Yesterday, stocks suffered their biggest one-day decline since July 2nd. The RECOVERY theme was delivered a blow from a disappointing data point from the manufacturing sector. More importantly, a larger-than-expected jump in initial jobless claims, created some concern about the release of September nonfarm payrolls due out shortly. I would also note that RISK MEASURES were elevated yesterday, with the VIX +10.4%, its biggest one-day spike since September 1st.

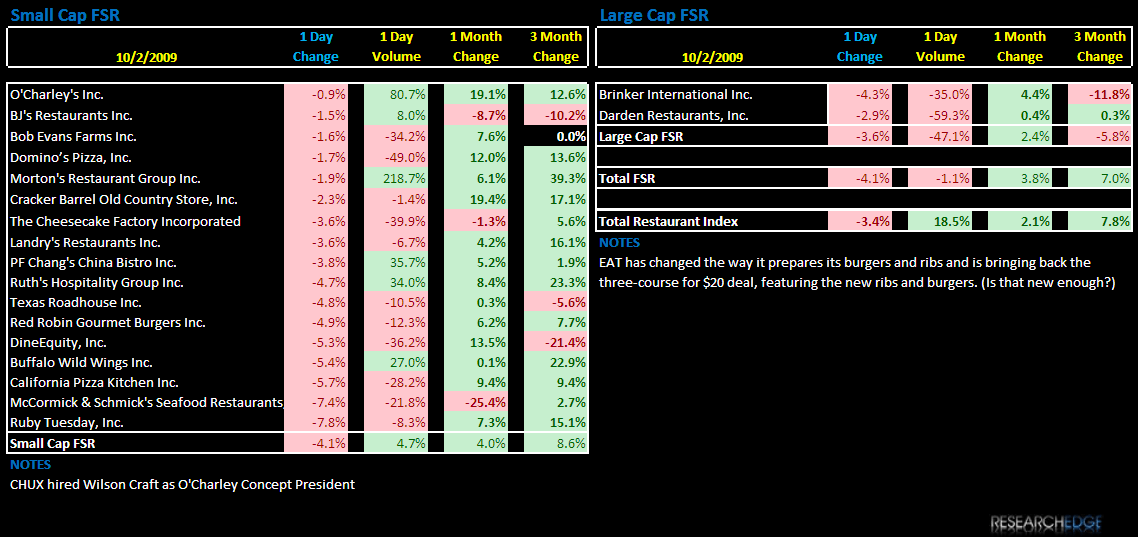

Surprisingly the Consumer Discretionary (XLY) slightly outperformed the S&P 500, despite the jump in initial claims. The RESTAURANTS underperformed the S&P 500 with Full Service (FSR) getting hit the hardest, declining 4.1%. Overall, the decline in the restaurant stocks was on very light volume.