Editor's note: On behalf of everyone here at Hedgeye, we wish you and yours the happiest of holidays. We thank you for your trust and your business and we look forward to another successful year together in 2015.

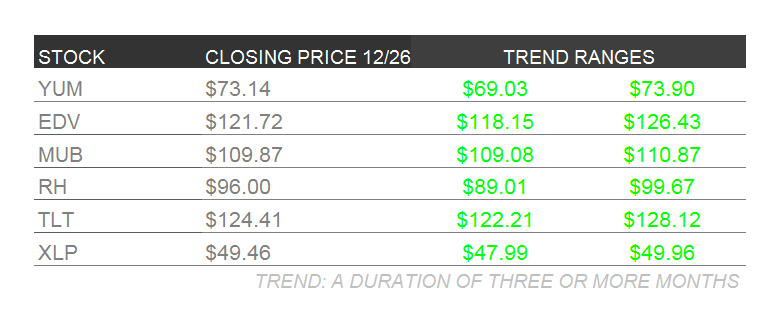

In this week's edition of Investing Ideas, we provide CEO Keith McCullough’s updated levels on our analysts' six current high-conviction long investing ideas. We also feature a special end of the year market recap written by Managing Director Moshe Silver. Our analysts will resume their updates after the holiday.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Investing Ideas Year in Review – The Year We Lost Interest (Rates)

One of the biggest stories this year has undoubtedly been the decline in interest rates, driven primarily (and ironically) by the Fed’s policy to deflate. This year’s game of “Out-Guess the Fed” opened with Janet Yellen taking the helm and promising that monetary policy would slowly return to traditional “hands-off” mode as the economy stabilized.

Hedgeye founder and CEO Keith McCullough welcomed incoming Chair Yellen with a burst of hilarity (Early Look 2/28/14, “Funny Fed.”)

“While it was fun buying everything other than US Dollars as you were outlining your qualitative policy to passively inflate, we have to go out there on the Street today and live in the real world.” Keith wrote, calling Yellen’s program a transparent Policy to Inflate, and a dangerous one at that.

Indeed, the first of our Q1 Macro Themes of 2014 was #InflationAccelerating, as our Macro team read upward pressure in the rate of change in price trends in just about everything Americans put in their mouths, their cars, and their closets. With Bernanke out and Yellen in, Keith called out a Fed policy that remained blind to these pressures, pressures that directly impact the ~ 71% of the US economy represented by The Consumer (that would be You.)

“While it’s both comical and counter-intuitive to the Keynesian economist contingent that you buy bonds when inflation starts to breakout,” Keith continued, “the fact is that’s precisely what you do when the entire world knows the Fed has 0% credibility in fighting real-world inflation. You buy commodities to own inflation. You buy bonds because you know that inflation slows growth. #InflationAccelerating to all-time bubble highs in 2011-2012 drove bond yields (growth expectations) to all-time lows (bonds to all-time highs) in late 2012 too.”

As 2013 drew to a close, there was a surge in the shift away from fixed income and into equities. This was driven partly by concern that Yellen would start selling down the Fed’s morbidly obese balance sheet, coupled with what psychologists call “magical thinking” that new Fed chair Yellen wouldn’t allow the stock market to go down any more than her two predecessors had done.

Writing in our year-end edition on 12/28/2013, senior financial sector analyst Jonathan Casteleyn noted “Worst Bond Outflow In Over 3 Months,” a shift that turned out to be another spectacularly bad decision on the part of many investors. The year-end surge in bond fund redemptions brought fixed income fund flows full circle, from +$5.8 billion per week during the 2012 Bernanke Bubble, to an average negative -$1.4Bn per week by the end of 2013, pushing 10-Year Treasury rates to over 3%.

But the timing of Yellen’s promise of a Return to Fed Normalcy was based on the Fed’s own analysis of the economy (“we’re data dependent”). This made for uncertainty and the equity markets got off to a rocky start. By early February, the Dow was down over 5% for the year, spurred by turmoil in less-developed markets such as Brazil, Turkey and Argentina which crashed for double-digit losses in January, to name but a few.

By early February, market turmoil led investors to assume the Yellen Fed would be forced to continue the dovish policies of her predecessors. Once again US Treasurys and their close proxies – damaged goods though they were – remained the best house in a bad neighborhood.

Hedgeye weighed in with a special Macro update on 2/8/2014 as Macro analyst Christian Drake reiterated Hedgeye’s Q1 Macro Themes of #InflationAccelerating and #GrowthDivergences in light of current major trends in the marketplace:

“Hedgeye’s macro work indicates that commodity prices have begun to break out as other inflationary pressures continue to build. If Fed chair Yellen decides to rescue the equities markets by going back to Quantitative Easing, the impact could re-ignite what has become a Pavlovian response from investors: QE Up, triggering Dollar Down, triggering Yield Chase/Inflation Hedge Assets Up. This would likely spark another round of growth-slowing commodity inflation.”

In the event, there was no announcement of a new QE round. In Fed-speak – or “Fed non-speak” – not saying that the Fed is going to do something is tantamount to saying they are not going to do it. The impact of repeated assurances that the Fed is “data dependent” creates its own mystical aura of uncertainty, particularly as the markets had witnessed the moving of those particular goalposts on more than one occasion. Which data? Dependent to do what? Then there was the expression “extended time,” which caused analytical hullabaloo.

