We remain very cautious on DRI shares and believe expectations of a 2H15 recovery are not grounded in reality. The bottom line is that the current consensus FY15 EPS estimate of $2.28 is about $0.28 too high.

As it stands, Darden’s management team is being asked to manage in an extremely difficult environment. Interim CEO Gene Lee is trying to fix the company, while simultaneously interviewing for the full-time CEO position. This not only poses inherent conflicts in the internal discussion of current trends, but it also strips him of the authority needed to make pursue value enhancing initiatives.

While most of the street is gloating about Olive Garden’s results this quarter, we have a very different point of view. In fact, we’d argue that the chain had a disastrous quarter. Though the sales trends appear to be improving, traffic and average check declined 100 bps and 30 bps, respectively, during the quarter. This is a worrisome combination for any restaurant company and the results showed in Darden’s P&L. Despite reporting strong comp growth and achieving, we assume, notable flow through at the majority of its other brands, consolidated restaurant margins declined 60 bps to 18.6%.

You need not look past the press release to understand that Olive Garden had a weak quarter.

The 1Q15 press release was very specific about the Olive Garden recovery:

"We are pleased with the progress we are achieving across our brands, particularly at Olive Garden," said Gene Lee, President and Chief Operating Officer of Darden. "The Olive Garden Brand Renaissance is well underway, and the improvements we are seeing in guest satisfaction and traffic trends reinforce our confidence in Olive Garden's potential."

The 2Q15 press release actually omitted comments about the Olive Garden recovery:

"Our brands performed well during the second quarter," said Interim CEO Gene Lee. "We have been working diligently to execute our strategy, including getting back to basics while delivering the best possible guest experience. It is starting to show in both improved revenue and profitability. While it's still early, we believe our renewed focus on operating fundamentals, coupled with our more streamlined support structure, will help us continue to grow and capture market share."

The most damning piece of evidence suggesting the lack of an Olive Garden recovery is the unexpected halt of the remodel program. While we agree this needed to happen, it was a critical component of the once highly-esteemed Brand Renaissance plan, which appears to be fizzling away.

Street Suggests a Turnaround, OG Metrics Suggest Otherwise

- Same-store sales +0.5%

- Traffic -1%

- Average check -0.3%

- Consolidated restaurant margins declined 60 bps year-over-year to 18.6%

- The remodel program has been put on delay due to insufficient returns

Given the operational short fall at Olive Garden, management consistently referred to opportunities with its real estate portfolio as well as the potential spinoff of other non-core assets. While these things are nice to hear, they aren’t what’d yield the most shareholder value at Darden (fixing Olive Garden). Importantly, none of the above will occur prior to getting a new CEO and CFO.

It’s been two months since Starboard took control and the lack of updates or disclosure around the CEO search has been discouraging; in fact, we haven’t seen or heard anything that suggests they are close to naming one. We find this surprising and believe it may have been a major strategic error on Starboard’s end not to have one in place at the time of its takeover.

The clock is ticking and it is getting more expensive to fix the company with each passing day.

The Good in 2QF15

- Top line and bottom line beat of 76 bps and 238 bps, respectively.

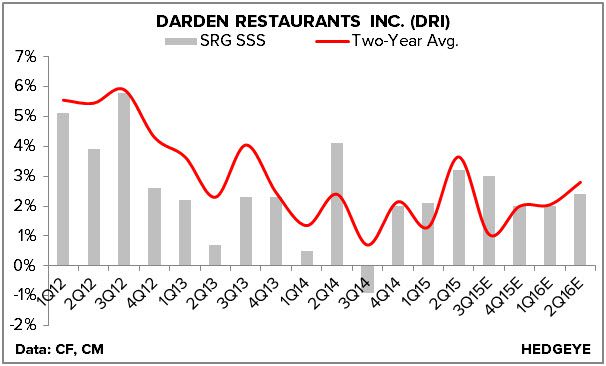

- Positive same-store sales trends across the portfolio (excl. BB): Olive Garden +0.5%, LongHorn +2.6%, SRG +3.2% (The Capital Grille +5.0%, Eddie V’s +4.9%, Yard House +3.7%, Seasons 52 +1.2%. Bahama Breeze -0.6%).

- Guided to +1-2% system-wide same-store sales growth in FY15 versus the consensus estimate of +1%.

- Tightened the low-end of its FY15 EPS guidance range to $2.25-2.30 versus $2.22-2.30 prior.

The Bad in 2QF15

- FY15 will be a transition year, and nothing more.

- There has been no mention around the timing of naming a new CEO and CFO.

- Still lacking a strategic long-term vision.

- There is no sign of a Brand Renaissance at Olive Garden; difficult to decipher between success of initiatives and broader industry trends.

- Deferring the Olive Garden remodel program due to insufficient returns.

- Management expects 2H15 food inflation to be up +2-2.5%, up from prior guidance of 1%.

- Restaurant level margins deleveraged 60 bps to 18.6%, despite strong comp growth across the majority of its portfolio.

Howard Penney

Managing Director

Fred Masotta

Analyst