Key Takeaways:

Our heatmap below shows almost everything red across the intermediate duration. 10 of 12 signals are deteriorating while just 1 is improving. The main callouts this week are: 1) commodity prices continue to drop. The CRB Index was down 2.2% week-over-week and is now down 12.0% month-over-month as Saudi Arabia keeps its foot on the production gas, 2) Chinese steel prices and the Chinese interbank rate are both going the wrong way. Chinese steel prices are down 2.7% on the week and are down 6.7% on the month. Meanwhile, Chinese interbank rates are up 97 bps on the month, and 3) Europe is backsliding with Greece moving, once again, to the front burner with the announcement this morning that the parliamentary vote for a new president has failed, triggering snap elections in early 2015.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 12 improved / 3 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Negative / 1 of 12 improved / 10 out of 12 worsened / 1 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 3 out of 12 worsened / 7 of 12 unchanged

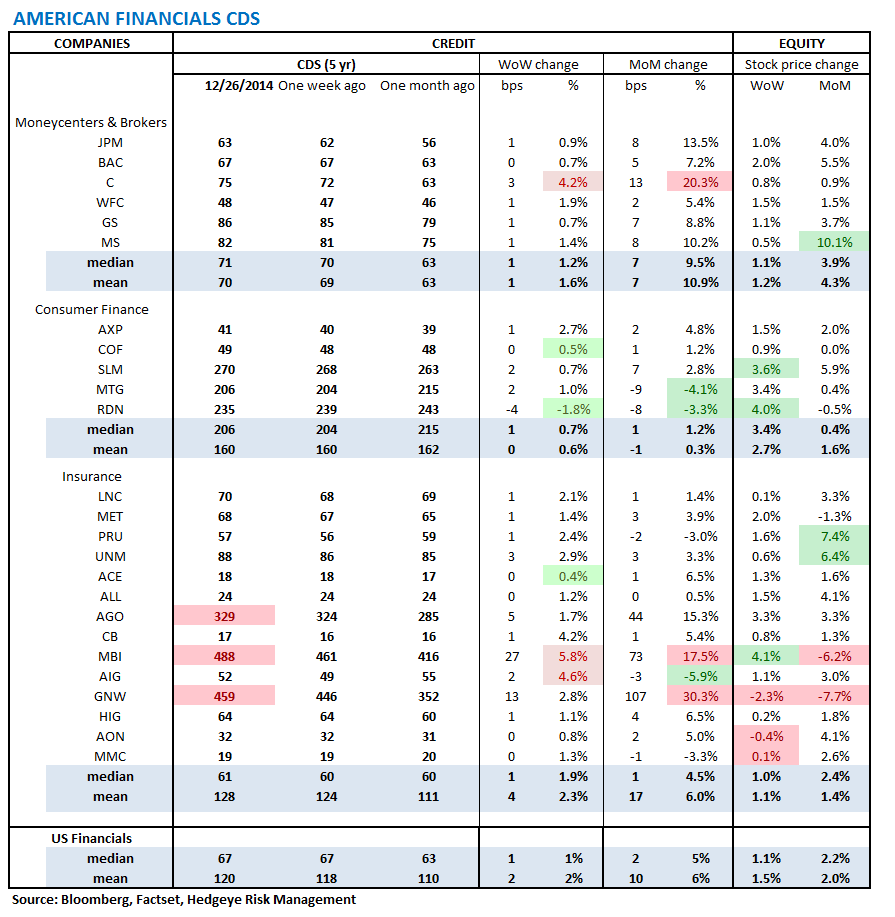

1. U.S. Financial CDS - Swaps widened for 24 out of 27 domestic financial institutions. MBIA swaps showed the biggest increase for the second week in a row (+27 bps to 488 bps). Meanwhile, Genworth swaps continue to widen, a trend sparked by their November 7 announcement of an impending charge of over $1 billion dollars pre-tax and continued by their December 17 announcement that they had not yet completed their annual review of long-term care insurance active life margins. Genworth swaps rose 13 bps to 459 bps.

Widened the least/ tightened the most WoW: RDN, TRV, TRV

Widened the most WoW: MBI, AIG, C

Tightened the most WoW: AIG, MTG, RDN

Widened the most MoM: GNW, C, MBI

2. European Financial CDS - Swaps mostly widened in Europe last week. Greek banks widened the most on fears that the parliamentary vote for a new president would fail. News broke this morning that the vote did in fact fail. That will force the country into snap elections in early 2015.

