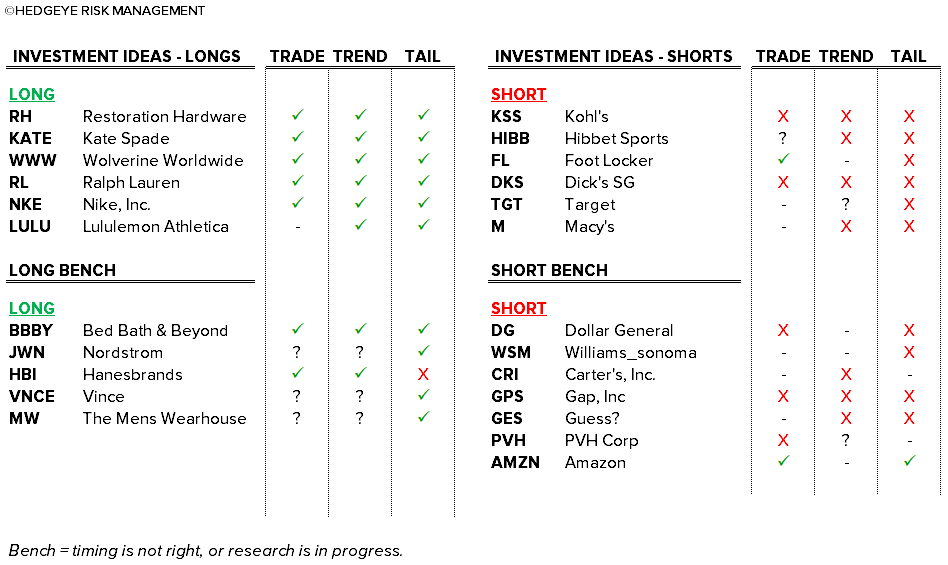

HEDGEYE RETAIL IDEA LIST

Several changes to the Idea List this week.

- We put all athletic retailers in our Core Short list. This follows our Athletic Black Book last week where we outlined the changes happening with distribution in that space, and how FL, HIBB and DKS are uniquely positioned to fail.

- We removed DDS from our Short Bench. With HBC making noise about acquiring the company, it hardly makes sense for us to continue to hold our breath waiting for an entry point.

- We contemplated moving KATE ahead of RH on our idea list into the #1 slot -- not because of lack of confidence in RH, but because we think that there's more controversy around KATE over the near-term. We're going to keep our positioning as is. But if KATE weakens or RH plows forward, we might make the switch.

