Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaways:

The big call-out this week remains the ongoing drop in yield spreads and commodity prices. The former puts pressure on the domestic banking market while the latter pressures the economies of select international economies like Russia. Sberbank saw swaps move out another 117 bps w/w as Fitch cut the sovereign rating to near junk. There's little indication thus far that the domestic banking market is pricing in rising international risk, but we think the risk/reward setup there remains unfavorable.

European Financial CDS - Fitch cut Russia's credit ratings to near junk territory. In response, Sberbank CDS swaps widened by a further 117 bps on the week to 726 bps. Greece saw its banks' swaps tightene w/w by an average 60 bps to the low-to-mid 800s. Elsewhere in Europe there was relatively little movement in swaps.

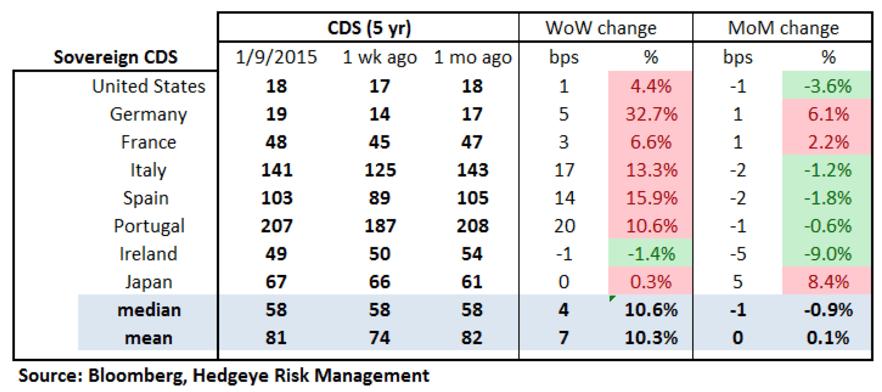

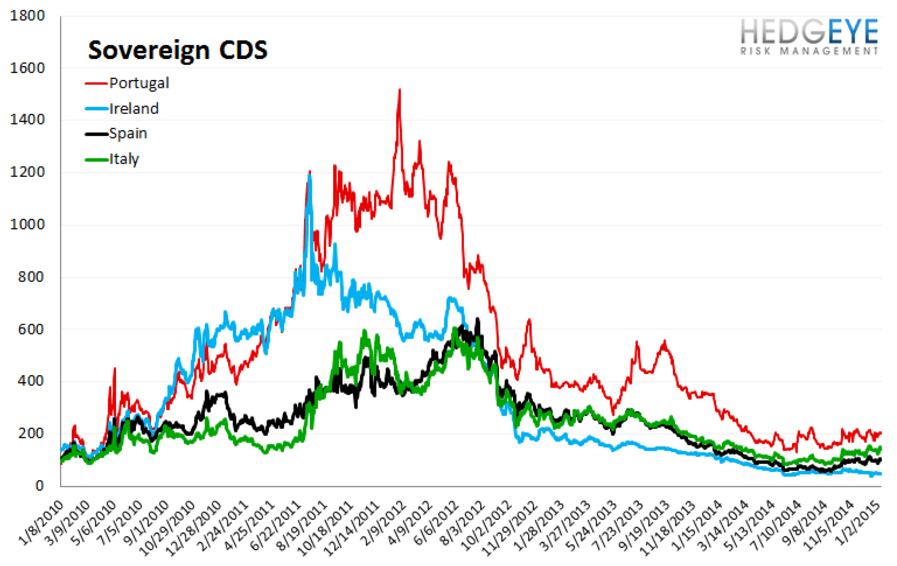

Sovereign CDS – Sovereign swaps mostly widened over last week. Italian, Spanish and Portuguese swaps rose 17, 14 and 20 bps, respectively on the week, though they are still down nominally on a month-over-month basis. The main event in the near term remains the Greek vote on January 25th.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst