“Skeptical of Oil & Gas Capital Spending…Energy-related capital spending looks like ‘mining capital spending-lite’”

– Hedgeye Industrials 4/21/2014 CAT: Defining Differences & The Segment Formerly Known As Power Systems

Overview

2015 is not shaping up well for CAT. While some other industrials offer exposure to pending declines in upstream oil capital spending, we think CAT has greater exposure than the market appreciates. We also believe CAT provides broader positives as a short/underweight, such as exposures to other resources-related capital equipment, likely credit losses, and problematic corporate controls. We have been bearish on CAT since Hedgeye Industrials launched in 2012, and the tail of the thesis – declining energy-related capital spending and credit issues at its captive finance subsidiary – is finally coming into view.

Consensus estimates for CAT’s 2015 EPS have hardly budged since late October. This is odd, since expectations for 2015 upstream oil capital spending, a key CAT end-market, have certainly declined. CAT provided its initial 2015 top-line guidance with its 3Q 2014 earnings report, calling for, give or take, zero growth. Consensus just assumed margin expansion in 2015, translating that flattish top-line guidance into 8% EPS growth.

Excluding a transaction or similar rabbit-out-of-the-hat solution, we expect both sales and EPS to be lower in 2015 vs. 2014. We think something in the $5.00 -$6.50 range is a reasonable expectation for the initial guide in January vs. current consensus of $7.00. Our guess is that management will want to set initial expectations low to avoid a repeat of the 2013 serial guidance cuts.

We really wonder if current holders have examined to whom CAT has provided financing in its quest to sell equipment. CAT Financial has disclosed a “material weakness” relating to “Allowance for credit losses”, although the disclosed adjustments so far have been fairly small. Caterpillar Financial has ~$35 billion in assets (although we do not hear much about it) and lends to mining and oil/gas companies, too. There will be credit issues, in our view. Losses at captive finance companies are typically greeted with a mix of confusion and disdain in the Industrials sector.

Here is a brief summary of why we expect the 2015 guide to come in well below consensus, and below anticipated 2014 results:

- Resource Industries: We expect Resource Industries to show further modest revenue declines and a segment loss in 2015, as oil sands capital spending should weaken, MATS regulations should prove an incremental negative for coal demand, and many mined mineral prices, like iron ore, have fallen further. Mining equipment prices should continue to be under pressure, as we understand it. Financing also is likely to be less available/attractive. Optimism around the cessation of the dealer destock seems misplaced in a market with slackening demand.

- Energy & Transportation: We have long expected a decline in oil & gas capital spending to follow the decline in mining capital spending, but the recent drop in oil prices locks that in for 2015. We think the market actually underestimates the relevance of upstream oil and gas capital spending for CAT. Gensets, drilling engines, fire pump engines, well service engines/pressure pumps, and transmissions add to the exposure, along with the aftermarket sales on these often overworked engine platforms. While Tier 4 Final will have a disclosed negative impact on locomotive sales, it will also impact other categories of very large engines, like gensets. The spike in North American E&T sales growth supports the view of a broader 2014 Tier 4 Final pre-buy.

- Construction Industries: While Construction Industries is largely insulated from the decline in resource-related capital spending, it faces very tough comps in 2015. Dealer inventory builds supported record 1H 2014 margins. Improving on 2014’s strong performance may prove challenging, particularly if dealer inventory actions are less supportive. Emerging market demand may well continue to deteriorate, too.

- Financial: Caterpillar Financial has lent money to a number of mining projects, as discussed here. While oil and gas financing exposure is difficult to quantify, it has presumably been a meaningful part of the portfolio. Asset growth has slowed, and we expect higher allowances in 2015.

Are investors missing CAT’s upstream exposure?

We think that E&T has more upstream exposure than investors realize. First, the margins correlate reasonably well to metrics like rig count, as best we can estimate.

Second, some oil and gas sales can get miscategorized. For example, gensets may get categorized as electric power, even if the unit is for an oil and gas application. Remote mines, offshore platforms, and onshore drilling sites tend not to have ready electricity grid access. Consider this article - http://thebakken.com/articles/685/generators-evolving-with-the-bakken.

Consider Aggreko's end-market mix in North America, which shows about 1/3 of sales to oil & gas and mining. Given CAT's product set and relationships, we would be surprised if it were a smaller part of the mix.

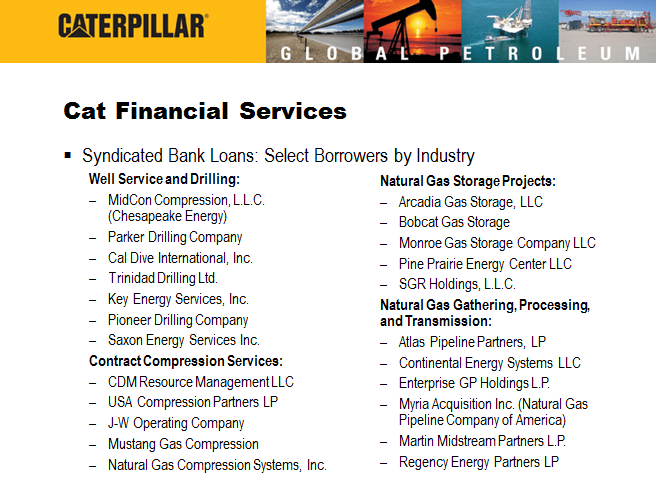

Would You Want These Receivables?

And these are the ones that the company discloses in its mining finance pitch book… We covered this in more detail a couple of weeks ago.

http://cafinance.cat.com/cda/files/3267604/7/Structued%20Finance%20Pitchbook%20012813.pdf

There is also likely to be credit exposure on the oil & gas side. We do not know how big the exposure is today, but in 2009 it was expected to grow to several billion dollars. We would guess that the growth has exceeded those earlier expectations.

https://catoilandgas.cat.com/cda/files/2021600/7/FINANCING%20SOLUTIONS%20FOR%20THE%20PETROLEUM%20INDUSTRY%20%20LESW0017-00.ppt?mode

In terms of exposures circa a few years ago, the drilling and well services names may be troubled, while the compression names look largely okay.

https://catoilandgas.cat.com/cda/files/2021600/7/FINANCING%20SOLUTIONS%20FOR%20THE%20PETROLEUM%20INDUSTRY%20%20LESW0017-00.ppt?mode

CAT is still advertising onshore financing, but we would bet credit standards have tightened just a bit this quarter. Tighter credit is an obvious negative for new equipment sales.

http://finance.cat.com/cda/files/2702016/7/Onshore%20Drilling%20Solutions.pdf

Upshot & Valuation

CAT has high quality products and employees, but has become a bit ‘low quality’ from an investor perspective, we think. There is an S.E.C. review of the company's accounting, some fantastically unfortunate acquisitions, numerous guidance gaffs, and clear strategy issues. We suspect CAT shares will put in a bottom when management is either changed, or does a 180-turn on strategy. If CAT earns, say, $5.00 in 2015, ex-items, and has some of the credit, accounting, management, and strategy issues that we anticipate, a 12x-15x multiple might prove generous. To us, it doesn’t seem unreasonable that the shares could trade in the $60-$75 range (although we do not like a P/E framework), and possibly even lower if it gets messy.

Still, the 2015 guidance we should see when CAT reports on January 26 will likely miss consensus, and we would expect the shares to underperform into that report. It also seems like a short-run cover the news event, but that decision can wait.