Here's a quick look at some of the top videos, cartoons, market insights and more from Hedgeye this past week.

HEDGEYE TV

McCullough: Why I’m Using the Word “Recession” for the First Time This Year

In this excerpt from the Q&A portion of Monday's Morning Macro Call for institutional subscribers, CEO Keith McCullough says that Fed Chair Janet Yellen could make a move that puts the U.S. in recession.

Keith's Macro Notebook 12/22: Yen | Russia | Sentiment

Hedgeye CEO Keith McCullough shares the top three things in his macro notebook Monday morning.

McCullough: Serious Lack of Momentum in the Momentum Stocks | $GPRO $LOCO

In this brief excerpt from Tuesday’s Macro Call for institutional subscribers, Hedgeye CEO Keith McCullough notes the similarities between current and earlier bubbly periods and highlights two momentum stocks in particular which are representative of the current climate.

CARTOON

This Won't End Well

The Gong Show that is Russia continues. The stock market is in a deep hole, down more than 40% this year.

CHART

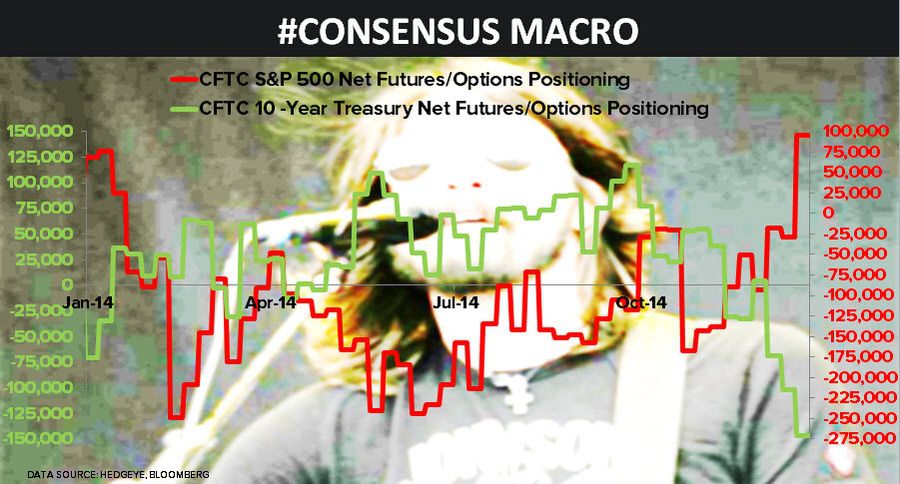

Consensus Macro Positioning $SPX $TLT

"I’ve used the net long/short positions of CFTC Non-Commercial positioning as a contrarian Global Macro indicator for years," wrote CEO Keith McCullough in Monday's Morning Newsletter.

Yield Spread Compression #NoWorries

YIELD SPREAD – the belly of the curve is even flatter, but the big one almost every objective strategist monitors (10s/2s spread) compressed another 7bps Tuesday morning to a fresh YTD low of +146bps wide (-38% YTD).

POLL OF THE DAY

Will the 10-year Treasury yield go below 2% at any time in the 1st quarter of 2015?

Our biggest call by far this year has been bucking the consensus tide on the direction of Treasury yields. While others said yields had nowhere to go but up, we remained resolute that yields were in fact, heading lower. So, as we head into the new year, we wanted to know what you think 2015 has in store.