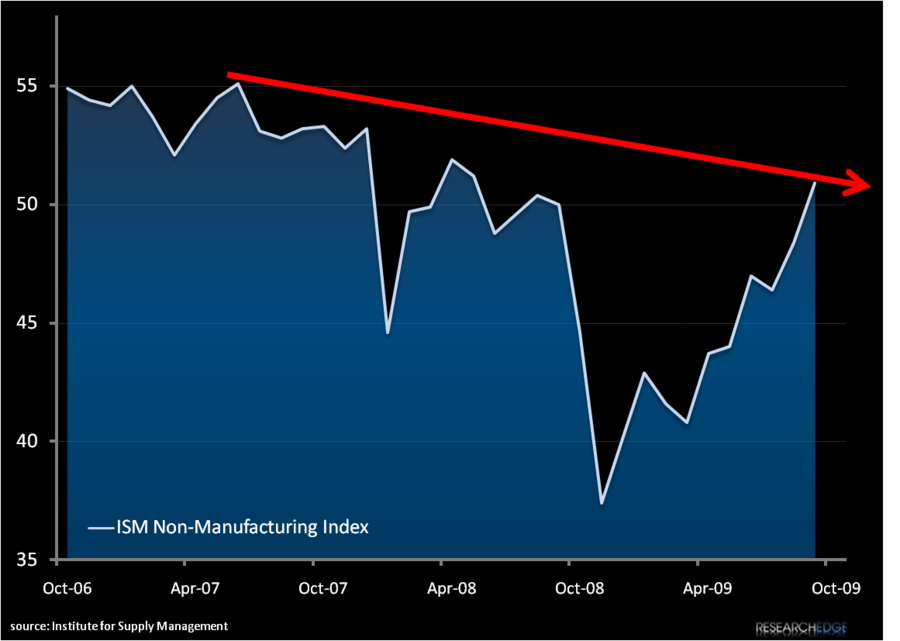

A full year after the last positive reading, today’s ISM Non-Manufacturing Index September reading showed expansion in the US Service Industry sector with a jump to 50.9 from the August reading of 48.4. The improvement, though impressive, was very narrow with just 5 industries reporting growth in September and 13 industries reporting contraction.

Narrow or not this reading is positive. It is also as good as it is going to get.

Gut check: unemployment is continuing to climb, many of the short-term incentives for consumer liquidity like cash-for-clunkers or foreclosure short-sales have reached their full incentive potential and the savings rate is on the rise despite historical low interest rates. In the absence of a catalyst for growth in the US economy in the form of real demand the glass half full brigade are grasping at the only straws they have left—strong equity performance YTD and the appearance of a bottom in the housing market.

The baby boomers are entering the home stretch for retirement with a busted currency, a broken financial system and employment insecurity –these factors WILL create incentive to curtail spending. The ISM-NMI for September is an incomplete rear view of last month’s spending; Wednesday’s measure of outstanding Consumer Credit for August by the Federal Reserve will provide another part of the story.

At 50.9, today’s data was positive by any measure, but it is not enough to change our minds (and we refuse to change the subject).

Andrew Barber

Director