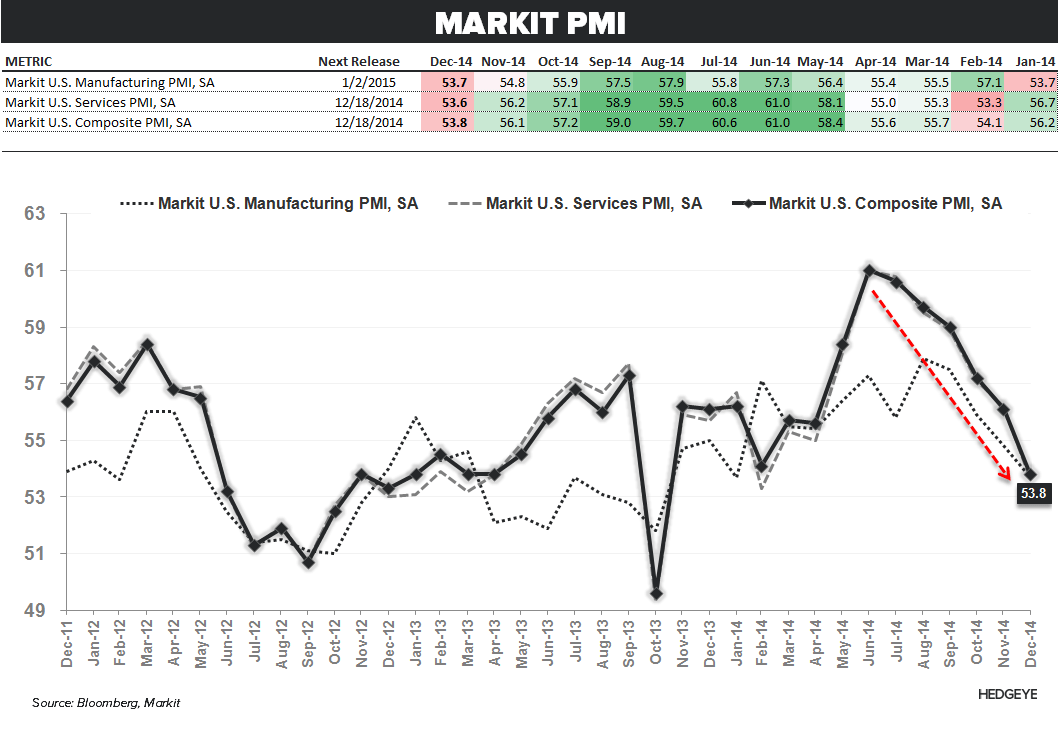

The U.S. has been the relative outperformer on the global Macro fundamental front and we highlighted the ongoing strength in the high frequency labor data this morning (HERE) but no month/quarter/year-end markup for domestic manufacturing as the data continued to slow into December.

