EVENTS TO WATCH

Today (1/8)

FDO - Earnings Call: 10:00am

BBBY - Earnings Call: 5:00pm

COMPANY HIGHLIGHTS

DKS - Dick’s Sporting Goods explores going private

(http://www.reuters.com/article/2015/01/07/us-dicks-m-a-idUSKBN0KG1S820150107)

Here's yet another example of a company that leaks out a one-liner talking about going private, and all of a sudden public markets get more excited about it. These are early stage discussions, which in no way, shape or form means that DKS actually will, in fact, go private.

Based on our LBO model (ping us is you want a copy), a DKS LBO at the current price -- and even 20% lower -- makes no financial sense. The IRR is negative in both instances.

To be clear, our model assumes…

- DKS tops out at 900 stores by 2018, below management's 1,100 goal

- 2% comp store sales growth as e-commerce offsets negative store traffic.

- Gross Margins fall by 50bp annually as e-commerce dilutes profitability, and aggregate sales growth is not strong enough for DKS to leverage occupancy costs.

- EBIT margins fall from 8% today to 5% in 2018.

The problem, however, is that DKS hired a banker that will use the inverse of our model as it shops the company around. Any PE investor worth its salt will see through bulled-up banker assumptions in a heartbeat. But if there's just one that's gullible enough think that DKS can grow its store base to 1,100 while improving margins at a low-mid single digit comp, then DKS might very well have a suitor. If I was Ed Stack (with 61% of the voting stock) I'd be speed-dating to find that partner.

LULU - lululemon athletica names stuart c. haselden chief financial officer

(http://investor.lululemon.com/releasedetail.cfm?ReleaseID=890190)

Takeaway: New CFO Stuart Haselden may not be a splashy hire, but we're inclined to give the duo of Michael Casey (ex. Starbucks CFO) and David Mussafer (Advent/new to the Board) the benefit of the doubt in the hiring process. This is the first big move for the Board after the coup that led to Chip's replacement as Chairman and the selling of half of his ownership position. We almost never get too upbeat about a single individual in an organization. But we think that this role is an exception.

Why? The Finance function at LULU has always been extremely weak. Currie (ex. CFO) was appropriate to be Chip's numbers guy in the early days of the company, but CHIP purposely kept the entire function at bay as the company grew up as he thought it would hurt the culture of the company. Translation = one of LULU's biggest problems is that it grew up without having any finance culture whatsoever. It's impressive that it made it this far.

Now you have Haselden who was hired by the Board led by Casey and Mussafer who both know the caliber of person needed to get this company back on track. Our sense is that new CFO will be tasked with rightsizing the company. If Laurent wants to follow, then great. Everyone wins. But if he resists, then the new CEO will soon be the old CEO.

It's odd…in our conversations with investors, people agree that Currie had to go, but don't necessarily think that there's a problem with the finance organization being so weak at LULU. We think that people will only realize how problematic this has been once it is fixed.

PVH - PVH Corp. Announces Closing of Izod Retail Division

(https://www.pvh.com/investor_relations_press_release_article.aspx?reqid=2004750)

Takeaway: The KSS bulls will argue that this is a net positive for the company who just picked up distribution in the fall of 2014. We'd point to a couple of things. 1) Most, if not all of the locations set to close are outlets. If you're an outlet shopper you don't go to the mall to buy IZOD, you go to the outlet center specifically to find great value in whatever brands happen to be there. Men's Polo shirts are a dime a dozen and so are the places that sell them. 2) IZOD - is not a KSS exclusive. If you go to Izod's website, which we would note doesn't actually sell anything, you'll see its wholesale partners: Kohl's, Macy's, Amazon, JCPenney, Belk, Bonton, Beall's, and Hudson's Bay. All of whom have a longer standing relationship and association with the brand than KSS. 3) Lastly and probably most importantly, PVH isn't closing these stores because consumers really want the brand. The IZ logo doesn't resonate the way the alligator once did and the brand has been diluted down to the point that it's a commodity. In that context, the closing of DTC makes sense as the brand itself can't drive traffic.

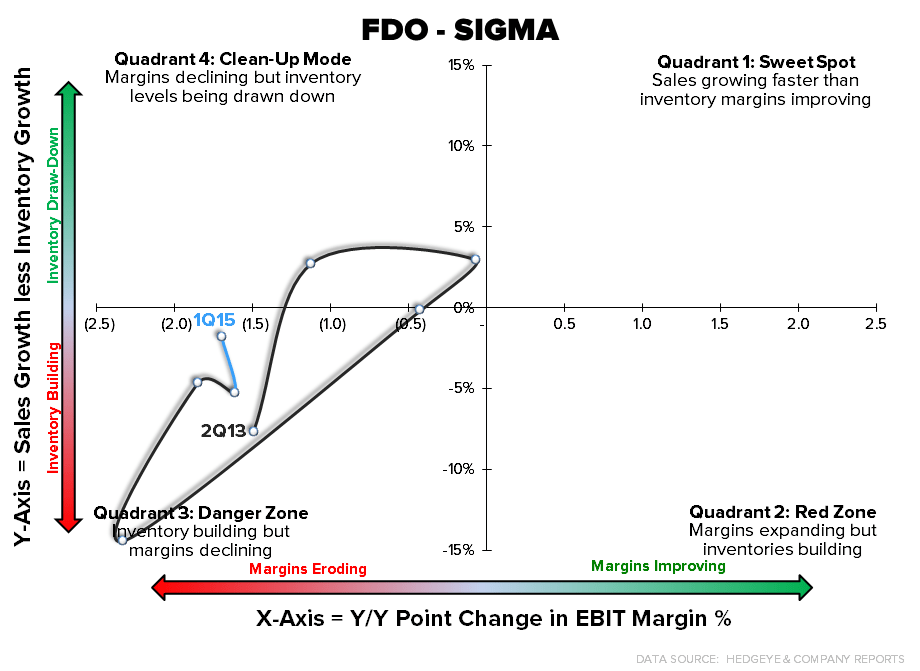

FDO - 1Q15 Earnings

AMZN, EBAY - AMZN 2year trend improvement, EBAY negative data point on 1 and 2 year basis

Takeaway: ChannelAdvisor's total same store sales for the Holiday (November and December) came in at +16.2%. AMZN outperformed at +26.9% and EBAY underperformed at +7.3%. The trend for both companies’ fiscal Q4 wasn't as good as the prior 2 quarters.

OTHER NEWS

TGT - Target Links With Lilly Pulitzer

TSCDY - Tesco’s Lewis Sets Out Revival Plan With Closures, Disposals

TSCDY - Tesco Names Halfords’s Davies as U.K. CEO in Turnaround Bid

MAKSF -Marks & Spencer Clothing Sales Drop Amid Online Delays

FAST - Fast Retailing Q1 Net Profit Jumps 64%

WTSL - Bankruptcy Rumblings Surround Wet Seal Closures

(http://www.wwd.com/retail-news/financial/wet-seal-shutters-338-stores-8091507?module=Business-latest)

BODY - Body Central Said to Prepare for Bankruptcy Within a Week

Bi-Lo CEO to leave