“Inconsistent ... just when things seem to be settling a bit, a new set of pressures develops."

ISM Survey - Retail Trade

Yesterday the S&P 500 rallied 1.5% on the back of the ISM survey. The improvement in the ISM numbers, though impressive, was very narrow with just 5 industries reporting growth in September and 13 industries reporting contraction.

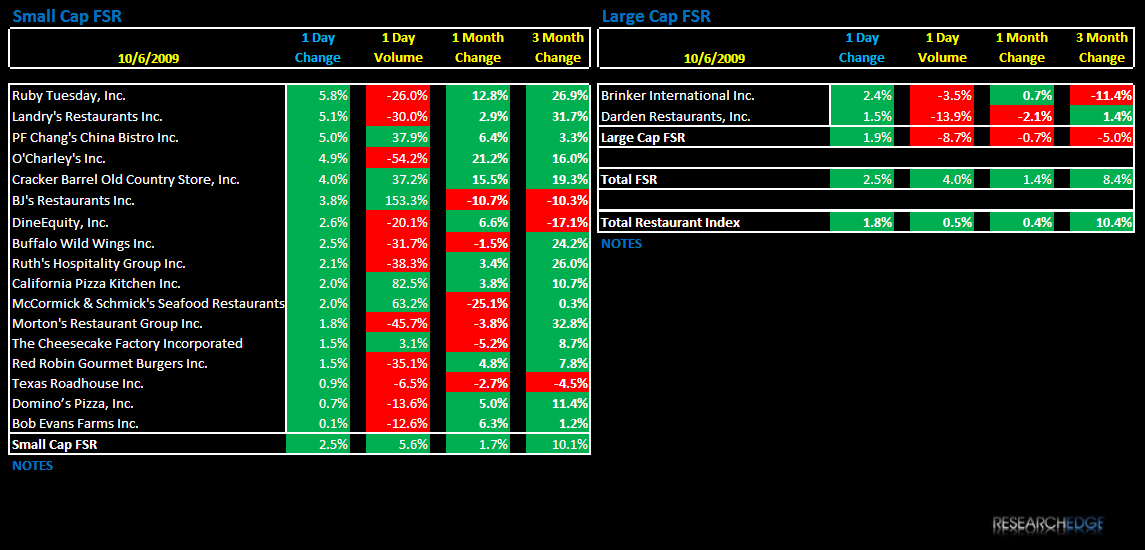

The quote above is from one of those industries not reporting growth. That is exactly what we are hearing from restaurant operators we are talking to. There is no consistency to sales trends. Tonight YUM will likely confirm the same findings. I know the financial press had a favorable article about YUM yesterday, but the stock was up 5.1% on a 126% increase in volume. YUM’s IR team is the best in the business so they are not whispering in anybody’s ear, but it sure seems like somebody knows something. We will see how today pans out for the stock.

RT reports on Wednesday and that stock was up 5.8% yesterday, but volume was down 26% - not a big RED flag there. Due to RT’s real estate portfolio is a cheap stock, but it is trading at 8x NTM EV/EBITDA versus 6.6x the group average. Sales trends really need to improve for the stock to work from here, which seems unlikely. I’ll pass on that trade for now.