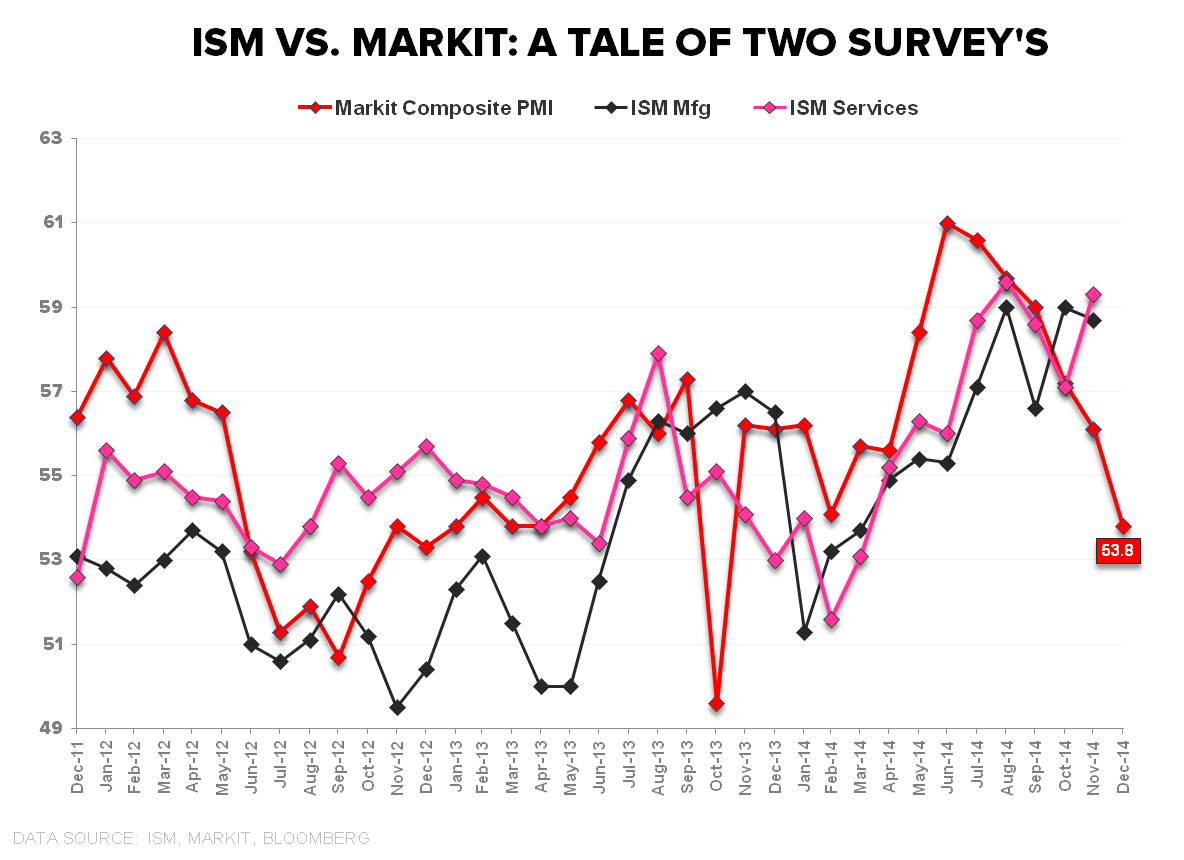

The Markit Composite PMI slowed in December alongside sequential slowing in both the manufacturing and services components. While holding above the expansion demarcation line of 50 for a 14th month, New Orders in December dropped to the lowest reading since October 2012 while the headline reading retreated for a 6th consecutive month, slipping to the lowest level since October of last year.

Alongside a reversal in here-to favorable seasonals and a deceleration in domestic mfg and export demand, we expect the reported ISM/IP data to follow the Markit reading lower in the coming months.

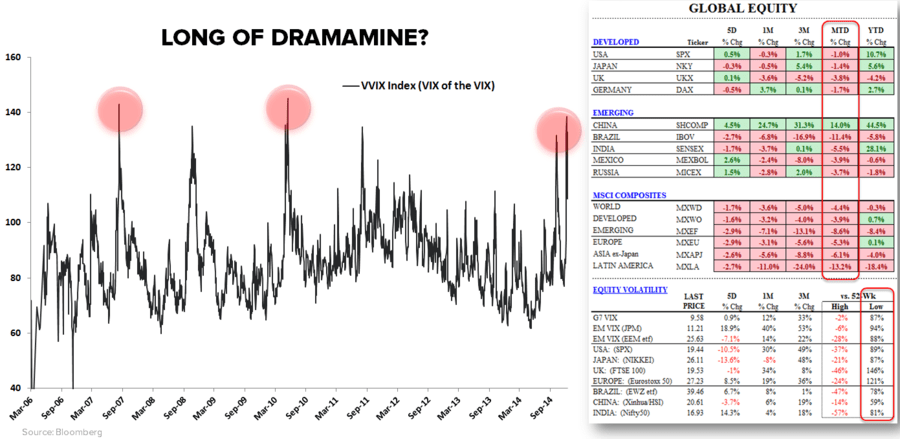

Looking globally – and despite the whipsaw action in markets – the trend towards disinflation and decelerating growth remains predominate as the negative growth and inflation estimate revisions continue to roll-in.

Oversold market bounce but with cross-asset class volatility ramping, the VVIX (VIX of the VIX) in breakout mode and the currency war race-to-the-bottom in full re-crescendo, being long of Dramamine futures…or its more liquid little brother, the long-bong (TLT)…remains our favored macro position into year-end.

Have a good night,

Christian B. Drake

@HedgeyeUSA