Editor's Note: This is a brief excerpt from Hedgeye CEO Keith McCullough's morning research. For more information on how you can subscribe click here.

3 big things happened in Europe this morning:

- Germany reported deflation of -0.9% year-over-year in the NOV PPI

- Central planning talk of making QE the periphery’s burden

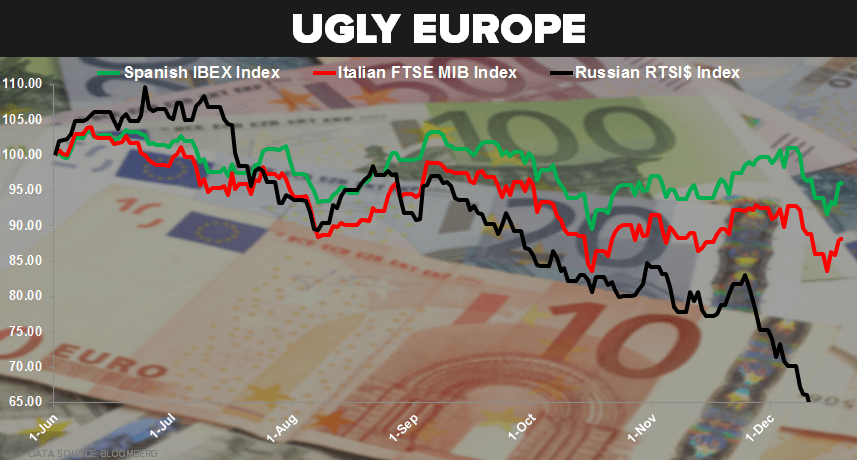

- Italian, Spanish and Russian equity markets all resumed their bearish TREND declines

We do not believe that ECB President Mario Draghi can get a “Big Thing” done in January to stem this European Equity drawdown.

In addition, as we outlined in #EuropeSlowing (one of our three Q4 Macro Themes) our view remains that inflation via currency debasement does not produce sustainable economic growth. We believe select member states will struggle to implement appropriate structural reforms and fiscal management to induce real growth.