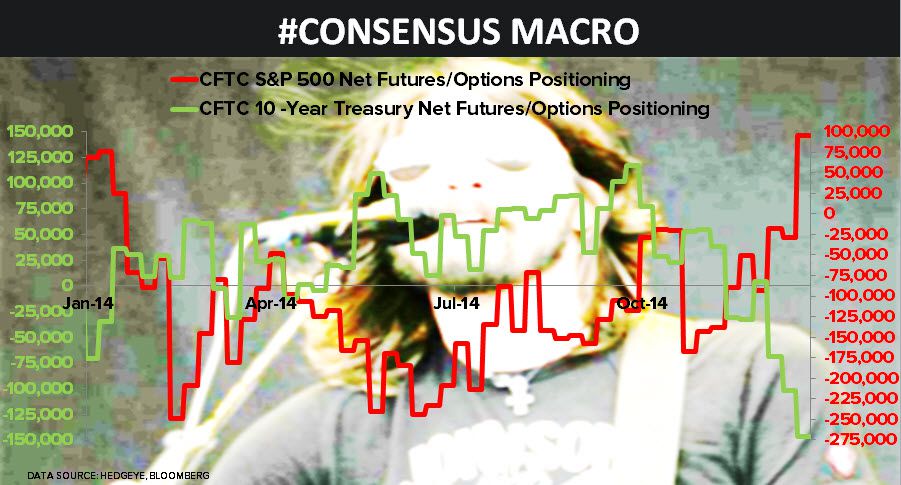

"I’ve used the net long/short positions of CFTC Non-Commercial positioning as a contrarian Global Macro indicator for years," wrote CEO Keith McCullough in today's Morning Newsletter.

"I’ve used the net long/short positions of CFTC Non-Commercial positioning as a contrarian Global Macro indicator for years," wrote CEO Keith McCullough in today's Morning Newsletter.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.