In reviewing the domestic December PMI data (see: (HEDG)EYE-CANDY | SURVEY SAYS...) we noted that the underlying Macro reality probably stood somewhere between the ongoing slowdown reflected in the Markit PMI measure (which slowed for a 6th consecutive month in Dec) and ongoing peak strength reported in the ISM survey.

We posited that alongside a reversal in here-to favorable seasonals and a deceleration in global growth and export demand, the reported ISM/IP data would follow the Markit reading lower in the coming months. With both the ISM mfg and services surveys slowing in December, it looks like that trend is playing out.

The U.S.’ s world share of trade and GDP may be in retreat but its glacial transition towards global interconnectedness is not. Is anyone particularly surprised that export orders (export orders don’t directly feed into the ISM index calculation but they obviously impact total activity) have slowed or domestically based global conglomerates remain hesitant to materially accelerate capex into OUS disinflation and discrete growth deceleration?

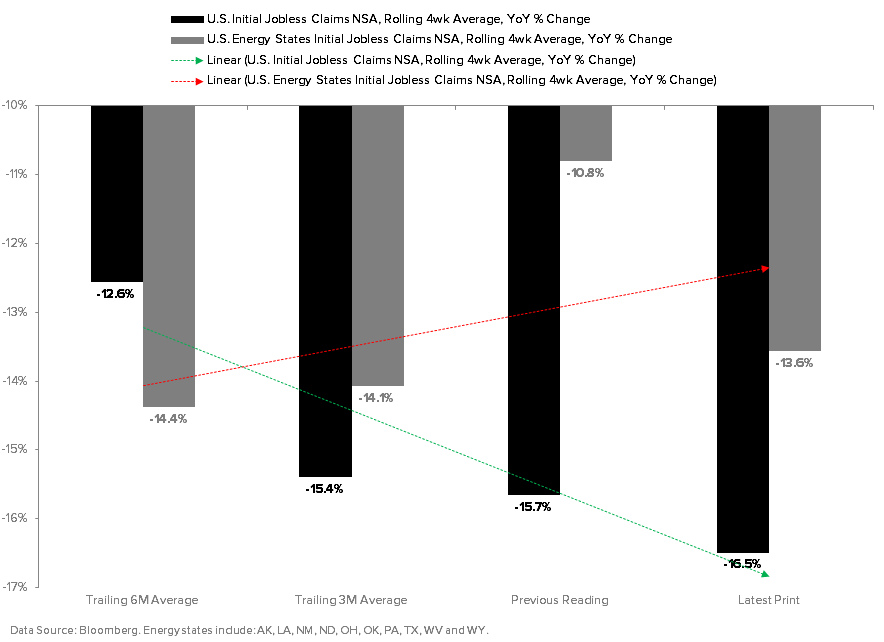

The ISM employment sub-indices remain good on balance and the domestic labor market remains insulated from the broader global reality, for now. Historical cycle precedents suggest labor market strength/improvement still has some runway before inflecting negatively.

The acute collapse in energy prices and any associated (negative) flow thru to capital spending and net hiring introduces some significant uncertainty, but represents a risk that can be largely monitored and managed in real-time with the high frequency labor data.

Bond yields and capital flows, meanwhile, continue to confirm the economic gravity of a global entre into Quad #4.

We wouldn’t be incremental buyers of the long-end on weakness but TLT/EDV remains one of our favorite global macro positions. Consensus disagrees (see net spec positioning), but #MacroMisfit has repeatedly proven to be profitable profile.

Christian B. Drake

@HedgeyeUSA