This note was originally published at 8am on December 03, 2014 for Hedgeye subscribers.

“The key to wealth preservation is to understand the complex processes and to seek shelter from the cascade.”

-James G. Rickards

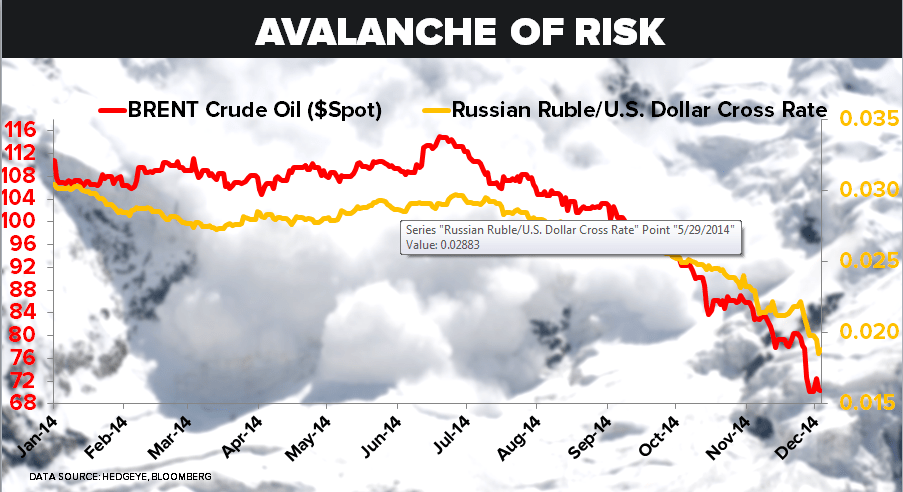

If you’ve proactively prepared your portfolio for the phase transition of market expectations from inflation to #deflation, congrats. Not being long cascading things like Oil, Energy stocks, and Russian Rubles has been key to your wealth preservation in the last 3 months.

But how many people really think about their net wealth this way? How many people start with Warren Buffett’s 1st Rule of Investing: “Don’t Lose Money?” How many services that you pay for are equipped to monitor complex systems in a dynamic way so that your expectations of risk are constantly changing alongside analyzable factors?

I spent some time discussing these questions at the annual Hedgeye Company Meeting yesterday in Stamford, CT. In order to illustrate how risk manifests slowly, then all at once, I showed what I think was a fantastic 4 minute video on Glacial Calving (https://www.youtube.com/watch?v=hC3VTgIPoGU). I’d love to see how Draghi and Yellen would centrally plan smoothing that.

Back to the Global Macro Grind…

Yesterday I used the snow-pack metaphor to discuss market risk factors that have a rising probability of cascading into asset class draw-downs. The idea was inspired by my friend Jim Rickards, who wrote an awesome chapter called “Maelstrom”:

“An avalanche is an apt metaphor of financial collapse. Indeed, it is more than a metaphor, because the systems analysis of an avalanche is identical … An avalanche starts with a snowflake that perturbs other snowflakes, which, as momentum builds, tumble out of control… The dynamics are the same, as are the recursive mathematical functions used in modeling the process.”

-The Death of Money, pg 265

Unless they are just looking at “charts”, I think almost everyone who gets paid real money to pick stocks, bonds, commodities, etc. has a bottom-up process to analyze securities. In fact, some are quite impressive. But how impressed are you with the systems of analysis our profession uses, from a top-down perspective?

Going on 16 years into this, my experience has been a learning one. The more I read, the less I know. But the more I observe how consensus thinks about top-down macro risks that are developing in this dynamic ecosystem of market expectations, the more opportunity I see in learning more of what not to do, out loud.

You see, while I certainly don’t make the same “money” I used to make on the buy-side, I am making a difference in my learning experience. When you open yourself up to the critique of the crowd (daily), you’re actually forced to learn faster.

In terms of big bang losses of wealth (draw-downs), the lessons, unfortunately, tend to be more expensive for the many, and profitable for the few. That’s why I think making money at the all-time highs in asset price inflation becomes next to impossible, without protecting for the downside risks associated with an avalanche (deflation) like the one we just saw in Energy markets.

Moving along…

Never mind snowflakes, there are two big snowballs that are going to hit you square in the forehead on Thursday and Friday:

- Thursday: European Central Bank (ECB) decision by Draghi

- Friday: US Jobs Report for November

In isolation, even for people who don’t do macro (but have a macro opinion on everything!) both of these events probably matter. From an interconnectedness perspective, fully loaded with time/price for both Euros and Yens relative to where European and Japanese equity markets are right here and now, these events matter as much as any we’ve seen in months.

Here’s the system’s setup:

- Japanese stocks (Nikkei) are signaling immediate-term TRADE overbought with a risk range of 16,945-17,741

- European Stocks (EuroStoxx 600 Index) are signaling immediate-term TRADE overbought with a risk range of 337-351

- Both the Euro and Yen are signaling immediate-term TRADE oversold vs. USD at $1.23 and $119.56, respectively

In other words, measuring the system’s risk within a “risk range” (where being at the top and/or bottom end of the range increases the probability of a short-term reversal), the probability is as high as it’s been of seeing a big macro reversal.

There’s that word again, probability…

If you’ve never gone heli-skiing on a mountain with identifiably risky snow-pack factors, try it and you’ll get my point. I’m not saying you are going to break your leg going down a certain path – I’m saying some paths/situations have higher probabilities of that happening than others!

Whether you are skiing, or risk managing your portfolio alongside already cascading asset class paths (like high-yield Energy stocks, Silver futures, Brazilian stocks, etc.), you should always be asking yourself a lot of questions:

- What if Draghi doesn’t deliver the drugs?

- What if Japanese election sentiment forces Abe to tone down the currency burning?

- What if the US Jobs reports misses, and the Dollar corrects from its overbought highs?

There are obviously a lot of questions to ask yourself, all of the time – and maybe that’s why some people don’t “do macro” the way we do. It requires a ton of rinse/repeat systems analysis, yes. But, more importantly, it always puts you at the epicenter of the uncertainty of the system… and stock picking tends to “feel” more certain than that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.16-2.30%

SPX 2032-2078

Nikkei 16945-17741

EUR/USD 1.23-1.25

Yen 117.41-119.56

WTI Oil 64.55-70.36

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer