Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

Please note we added Medidata Solutions MDSO earlier this week. Our Healthcare sector team presents a granular, deep-dive distillation into our bullish thesis below.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

mdso

SUMMARY

Down from its peak in March 2014 when all things cloud were working, MDSO's stock price has been cut in half and the short interest has doubled. When they report in early February we think they beat numbers and the shorts get squeezed.

Click to enlarge.

BACKGROUND

Business Model: Cloud-based clinical trial software

- MDSO sells cloud-based software on that helps customers manage clinical trials (electronic data capture, study design tools and clinical trial management systems)

- Customers include top 25 pharma, mid-market pharma/biotech, CROs, Government sponsored organizations.

- Paid on a per trial basis or fixed amount for high volume Enterprise clients.

- Subscription model provides high degree of visibility into revenue base, near 100% revenue retention and 90% customer retention. Mid 80% gross margin for Application Services.

History: Rise and Fall

- Founded in 1999 and went public in June 2009.

- Backlog and revenue growth accelerated in 2012/2013 and the stock went parabolic, peaking at $68.21 on March 4,2014 (up ~300% from its 2012 closing price)

- Subsequent 6 weeks the stock fell by 30% before the company missed 1Q14 earnings on April 22, 2014.

- Stock price bottomed on May 8th at $33.98, 50% below its peak.

- Company went on to miss Q3 earnings and lower 2014 guidance. Stock has since stabilized and is up 27% since last earnings report and 33% below its peak.

Consensus: Sellside bullish, shorts tend to be wrong

- Consensus is unanimously bullish on the name, with 12 out of 12 analysts rating MDSO a buy, despite both price targets and estimates coming down for 4Q14 and 1Q15.

- Consensus TAM estimates are likely too high, but should not matter over next 3-years. Consensus basing TAM off 150k+ registered clinical trials, only 40-60k active at given time.

- Short interest has been rising over the last 12 months rising to 12% if the float. Historically, high short interest is correlated with positive price performance.

- The sellside rating is in the upper range of its historical levels which is generally reflects positive forward price performance.

- Sellside estimates trended lower over the course of 2014, although revenue and EPS estimates have been stable over the last 3 months.

THESIS

1. Currently the stock screens long based on performance, earnings revisions and short interest. 50% peak-to-trough stock price decline driven by missed expectations (deal timing), guidance adjustment and fraudulent wire transfer*. We view recent weakness as buying opportunity given strength in leading indicators.

2. Macro Monitor identified the following series as two quarter leading indicators of y/y ROC in Application Services Revenue:

- NIH Award # - Epigenetic/TTM/Delta (0.93 RSQ) – Updated Monthly, HRM Calculated

- Genomic Clinical Trials Net Starts (0.94 RSQ) – Updated Monthly, HRM Calculated

- Customer y/y % (0.94 RSQ) – Updated Quarterly, Company Provided

3. $1.5 bill annual revenue opportunity based on current product mix ($409 mill ’15 Consensus Sales). Long-term model utilizing s-curve methodology tracking 50% market share based on 4,000 potential customers. Significant cross-sell opportunity with 12 products available, average product per customer (intensity) 2.4.

Combined, these key drivers point to a material acceleration in application services revenue through 1Q15 at a time when consensus sales and earnings estimates have been reduced.

*Fraud targeted certain mid-level employees in their finance department resulting in the transfer of $4.8 mill to a rogue overseas account. No customer data was involved in the matter and the company’s systems were not impacted or compromised. Management has reviewed internal controls and processes and implemented additional procedures to prevent future incidents. (Source: Q3 Prepared Remarks)

VALUATION

- Application Services Revenue y/y % ROC leads NTM EV/Sales multiple by two quarters (0.89 RSQ).

- Model results in NTM EV/Sales multiple of approximately 8.5x by 3Q15. Similar expansion can be applied to NTM P/E and NTM EV/EBITDA given correlation.

- Current price $46.40 – 6.0x EV/Sales

- $61 Stock Price - 8.5x HRM $429.7 mill ’15 revenue estimate.

- $72 Stock Price - 70x HRM $1.03 ’15 EPS estimate.

- $72 Stock Price – 40x HRM $107 mill ‘ 15 EBITDAO estimate

Figure 1: NTM EV/Sales Valuation Table

CATALYSTS

- Key Driver Update – February 2015

- 4Q14 Earnings Not Formally Announced – Reported 2/6 Last Year

- No other scheduled events/conferences

RISKS

- Slowdown in Clinical Trials – Medidata’s fundamentals are tied to the number of Clinical Trials being conducted and biotech/pharma activity in general. We have identified several, high-frequency leading data points (updated monthly) that should flag a slowdown before it shows up in the numbers.

- Failure to Cross-Sell/Attrition – We will monitor trends in customer intensity and have discussions with industry participants to get a better sense for cross-sell potential. We have identified several leading indicators of customer growth, although their significance is less than other factors we identified.

