SENTIMENT UPDATE

OCTOBER 6, 2009

TODAY’S CALL OUT

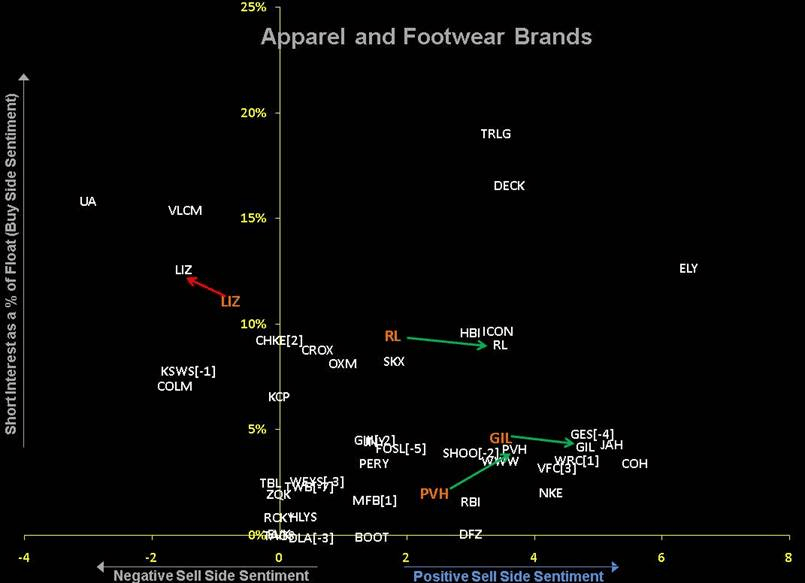

A couple of months ago we introduced an analysis breaking down over a hundred retail-related companies by triangulating buy-side sentiment, a sell-side ratings factor, and the delta between insider buying/selling. The visuals clearly flag areas of both risk and opportunity. With very positive “anecdotal” sentiment heading into September sales, we’ve decided to revisit our quantitative sentiment screen to see how things have changed over the past 5 weeks.

Callouts and notable changes since the end of August through yesterday include:

- Notable Negatives: LIZ, CAB, HIBB, and FL

- Notable Positives: RL, GIL, PVH, DSW, GCO

- Positive Sentiment, Low Short-Interest, but High Insider Selling: TGT, SPLS, GES, KR, GPS, LOW

- Notable Insider Activity (Negative indicates selling): GCO [-8], TGT [-6], SPLS [-6], SKS [-6], FOSL [-5], GES [-4], DKS [-3], KR [-2], GPS [-2], VFC [3], DLTR [5]

- Interestingly, overall short interest for the this universe was essentially unchanged only up 10bps to 7.8% this month.

LEVINE’S LOW DOWN

Some Notable Call Outs

- With NFL TV ratings off to a very a strong start, there is even more reason to keep an eye on an upcoming Supreme Court case that pits a sportswear manufacturer against the league. The root of the case asks the question of whether the National Football League should be considered a single entity or a collection of 32 businesses. If the court rules that the NFL remains a single entity, the league would be mostly exempt from antitrust laws. This in turn would allow the NFL to continue negotiating exclusive apparel licenses on a league-wide basis as well controlling other key topics like ticket prices and player salaries.

- Add supermarkets to the growing list of consolidation and m&a. The parent company of Food Lion, Delhaize, has signed a letter of intent to acquire Bi-Lo ‘s assets for $425 million out of bankruptcy. The transaction is subject to court approval and is just one of a handful of proposals currently on the table for bankrupt chain.

- In what is likely just the beginning of a massive opportunity to harvest data and ultimately monetize it, Facebook has launched an application called the “Gross National Happiness Index”. The index is developed from data that is collected from public and semi-public forums, with a particular goal of identifying terms that are most often used to express happiness and sadness. So far the results are simply plotted on a graph which then depicts such trends over time. However, we suspect it’s only a matter of time before key word searches and algorithms are used to target consumers and promote brands based on user generated “conversations”.

- Almost 1yr to the day Sears and Kmart brought back the Layaway Plan, they introduce online layaway… what’s next, the giveaway plan?

MORNING NEWS

-Group Pressures European Retailers to Lift Wages - An Amsterdam-based advocacy group has said it will target Europe’s biggest retailers, including Tesco, Carrefour, Aldi and Lidl, this week as part of an international effort to raise the wages of garment workers in India and the Far East. The Clean Clothes Campaign said Monday that its partner organizations across Europe planned to call for “an immediate commitment by retailers to take steps to implement the living wage in their garment production supply chains.” CCC’s efforts are meant to raise awareness for the Asia Floor Wage Alliance, a worldwide consortium of trade unions and labor rights activists, which on Wednesday in New Delhi will launch an international campaign calling for a common minimum living wage for Asian and Far Eastern garment industry workers. <wwd.com>

-NRF Sees Holiday Retail Sales Sliding - Holiday retail sales will be down, but not as sharply as last year, according to the National Retail Federation. The trade organization on Monday predicted holiday sales would decline 1% this year to $437.6 billion. That’s well below the 10-year average of 3.39% gains, although far better than both last year’s 3.4% drop and the 3% decline in annual retail sales forecast for all of 2009. “As the global economy continues to recover from the worst economic crisis most retailers have ever seen, Americans will focus primarily on practical gifts and shop on a budget this holiday season,” NRF chief economist Rosalind Wells said. <wwd.com>

