“My prediction? Pain!”

-Mr. T

For those who are in the business of being paid to issue wire-to-wire-JAN-to-DEC annual predictions, that is…

I can also predict, with 100% certainty, that market and economic risks (often two very different things) will accelerate and decelerate throughout the year, in rate of change terms. So let’s embrace the dynamic and non-linear uncertainty of that.

On behalf of everyone on my team, I wanted to wish you, your families, and firms the best of luck and health in 2015. Working together, I know we can make this year every bit as successful as 2014 was.

Back to the Global Macro Grind…

What defines a successful year in terms of professional growth is often different vs. the YTD performance that stares us in the face each and every day. Since I think of most things in rate of change terms, progression vs. regression is as important to me as anything.

Are we learning from our mistakes or are we making excuses? Are we challenging ourselves to evolve our processes or are we being complacent? Are we enjoying the path of progression or are we just trying to get paid?

For me personally last year was quite satisfying. It was the 1st year in my career that I was able to translate a bearish view on big Global Macro factors (rate of y/y change in growth and inflation) into an uber bullish position on the long side (the Long Bond).

To review the score:

- Depending on what version of the Long Bond Index you had on, you were +24-41% in 2014

- The SP500, Dow, and Russell 2000 were +11.4%, +7.5%, and +3.3% in 2014, respectively

- Commodities (CRB Index) were -18.4% YTD

Now if your job is to simply navel gaze at one of those US equity centric indexes (you can’t charge active manager fees for that), you’d probably say 2014 was a good year. And I don’t disagree with that. But being long the Long Bond was a great year.

How do you define “great” returns?

- Higher absolute returns?

- Higher relative returns?

- Lower-volatility adjusted returns?

Well, being long the long end of sovereign bond markets from Germany to France to the USA and back again beat their local equity market returns on all 3 of those factors.

That last point on volatility is the most important. It’s also the one that tends to tackle most momentum oriented fund managers, eventually. There is nothing that crushes levered-long beta faster than a breakout in the volatility of an asset class’ price.

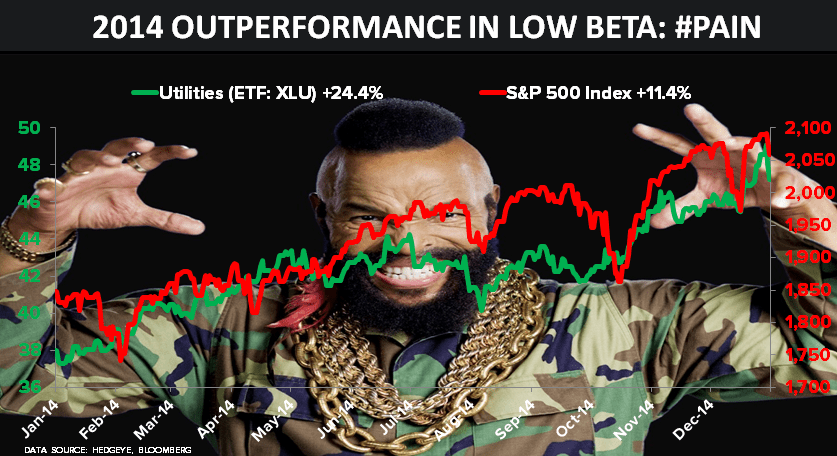

If you’re a US equity only investor, the lower-volatility + higher-absolute-and-relative returns came in mostly slow-growth, lower-beta, #YieldChasing sectors:

- Number 1 (within the Top 9 S&P Sectors) for 2014 was Utilities (XLU) at +24.3% YTD

- Number 2 for 2014 was Healthcare (XLV) at +23.3% YTD

Yep, instead of being long #deflation (Energy stocks, XLE, DOWN -10.6% YTD), these slower-growth, lower-volatility sectors had similar returns to what? Yep – the Long Bond.

Tech (XLK) had a good year at +15.7%. But most of the outperformance in Tech came from the low-beta big cap names like AAPL and MSFT (+40% and +30%, respectively) where stock specific volatility got smashed inasmuch as small-cap social #bubble stocks did.

Then, of course, there was the rest of the world (no, it didn’t cease to exist) in Global Equities where you could have lost everything you made in your Russell or Dow allocations if your RIA’s pie chart had you “diversified” into:

- Russian stocks -42.6% for 2014

- Greek and Portuguese stocks -25-26% on the year

- South Korea’s KOSPI (heaviest weight in the EEM index) -3.7% in 2014

- Brazil’s Bovespa -2.6% YTD

- FTSE (UK index) down -2.1% for the year as well

And no, I won’t go into all of the #GrowthSlowing and #Deflation realities that train wrecked COMMODITIES as an asset class in 2014. I’m trying to be progressive this morning! “So” I’ll keep our net asset allocation to commodities right where it’s been, at 0%.

As far as my 2015 predictions go – I don’t have any. Or at least not on the JAN-DEC terms that the #OldWall and its media drives advertising revs. That said, I’ll tell you what wouldn’t surprise me in the next 6-10 months (because it’s already happening):

- Global #Deflation Risk becomes consensus, as central planning Policies to Inflate fail

- Interconnected risks, across asset classes, linked into global #GrowthSlowing + #Deflation continue to rise

- Late-cycle US growth indicators (like employment) slow, in rate of change terms

- Early cycle US growth indicators (like Housing and Restaurant traffic) accelerate, in rate of change terms

- I lose 5-10 pounds, because I need to

Yes, I predict pain (for myself) in cutting out my post Mite Hockey practice Mickey D’s meals on Tuesday nights too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.13-2.25%

SPX 2017-2090

FTSE 6

VIX 16.03-19.95

EUR/USD 1.20-1.22

Oil (WTI) 52.61-55.38

Gold 1167-1195

Best of luck out there this year,

KM

Keith R. McCullough

Chief Executive Officer