By March, the capital spigots were open again. Hedgeye’s Macro call was that the Fed would keep its foot squarely on the Dovish pedal, pushing equities higher with everything they could muster. Markets seem to have read the situation the same way. Casteleyn again, on 3/18, in his update on TROW: “This continues to dovetail with the ICI fund flow survey which had another positive week of results with $4.9 billion flowing into all stock mutual funds this week, with $3.1 billion of the $4.9 billion moving into U.S. equity mutual funds…” This dovetailed nicely with Chair Yellen’s non-statement that same week that rates could rise “eventually,” tempered by her emphatic reminder that the Fed’s economic forecast was just a forecast.

This was a level of murkiness too dense to dignify with the name “obfuscation.” In plain English: “We think the economy might move in one direction, unless it doesn’t. If that does happen – or if something else happens that we never thought of – it could result in higher interest rates at some indeterminate time in the future. Or not. Unless we’re wrong.” You too could be a Fed governor.

The constant stream of wind from the Fed did the trick: it inflated an equities bubble that floated along pretty well until breaking down in July, when ten consecutive weeks of outflows in US equity funds culminated in their biggest weekly outflows in 79 weeks. That first week of July saw $8.8 billion in outflows from equity funds, versus only $3.2 billion in new subscriptions to fixed income mutual funds and ETFs.

Hedgeye’s Macro process anticipated these shifts, moving our Investing Ideas subscribers into TIPs, the inflation-adjusted Treasurys ETF (6/7).

Investor fears around equities, combined with available cash, combined with the convergence of signals in Hedgeye’s signaling process, put our subscribers firmly into Treasurys when we moved from the TIPs into the iShares 20+ Year Treasury Bond ETF (TLT) consistent with our Macro view that the rate of change in reported inflation and inflation expectations would level off.

As our declining rates thesis proved out and picked up steam over the course of the year, we also added the Vanguard Extended Duration Treasury ETF (EDV) to Investing Ideas on 9/5, followed by the 1Shares Muni Bond ETF (MUB) on 10/22. We see this trend continuing into Q1. Short of a Fed rate hike, there’s no force out there with the oomph to reverse this trend, particularly with global growth decelerating and disinflationary trends pushing capital flows into the one remaining unbreakable piggy bank, which is the US Treasury debt market.

Inexplicably – or maybe all too obviously – we remain in the distinct minority in this view. That in itself should indicate that we are probably right.

Our robust Macro work differentiates Hedgeye from the rest of the herd in a big way. But we have also had some successes producing single-name Alpha (that’s hedge fund-speak for “we picked some stocks that did really well.”)

Star retail sector analyst Brian McGough added Restoration Hardware (RH) to Investing Ideas over a year ago (9/6/2013) at a closing price of $74.62. The stock recently traded above the one hundred-dollar mark. McGough says RH has become the category killer in home furnishings, combining high quality mega-store locations (up to 35,000 square feet) with a well managed catalogue and on-line business. RH’s nimble and high-class approach to their business line, combined with the right demographics for new family and new household formation, put this company on track to potentially double from here, then double once more over the coming three years.

Back to our All Things Yield theme, investors who stayed with our So-Simple-A-Government-Employee-Can-Do-It strategy of sitting out the last, vapid gasps of a late cycle equity bubble have been rewarded with low volatility, double-digit returns since we first moved decisively into the Treasurys ETFs. Unless you are absolutely committed to paying for your investment professionals’ Christmas gifts by way of commissions, you would do well to consider sitting tight with those same positions going into the new year.

One key tool in the Hedgeye process is our fundamental Four-Quad model, measuring the interplay between Growth, Inflation, and Government Policy. Where standard Wall Street models tend to combine academic economic theory, with valuation calculations, with a constant search for the elusive Paradigm Shift (“this time is different!”), Hedgeye’s framework is Math (2+2 = 4 over and over again), Behavioral Psychology (tulips got expensive because everyone saw their neighbors bidding them up – ditto stocks) and History (as Mark Twain said, it doesn’t repeat, but it does rhyme).

For much of this year, the US has been stuck in Quad #3: Growth Slowing and Inflation Accelerating. This is the Sargasso Sea of monetary and fiscal policy. There is really no good policy move. Try as they might, policy makers end up having to sit this out as the economy grinds out its problems. Time heals all wounds – but at the expense of an angry electorate when Washington can’t fix what’s wrong with the economy.

Hedgeye’s Macro team doesn’t yet see a meaningful likelihood of rates turning up in the first half of 2015. Against a growing chorus of certainty, we think the Yellen Fed might be forced to address the current slow-growth reality. “Slow growth?!” Well, yes. Like you, we saw the big Q3 GDP number but from a rate of change perspective, we think growth slows from here. Oh yeah, and there’s thing called The Rest of the World (i.e the other 75%+ of Global GDP) that remains in discrete deceleration. Hedgeye’s macro work sees rates of change continuing to erode on overall economic growth. Even the Fed will ultimately have to acknowledge that.

Even if the Fed chooses to poke the body economic to determine whether there’s any life left – we’d expect an opening gambit of a 25 basis-point hike – take a look around you.

European shares are down over ten percent from their high this year, and the euro is looking mighty uncertain. Elsewhere, the iShares emerging markets ETF (EEM) is down double digits, including such standouts as Russia (down over 42% from its high this year), to Ukraine (down over 20% from its high), to Argentina (down 34%), to Mexico (down over 19%) and even China coming into year-end down about 5% from its recent highs.

You have to live somewhere, and if you don’t like the neighborhood this house is in, it’s still the only one without a leaky roof. As the US equities markets march higher, volatility has stepped up, while trading volume has run counter to the direction of prices – never a bullish sign, no matter who your astrologer is.

Treasurys will likely continue to be in mega demand around the world. Will there be a shortage? Consider this: if Yellen actually decides to unwind, the Federal Reserve will become the Seller of Last Resort.

Merry… uh… whatever…?