- Insufficient TAM – Core to the bear case is that the EDC market is small and MDSO is near saturation. In our opinion, Medidata has a diverse product offering and is no longer a ‘one trick pony’. Management indicated that Rave, their EDC offering has several years of +20% growth ahead of it. That being said, we do believe the TAM is considerably smaller than some think and plan on spending more time here. We will be speaking to industry participants, marking their customer growth to our model and tracking leading indicators.

- Increased Competition – Oracle/Phase Forward is the main competitor, however Medidata has been actively displacing them. While Medidata is the market leader and barriers to entry are relatively high, increase competition would dampen their long-term prospects.

- Regulatory Risk – Clinical trials are heavily regulated by the FDA and other federal agencies. Implementation of, or changes in existing policies in the U.S. or in any other country could disrupt Medidata’s customer base and/or require costly changes to Medidata’s software.

TLT | EDV | XLP | MUB

Bonds, Bonds, Bonds, Bonds, Bonds!

Amid a mixed week of domestic economic data, our slow-growth, yield-chasing trade of long TLT, EDV, MUB and XLP latched on the trend of #GrowthSlowing data throughout the fourth quarter:

- TLT: +2.95% WoW

- EDV: +3.77% WoW

- MUB: +0.88% WoW

- XLP: +1.57% WoW

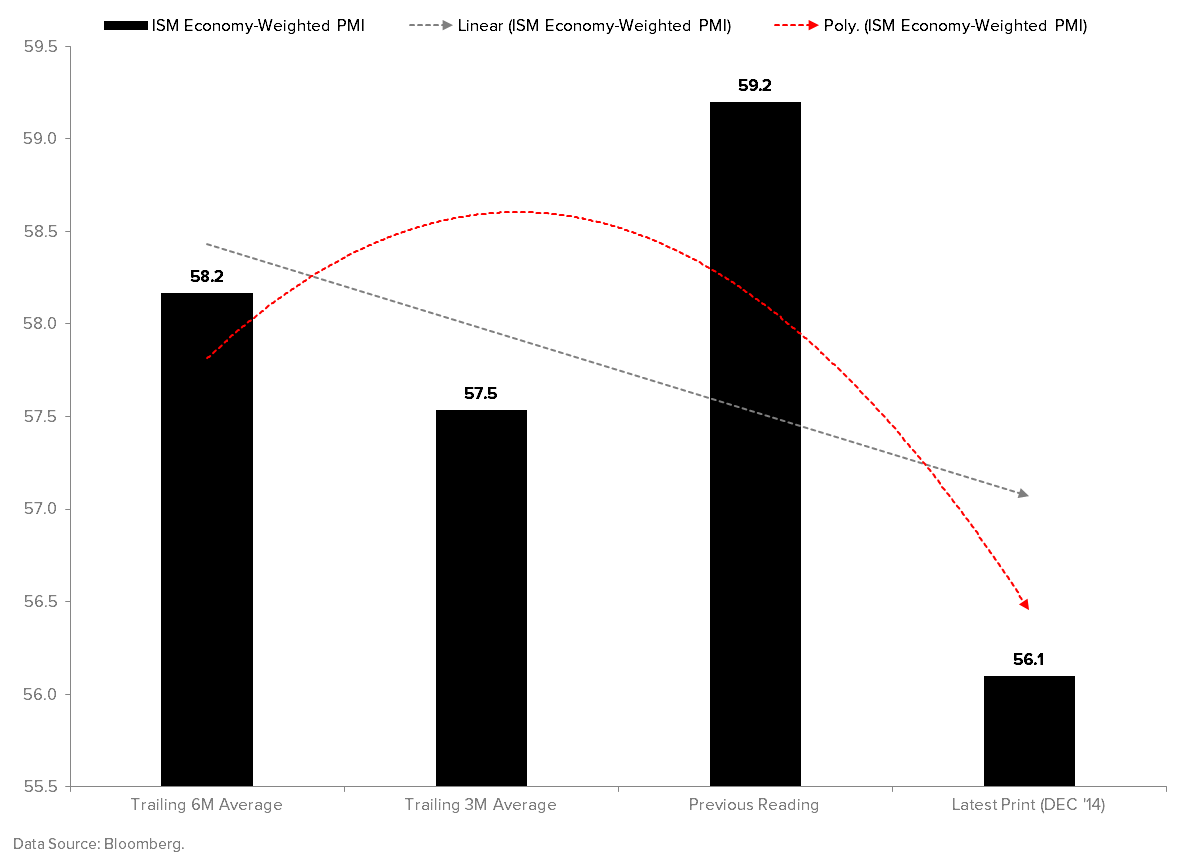

If the DEC Markit and ISM Composite PMI data are any indication, the preponderance of DEC high-frequency growth data will continue to slow as we progress throughout the month of January:

If the DEC Average Hourly Earnings data from Friday’s Jobs Report is any indication, the trend of reported disinflation will continue when we get the DEC CPI data next Friday:

When the 2nd derivatives of real GDP and headline CPI are concurrently negative, the marginal investor is predisposed to allocate assets to the long bond and to equities with defensive, bond-like characteristics.

