Below are Hedgeye analysts’ latest updates on our seven current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

Please note we added Hologic (HOLX) on Friday.

We feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

Sticking With the Long Bond to Start 2015

Consistent with our intermediate-term view on the most probable trajectory of both rates and the reported inflation – i.e. lower – we remain bullish on the long bond (in TLT, EDV and MUB terms), as well as on equities with bond-like characteristics (in XLP, XLV and VNQ terms).

As most recently reiterated by today’s Markit and ISM Manufacturing PMI data, domestic economic growth slowed on the margin in 4Q14 and we will continue to receive such #GrowthSlowing data points throughout the month of January:

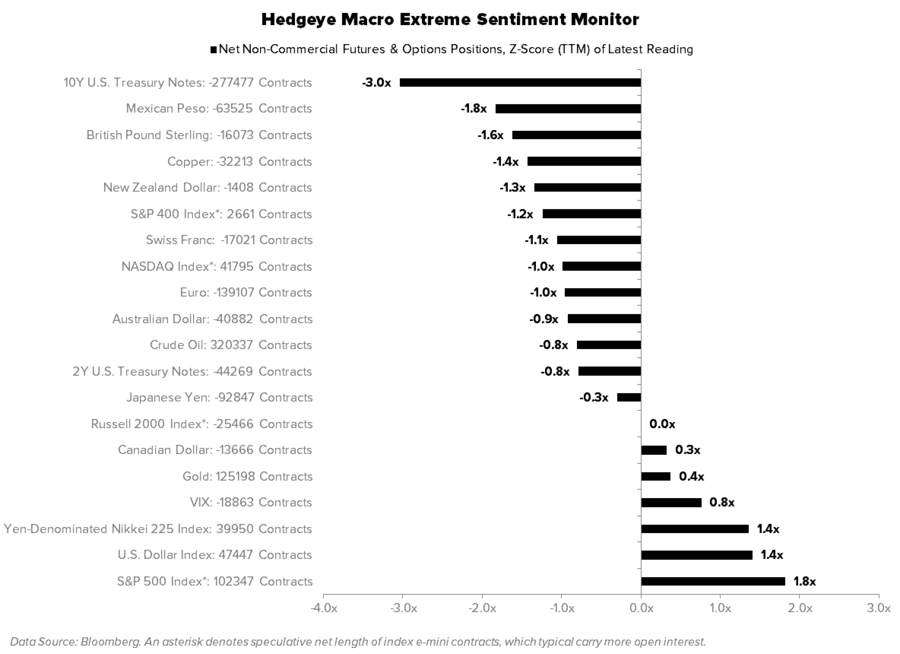

Additionally, there remains a 3-SIGMA net SHORT position in 10Y Treasury futures and options contracts; to the extent long-term Treasuries continue to rally, we think there is ample room for mass capitulation in the coming weeks on long-term.

In summary, we continue to see ample risk of Consensus Macro having to cover [higher] securities that you already own.

RH

Shares of Restoration Hardware closed 2014 up 43% and we think this name still has legs in the New Year.

We are modeling $2.40 in EPS for the 2014 fiscal year with a 45% EPS CAGR through 2018. At a mid-twenty multiple, that gets us to an RH stock price well over $250 by 2018.

It remains our favorite name in retail.

yum

We’ve previously mentioned that we believe YUM is vulnerable to activism, but in this week’s addition we seek to provide more detail on why now is an optimal time for change. YUM currently has both internal and external factors working for it. We believe the company is a change, or two, away from unlocking significant shareholder value.

Internal Changes are a Catalyst for Change

- New CEO beginning in 2015

- We believe the current CFO is likely more open to changes than the previous CFO

- In 1Q15, YUM changed its reporting structure to align global operations outside of China and India by brand

- This change in reporting structure allows for a clean sale or spinoff of brands

- The new reporting structure also suggests little internal friction to a potential spinoff or sale of brands

- YUM has been paying down debt and is now underleveraged relative to peers

External Environment Creates Possibilities

- Restaurant multiples are at all-time highs

- Restaurant IPOs are being very well-received by investors

- Global asset-light business models are trading at a premium to the group

- Significant liquidity in the fixed income markets

- Significant liquidity in the franchisee finance market

- It is a great time to be a seller of restaurant assets, especially of strong brands like YUM’s

- The board needs to address the issue of increased volatility in the Chinese business

- Gaming companies have successfully issued tracking on their Chinese assets

- YUM China could be the largest consumer company in China and investor interest would be strong

Regardless of any major changes, upside to YUM shares in 2015 could also be driven by a recovery in China. The street is modeling a turnaround that is, in our view, rather tempered compared to expectations of past recoveries. If China recovers, the stock will take off. If not, we expect an internal or external force to effect change.

There are multiple ways to win here, which is why we continue to like YUM heading into 2015.

holx

We added Hologic on Friday. Here is the note which accompanied the addition.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

ici fund flows: heavy inflow to passive funds

Investors have favored passive over active this year. Passive equity put up its largest inflow in the 52-week period.

podcast: morning macro call (Friday 1/2)

Hedgeye CEO Keith McCullough walks through the most important macro data on his radar screen and answers key questions from institutional subscribers.