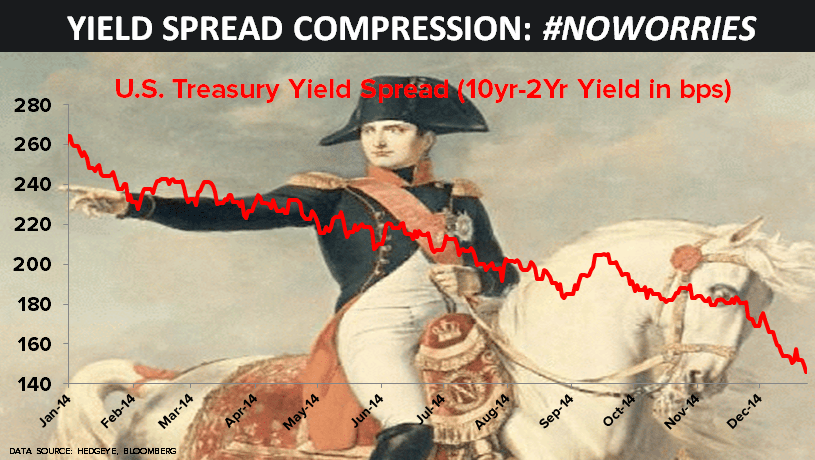

YIELD SPREAD – the belly of the curve is even flatter, but the big one almost every objective strategist monitors (10s/2s spread) has compressed another 7bps this morning to a fresh YTD low of +146bps wide (-38% YTD)

YIELD SPREAD – the belly of the curve is even flatter, but the big one almost every objective strategist monitors (10s/2s spread) has compressed another 7bps this morning to a fresh YTD low of +146bps wide (-38% YTD)

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.