Fortuitously for you, you’re already positioned that way!

RH

Here’s a look at the growth algorithm for Restoration Hardware going forward.

1) Square Footage Growth: The company is in the beginning stages of transforming its existing 10,000 square foot Legacy Store portfolio to the 45,000+ square foot Design Gallery concepts. Currently the company has 7 of these properties in LA, Houston, Scottsdale, Indianapolis, Boston, Atlanta, and Greenwich. Over the next 5 years an incremental 20+ locations will be added and square footage will grow from 550K at the end of FY2013 to 1550K at the end on 2018.

2) Revenue: Our model calls for mid-20’s sales growth over the next 4 years as the company finally has the real estate to showcase its diversified category portfolio. The current Legacy stores show about 10%, but the new Full Line Design Galleries (Atlanta) houses closer to 70%. The proof of concept from the existing 7 design gallery doors have shown that new categories when presented at retail experience a 50%-150% lift across channels (both retail and DTC). That’s a big opportunity for RH as it builds out its real estate portfolio.

3) Margins: Over the duration of our model we have operating margins going from high single digits to mid-teens. The main driver of that is occupancy leverage. As the company builds these new bigger stores it is taking square footage up in each market by 6x to 8x, but rent expense only increases by 30%-50%. Meaning that on average new square footage comes in at about 25% of the cost of Legacy Store square footage. Perhaps the best example of that is the Denver market where selling square footage will go from 7,500 sq. ft. to 45,500, with rent expense going from $1.3mm to $2.0mm. And this deal isn’t a one off. Over time occupancy will come down from low double digits to mid-single digits. That will be a big tailwind to margins.

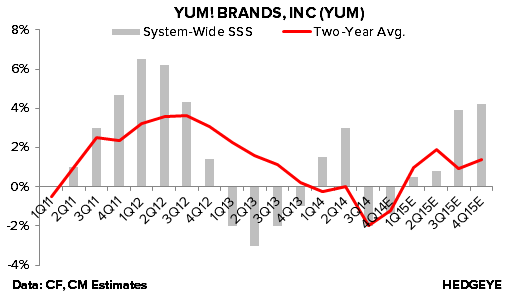

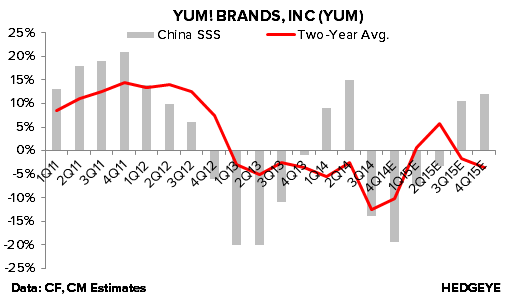

YUM

YUM is a stock that continues to trade at a significant discount to its intrinsic value, making it one of our favorite long-term buys in the restaurant space. The China recovery may be slightly slower than anticipated as management works hard to regain consumer trust there, but the recent industry-wide acceleration in U.S. sales should be enough to offset any concerns. If the recovery fails to materialize at all, management will be pressured to de-risk the business by spinning off a piece of China.

We wouldn’t be surprised to wake up one day to news of a prominent activist buying up shares of YUM. There’s too much value here to ignore and the stock’s multi-year underperformance is not going unnoticed. Sell-side sentiment is bombed out enough to provoke several upgrades on the slightest hint of good news, and the buy-side knows better than to short a company with such upside. Learn to ignore the day-to-day volatility and prepare yourselves to own this stock for the long haul.

HOLX

3D TRACKER UPDATE DECEMBER 21, 2014

Our Healthcare team updated our count (proprietary process) of US facilities currently offering 3D Tomosynthesis. December placements are signalling a break-outquarter after a sharp acceleration in October and slight correction to a still very high rate in November. We believe we are seeing a sustained acceleration in placements that will likely drive upside to Breast Health throughout FY2015.

PLACEMENT HISTORY TABLE

The number of new facilities is accelerating and coming up against an easy comparison (December 2013). The key data in the table below is the 146 new facilities during F1Q15 versus 49 a year ago, or a ~+300% increase. Consensus is modelling 4.7% growth for Breast Health in F1Q15 while our model is producing segment growth well into the teens.

PAP Testing Volume

Results of our December OB/GYN show rate of decline in PAP volume continues to moderate. 48% of survey respondents indicate pap testing on a 3-year basis, with an annual expected rate of decline of -12% to reach 100% compliance. This rate of decline translates into 2.6 years before total compliance is reached.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

JUST CHARTS: EYE-CATCHING INDUSTRIALS DATA

A rig today isn’t quite the same as a rig in the late 1970s, but the trend should be clear.

ICI FUND FLOW SURVEY: 2014 WAS THE YEAR FOR FOREIGN STOCKS AND DOMESTIC EQUITY ETFS

2014 was best for international stock funds and domestic equity ETFs. Money funds also rallied late with +$124 billion in the last 11 weeks