3. Asian Financial CDS - 9 out of 10 Asian bank CDS widened last week. Japanese and Indian bank swaps widened the most.

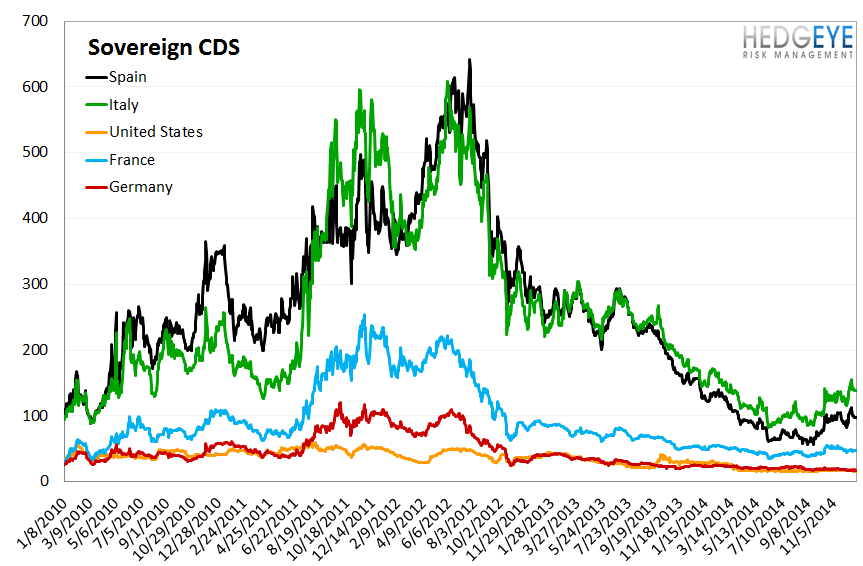

4. Sovereign CDS – We look at the move in swaps as of Friday's close so the Greek election news this morning is not reflected in these figures and has most swaps higher as of this morning. There was notable tightening in Portuguese sovereign swaps (-23 bps to 173 bps) and modest tightening in Italy and Spain.

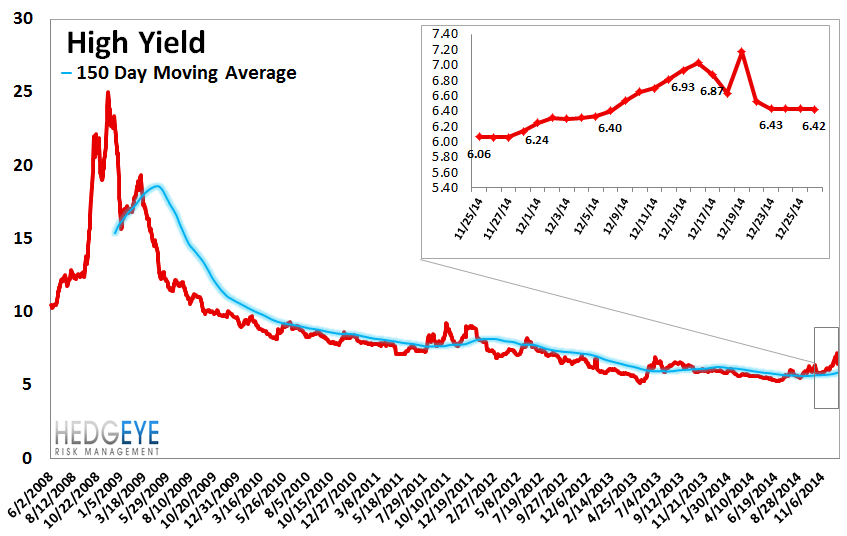

5. High Yield (YTM) Monitor – High Yield rates fell 74.8 bps last week, ending the week at 6.42% versus 7.17% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 5.0 points last week, ending at 1853.

7. TED Spread Monitor – The TED spread rose 3.2 basis points last week, ending the week at 25.4 bps this week versus last week’s print of 22.21 bps.

8. CRB Commodity Price Index – The CRB index fell -2.2%, ending the week at 235 versus 240 the prior week. As compared with the prior month, commodity prices have decreased -12.0% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 10 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 6 basis points last week, ending the week at 3.549% versus last week’s print of 3.606%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 2.7% last week, or 76 yuan/ton, to 2756 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

12. 2-10 Spread – Last week the 2-10 spread tightened to 151 bps, -1 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.9% upside to TRADE resistance and 2.2% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT