“The two most powerful warriors are patience and time.”

-Tolstoy

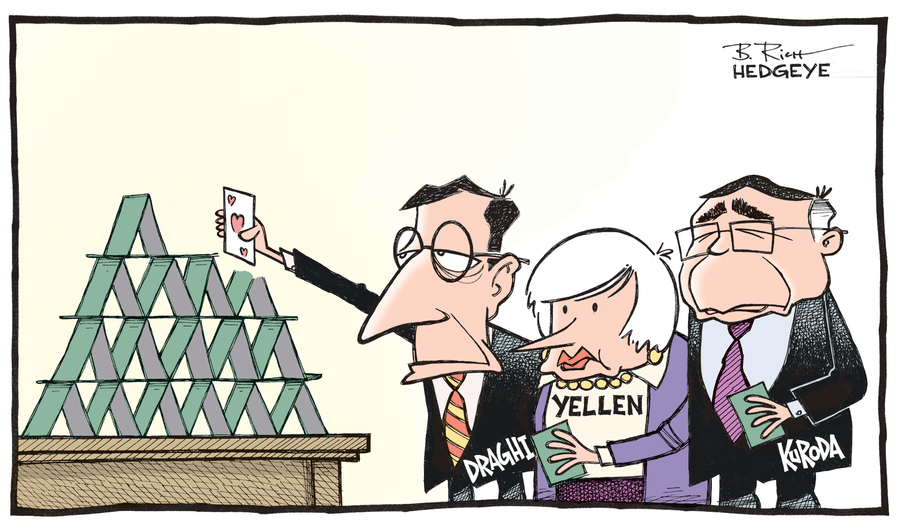

In case you didn’t know that I’m not a fan of centrally planned markets and economies, now you know. My long-term risk management call remains that any asset price inflation that is based on perma-planning will end in some form of a deflationary shock.

And while I know everything is rainbows and puppy dogs these days in the US economy (it’s going to “de-couple” from all of Global Macro markets, but bounce when they do!)… even the most avid perma bull on global growth should note that the Top 5 Stories on Bloomberg this morning have everything to do with central planners bailing markets out of the “everything is awesome” narrative.

Janet Yellen leads headlines this morning, followed by Mario Draghi (Europe), Shinzo Abe (Japan), a Swiss dude you probably don’t know (Switzerland cut interest rates to negative), and, of course, Vlad – as in Putin. Other than what went violently wrong in markets in the 1st two weeks of both October and December, what could possibly go wrong? #Patience, Risk Managers. Patience.

Back to the Global Macro Grind…

Away from her ridiculous comment that the crash in Oil is “transitory” (she can’t call bubbles, but she can call crashes… boil the oceans, part the heavens, etc.), I must give Janet Yellen props for having the #patience to wait until year-end to cut her forecasts (again).

This is big news for Hedgeye as the Fed, once again, effectively agrees with our core macro call that:

- Growth is slowing

- Inflation is slowing

I recapped the sell-side forecasts for you on Tuesday. Here are the Fed’s for 2015:

- GDP Growth cut from 3.5% to 3.0%, lowering the range to 2.6-3.0%

- Inflation cut from 2.2% to 1.9%, lowering the range to 1.0-1.6%

Notwithstanding that the Fed’s forecasts on growth and inflation have been wrong 60-70% of the time since Bernanke/Yellen took over the central planning bureau, the point here isn’t about good or bad – it’s about better or worse.

One of my Partners here @Hedgeye (Josh Steiner) coined that one-liner… and since I’m a rate of change guy, I like it. It’s simply another way to say the same thing. I don’t care much about absolutes – I care about the slope of the line. Is it slowing or accelerating?

Clearly, both locally and globally, the rate of change in both growth and inflation expectations are slowing. That’s why US, German, and Japanese bond yields continue to fall. That’s also why FX, High Yield, Commodity, and Equity Volatilities continue to accelerate.

“So” (Janet said that every other sentence yesterday, proving she’s in the tank with #OldWall groupthink), now that most things Global Macro have corrected (and bounced) again, what do we do next?

- As Long-term Risk Managers (Long-term Investors, I know you like that term!) we want to have #patience

- From Oil to Energy stocks, to EM and High Yield, we want you to recognize that #Deflation’s Dominoes take time

What we don’t want you to do is very straightforward:

- Don’t chase high, and freak out low

- Don’t believe the Fed’s forecasts (front-run them)

That’s it – just #FadeBeta (when the non-consensus view on growth and/or inflation is the most probable one).

Don’t be a Consensus Macro perf chaser who gets stimulated above the 50-day moving monkey and depressed below it. That is not going to make you a warrior of the alpha generating gridiron. No Sirs and Madames. That is going to make you mentally weak.

I don’t do weak. And I don’t do drawdown risk either. If I can proactively prepare you for it, that is…

If you nailed every 50 handle whip-around in spooz perfectly for the last 2 weeks, congratulations. We had a great year here, so send me your docs and I might give you some of my money to manage. If you did not, and stayed the course of patient, dynamic asset allocation:

- You sold some of your long duration bonds at 2.03% on the 10yr

- You bought some #Quad4 US Equity Exposure (Healthcare or Utilities were 1-2 for us this week)

- You shorted more Burning Yens and Euros high, against a net long US Dollar FX asset allocation

I didn’t have to nail every US stock market move to get that right in our asset allocation model. I just had to have the patience to not buy the November highs in US stocks and/or get shaken out of my Long Bond and US Dollar allocations on the recent November pullbacks.

Patience and time. They work in risk management as well as your best long term ideas do. Be a powerful warrior versus the tyranny of centrally planned momentum chasing consensus.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.03-2.19%

SPX 1

VIX 16.33-25.27

USD 88.15-89.67

Yen 116.16-121.11

WTI Oil 52.49-59.91

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer