Disappointing Guidance

Today, DNKN announced that it expects Dunkin’ Donuts U.S. full-year same-store sales growth to be approximately +1.4% in 2014, below the current +1.8% consensus estimate. This guidance implies that 4Q same-store sales are running in the +0.5-0.8% range, well below the current +2.2% consensus estimate. In 2015, the company expects to deliver full-year same-store sales growth of +1-3% in the U.S and adjusted EPS of $1.88-1.91 (current consensus estimate is $2.02).

Management broadly alluded to a couple of headwinds its business is facing: “Dunkin' Donuts' 2014 U.S. comparable store sales and transactions remained positive, although not as positive as we hoped because of continued pressure on the consumer and decelerating sales of packaged coffee in our restaurants. We expect these trends to continue into next year.”

Is Starbucks Immune?

The obvious question that arises from this press release and aforementioned guidance is whether or not Starbucks is seeing similar pressure. Many people will roll their eyes at this notion as “the brands have different consumer bases,” but the fact of the matter is, the correlation between Dunkin’ Donuts and Starbucks same-store sales is a respectable 0.75 since the beginning of calendar 2011. Call us crazy, but it isn’t clear that Starbucks is immune to some of the softness Dunkin’ is facing.

What’s Really Wrong with Dunkin’?

DNKN sales trends have been decelerating for quite some time now. In fact, two-year trends would suggest comps have been steadily decelerating for the past three years. It is now abundantly clear that 2014 has been a real pain for the company and management constantly cites a difficult macro environment as the reason for the slowdown. Intense competition in the QSR segment could be partially to blame, but it certainly doesn’t tell the whole story. This rationale has also been extremely inconsistent with the improving jobs outlook, consumer confidence, and declining gasoline prices.

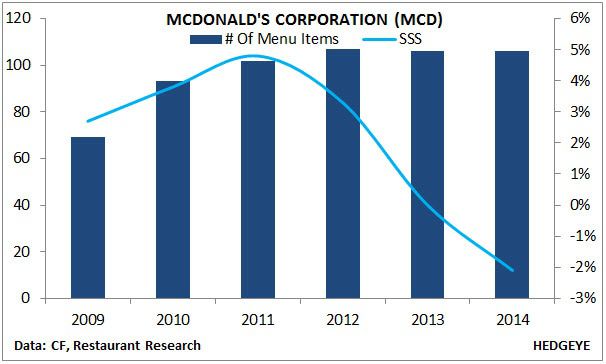

Menu Proliferation Can’t Be Helping

Pulling back the curtain on the menu complexity at Dunkin’ reveals a much bigger problem for the company than the current competitive environment. Similar to MCD and (dare we say) SBUX, DNKN’s sales trends have decelerated as menu proliferation has accelerated. As we outlined in our Starbucks deck back in September, concepts that see a significant increase in menu items tend to see a coincident deceleration in comps (and vice versa). Ask McDonald’s how well menu expansion has gone for them!

Upshot

Needless to say, today’s DNKN news certainly makes us feel more comfortable with our SBUX short. Expectations are elevated after the recent Starbucks analyst meeting that the concept will see an acceleration in traffic trends during the holiday period. At 26x forward P/E and 14x forward EV/EBITDA, this isn’t something were willing to bank on and, so far, the news flow around the holiday season has favored the short side of the trade.

Howard Penney

Managing Director

Fred Masotta

Analyst