Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

Continuing to highlight Russia, the country's Sberbank CDS continue to drastically widen (+64 bps WoW, +204 bps MoM). The ruble continued to fall alongside the drop in oil prices last week, even with Russia's central bank decision to lift its key interest rate.

Greece re-entered the risk spotlight with banks CDS widening by more than +200 bps; the country's snap presidential election rekindled investor worries about the country's recovery.

European Financial CDS - Swaps mostly widened in Europe last week. The average move was a drastic +14.8%. The only two institutions whose CDS tightened were Portugal's Banco Espirito Santo and the UK's HBOS. HBOS' swaps tightened by only -1 bps. Banco Espiroto Santo's swaps continued to tighten after the December 4 news that the bank was nearing a sale of some of its parts.

Greek bank swaps blew out last week, with CDS widening +216 bps on average, on the announcement of a snap presidential election. The announcement sparked fresh investor fears over how long-lasting and/or effective Greek fiscal reform will be.

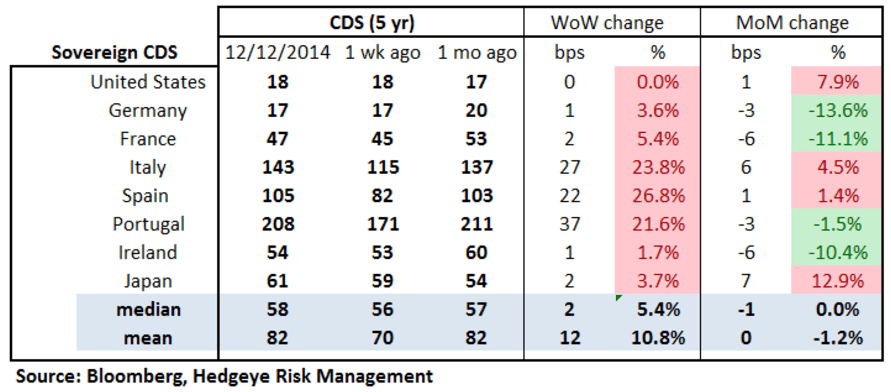

Sovereign CDS – Sovereign swaps widened across the board last week. Spanish sovereign swaps widened by 26.8% (22 bps to 105), while Portuguese swaps widened by 37 bps. The global theme last week was derisking as the Global Dow fell -4.43% and CDS nearly universally widened.

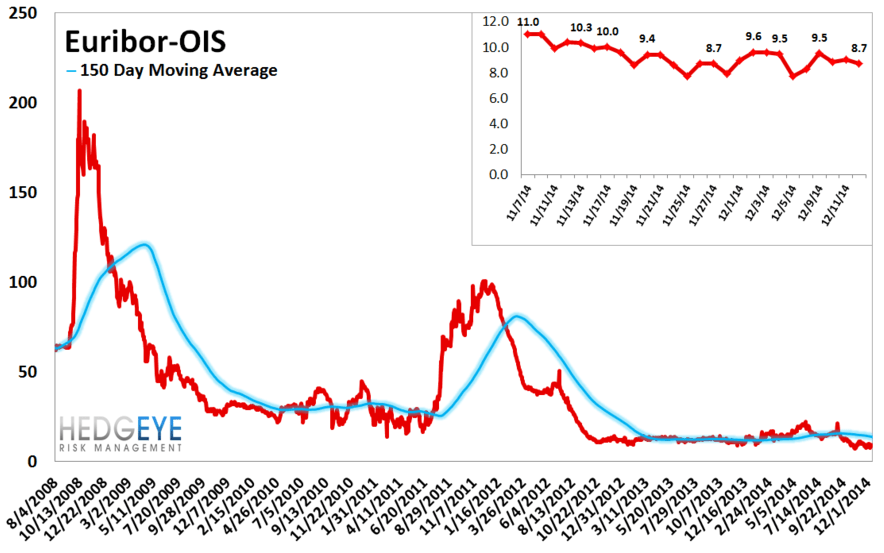

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 9 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst