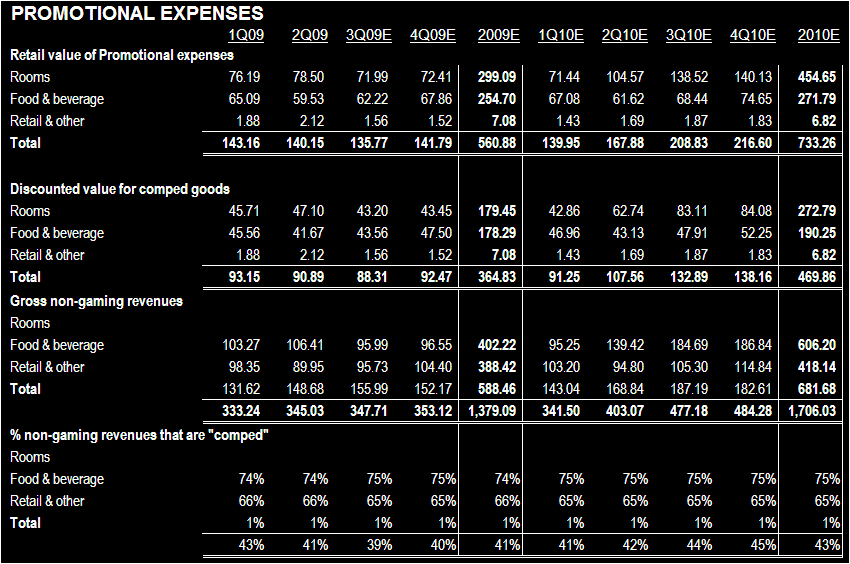

Unlike in the US, Wynn Macau’s revenues are already net of promotional expenses and discounts. This means that rooms, food & beverage and retail & other revenues do not include the retail value of complementary rooms provided to junket operators. Since opening, the percentage of rooms and food & beverage allocated to “comps” has steadily increased. For 1H09, 74% of the retail value of rooms and 66% of the retail value of food and beverage operations were “comped.” Retail & other is almost exclusively a cash business. For the purposes of junket commission calculations, rooms will be discounted by 40% and food & beverage will be discounted 30% from retail values.

Gaming premiums:

In addition to paying 39% of gross gaming win to the government of Macau, concession holders also pay fixed and variable gaming premiums based on the number of VIP / Mass tables and slots that a facility has. Wynn Macau pays a fixed annual premium of HK$29.1MM plus an annual charge of HK$291k per VIP table, HK$146k per Mass tables, and HK$971 per slot machine.

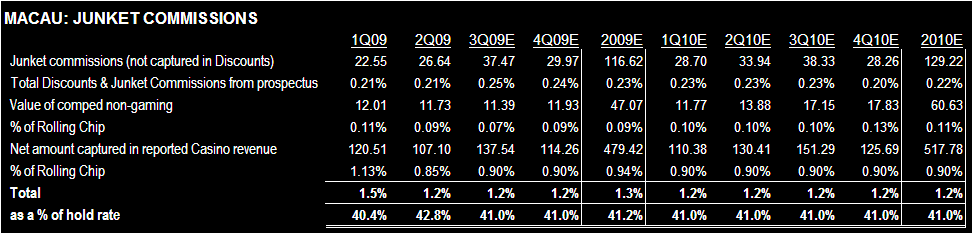

Junket commissions:

In the breakout of “Other Operating Expenses” in the appendix of the circular one can find junket commissions broken out. However, at first glance the number seems extremely low (roughly 0.2% of rolling chip). This is because “Casino Revenues” are already net of the portion of the junket commission that is a rebate to customers. To calculate the all-in commission rate that we all refer to, you need to include the rebate as well as the discounted value of “comped” rooms and food & beverage. We estimate that in 1H09 WYNN Macau paid an equivalent rate of 1.29% to junkets or 41.5% of gross win.