Current Ideas:

Key Takeaway:

The global theme last week was derisking as the Global Dow fell -4.43% and CDS nearly universally widened. The only positive short-term measure on our heat map below is the falling price of commodities; however, that has recently signaled concerns over global economic slowing. Intermediate-term measures don't look much better, dominated by red.

Continuing to highlight Russia, the country's Sberbank CDS continue to drastically widen (+64 bps WoW, +204 bps MoM). The ruble continued to fall alongside the drop in oil prices last week, even with Russia's central bank decision to lift its key interest rate.

Greece re-entered the risk spotlight with banks CDS widening by more than +200 bps; the country's snap presidential election rekindled investor worries about the country's recovery.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 9 out of 12 worsened / 2 of 12 unchanged

• Intermediate-term(WoW): Negative / 2 of 12 improved / 6 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 3 out of 12 worsened / 7 of 12 unchanged

1. U.S. Financial CDS - Swaps widened for 23 out of 27 domestic financial institutions. Marsh & McLennan was the only institution whose CDS tightened (-5.6% WoW). This continues the intermediate trend; month over month, of all American CDS, MMC's have tightened the most at -11.7%.

Widened the least/ tightened the most WoW: MMC, ALL, TRV

Widened the most WoW: JPM, AGO, HIG

Tightened the most WoW: MMC, ALL, CB

Widened the most MoM: GNW, C, SLM

2. European Financial CDS - Swaps mostly widened in Europe last week. The average move was a drastic +14.8%. The only two institutions whose CDS tightened were Portugal's Banco Espirito Santo and the UK's HBOS. HBOS' swaps tightened by only -1 bps. Banco Espiroto Santo's swaps continued to tighten after the December 4 news that the bank was nearing a sale of some of its parts.

Greek bank swaps blew out last week, with CDS widening +216 bps on average, on the announcement of a snap presidential election. The announcement sparked fresh investor fears over how long-lasting and/or effective Greek fiscal reform will be.

3. Asian Financial CDS continued the global trend of derisking with all CDS in the table below widening. Of note, Chinese inflation figures came in at a five-year low for November.

4. Sovereign CDS – Sovereign swaps widened across the board last week. Spanish sovereign swaps widened by 26.8% (22 bps to 105), while Portuguese swaps widened by 37 bps. The global theme last week was derisking as the Global Dow fell -4.43% and CDS nearly universally widened.

5. High Yield (YTM) Monitor – High Yield rates rose 36.7 bps last week, ending the week at 6.70% versus 6.33% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 29.0 points last week, ending at 1843.