-Chinese Footwear Sales to Witness Over 7% CAGR - A new report “China Footwear Market Analysis” published by RNCOS provides extensive research and rational analysis on the Chinese footwear industry, giving an insight into the industry’s production as well as consumption trends. The report suggests that rising income levels and increasing number of fashion-conscious people will lead Chinese footwear market to post a CAGR of over 7% (in volume terms) from 2010 to 2013. As per the report, the footwear industry in China has witnessed robust growth over the recent years, both in terms of consumption as well as production. Our industry analysis identifies that footwear consumption in the country has been growing at an annual rate of around 6-7% since past few years. A number of factors such as increasing income levels and rising fashion-consciousness and brand awareness among Chinese populace, in addition to other consumer trends, are continuously boosting the footwear consumption. We anticipate the Chinese footwear market to swell at a CAGR of over 7% in volume terms for the period spanning from 2010 to 2013. <emailwire.com>

-ENI-JR286 Becomes Global Licensee for Nike Fitness Product - ENI-JR286, Inc., based in Redondo Beach, CA, has entered into a new exclusive long term relationship with NIKE, Inc. As per the agreement, ENI-JR286, Inc. will become the global licensee for certain Nike’s fitness and sports equipment accessories. "This relationship allows our organization the ability to partner with the world’s largest and most innovative athletic brand and enable them to fully penetrate the global market with these accessories, thus providing the consumer a true head-to-toe offering," said Jonathan Hirshberg, President of ENI-JR 286, Inc.. <sportsonesource.com>

-FTC to Regulate Blogging, Testimonials, and Celebrity Endorsements - The Federal Trade Commission approved final revisions to the guidance it gives to advertisers on how to keep their endorsement and testimonial ads in line with the FTC Act. Under the revised Guides, advertisements that feature a consumer and convey his or her experience with a product or service as typical when that is not the case will be required to clearly disclose the results that consumers can generally expect. The revised Guides also add new examples to illustrate the long standing principle that “material connections” (sometimes payments or free products) between advertisers and endorsers – connections that consumers would not expect – must be disclosed. <sportsonesource.com>

-CIT Launches Restructuring Plan - CIT Group, the troubled lender to small to medium-sized businesses, launched a restructuring plan aimed at reducing $5.7 billion in debt. The company warned it could file for bankruptcy if it falls short of that goal. Under the plan, bondholders will be given the right to exchange their current notes for a portion of a series of newly-issued secured notes and/or preferred shares. <sportsonesource.com>

-Macy’s Gets Ellen Tracy Sportswear Exclusive - Macy’s Inc. confirmed Monday that it has forged a strategic alliance with Ellen Tracy owner Brand Matter LLC and its sportswear licensee, RVC Enterprises, to become the exclusive department store retailer of Ellen Tracy better women’s sportswear, beginning in spring 2010. <wwd.com>

-USTR Announces Small Business Initiative - U.S. Trade Representative Ron Kirk unveiled a new agency initiative on Monday to help small and medium-sized businesses in the U.S. The goal of the program is to assist companies in boosting their exports and grow jobs in the U.S., Kirk said. <wwd.com>

-Big and Little Retailers Join Forces to Stimulate Sales - Over the weekend, Gap and edgy Parisian boutique Merci wrapped up a month long project in which each hosted a selection of the other’s products in their New York and Paris stores. Also over the weekend, Parisian department store Printemps christened the opening of a Maria Luisa location within its recently revamped Boulevard Haussmann flagship here. Uniqlo recently set up shop in hip Paris concept store Colette as a teaser for the arrival of its Paris flagship, which opened last week. And Target is mulling a one-off collaboration with Britain’s Liberty to launch clothing and accessories bearing the store’s trademark flower prints. <wwd.com>

-Tesco Reports Smallest Profit Increase in 11 Years - Tesco Plc, the world’s third-largest retailer, reported the weakest first-half profit growth in 11 years after acquisitions added to financing costs and units from the Czech Republic to Ireland withered in the recession. Net income rose 1.3 percent to 1.03 billion pounds ($1.64 billion) in the six months ended Aug. 29, from 1.01 billion pounds a year earlier, the Cheshunt, England-based company said today. The median estimate of eight analysts surveyed by Bloomberg was 1.04 billion pounds. So-called trading profit increased 14 percent to 1.55 billion pounds, the retailer said. <bloomberg.com>

-Tesco Launches Separate Online Fashion Store - Tesco has launched its first standalone online fashion store at www.tesco.com/clothing, with some 3,500 product lines and 20 brands across kidswear, menswear, accessories and womenswear, including character lines. The retailer hopes the business will grow to account for 10 percent of its total clothing sales. The site features Tesco clothing brands such as F&F and Cherokee, as well as casualwear brand Henry J Finn, urban menswear brand Method, handbags by Mischa Barton, womenswear by Chupa Chups and fair-trade denim by Monkee Genes. <licensemag.com>

RESEARCH EDGE PORTFOLIO: (Comments by Keith McCullough): KR

10/05/2009 10:18 AM

SHORTING KR $21.01

Credit Suisse adds it to their "focus list"... We agree. Investors should be focused on selling the stock as the risk management setup changes. KM