ECONOMIC DATA

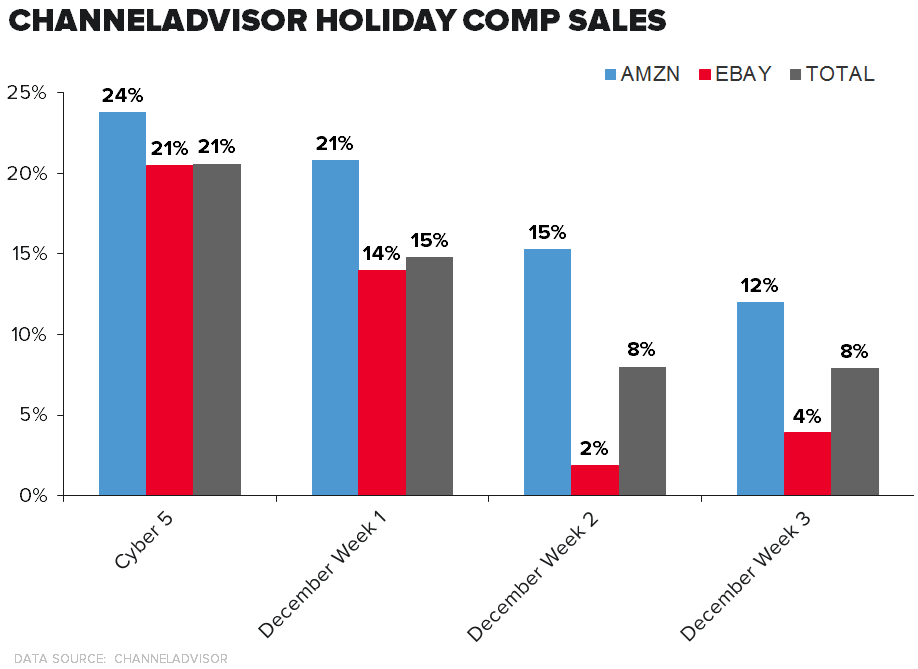

Takeaway: A big rebound in sales for the week, but it follows two big weekly declines in the context of an intermediate downtrend. The point there is that with sales trending down so much heading into the biggest Holiday week, it makes sense that retailers would really turn the discounting machine into overdrive to have any shot at hitting numbers and prevent a glut of inventory in January.

We're seeing the same here out of the ChannelAdvisor numbers -- which show e-commerce trends. The consistency in spending decline is clear as day.

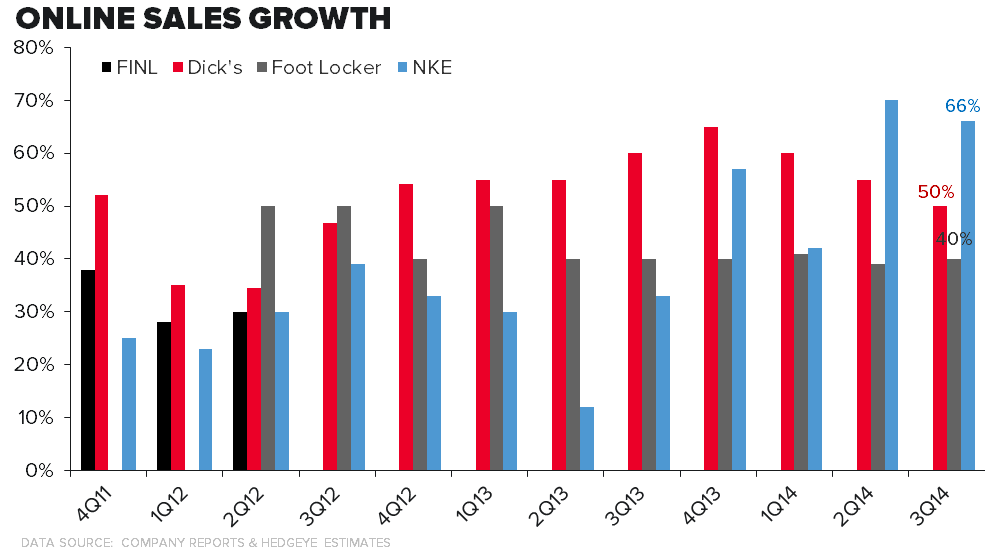

NKE, FL, DKS, FINL - e-Commerce Trends

Takeaway: Following up on a major theme of our Athletic Black Book here is a look at e-Commerce sales growth for the relevant companies. If you are wondering when Nike's commitment to DTC starts to have an effect... it's now.

Dick's and Foot Locker occasionally report their main banner performance, which outpaces their consolidated company e-commerce growth. We have used that data here and included our estimates where necessary.

As a reminder HIBB does not have an e-commerce business. That's a problem.

The key takeaway is that there have only been two quarters in history where Nike outgrew its wholesale partners with online sales. Those two quarters just happened. And we're going to see a third, and a fourth...etc...

OTHER NEWS

BABA, COST - Alibaba’s Tmall Global Site Stumbles

(http://www.wsj.com/articles/alibabas-tmall-global-site-stumbles-1419274439)

M, VFC - Ranking the Top 20 Finance Chiefs

(http://www.wsj.com/articles/the-top-20-finance-chiefs-1419297855)

DDS - Hudson's Bay could wrap up Dillard's in 2015

WMT, TGT - Walmart stores busy, Target stores, not so much

(http://www.thestar.com/business/2014/12/22/walmart_stores_busy_target_stores_not_so_much.html)