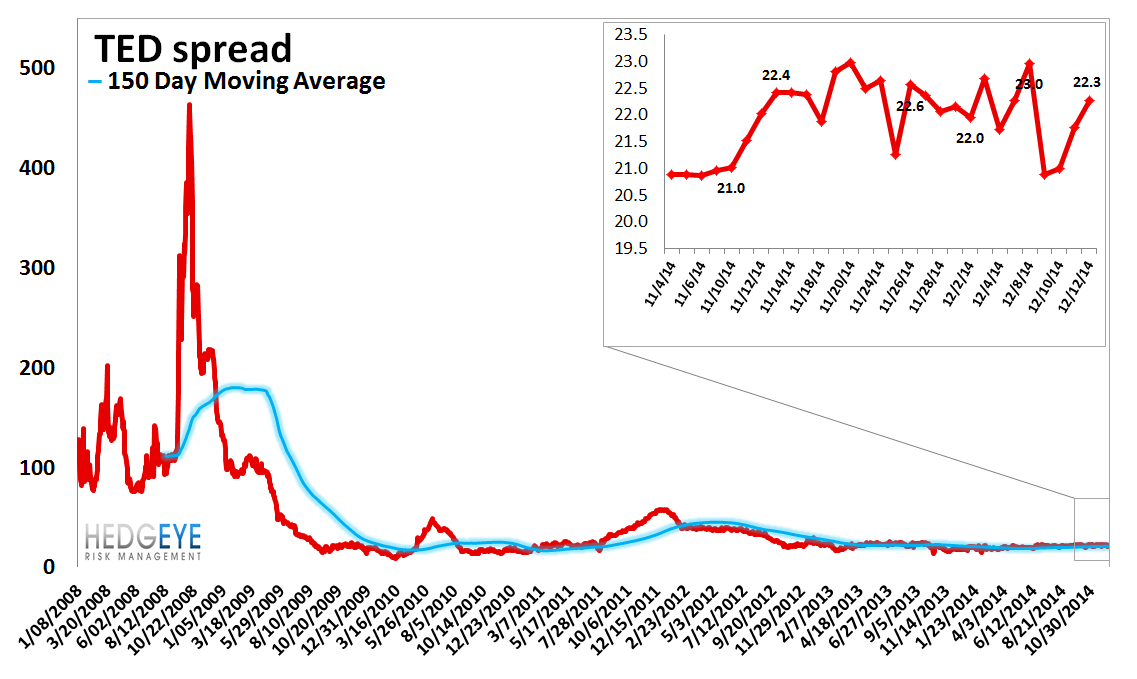

7. TED Spread Monitor – The TED spread was unchanged last week at 22.3 bps.

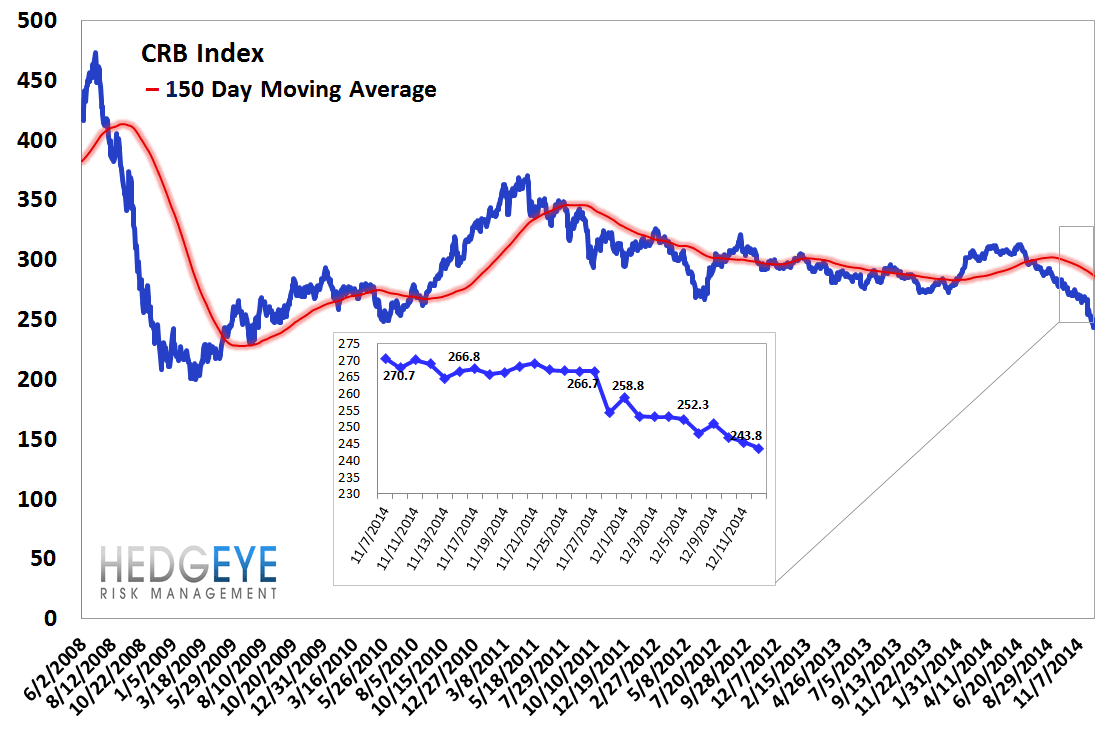

8. CRB Commodity Price Index – The CRB index fell -3.7%, ending the week at 244 versus 253 the prior week. As compared with the prior month, commodity prices have decreased -7.9% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 9 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 2 basis points last week, ending the week at 2.646% versus last week’s print of 2.628%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 1.2% last week, or 36 yuan/ton, to 2879 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

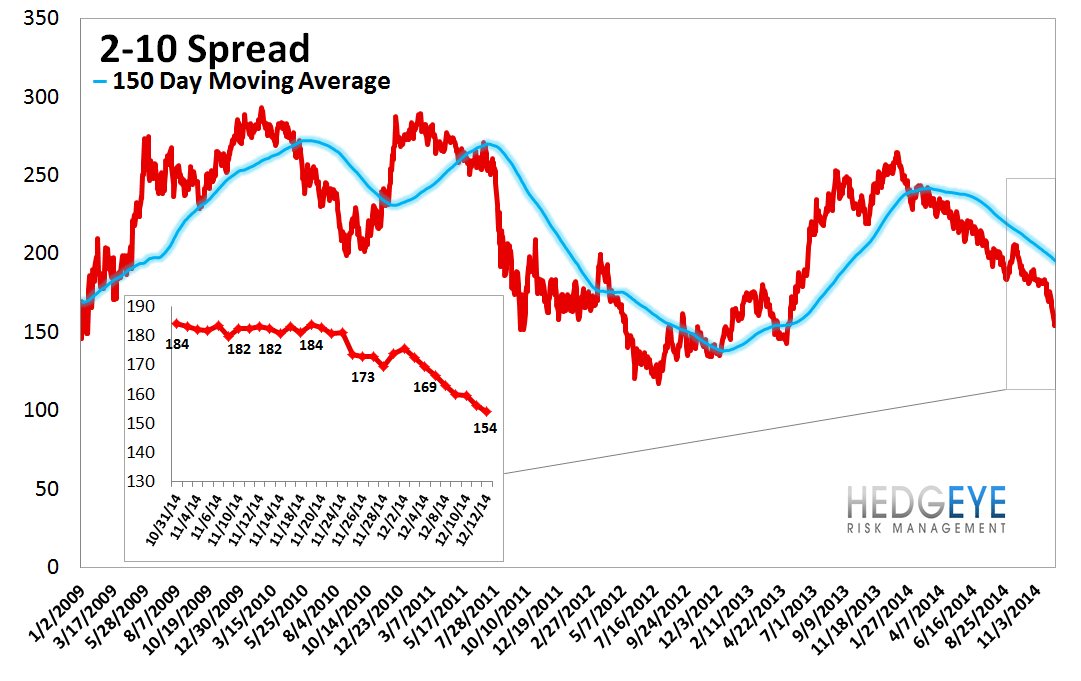

12. 2-10 Spread – Last week the 2-10 spread tightened to 154 bps, -12 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.0% upside to TRADE resistance and 0.5% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT