Our model portfolio is limited to investments in the securities universe. This is by design, since the majority of investors in the US do not actively participate in the futures, physical commodity or spot currency markets and a founding principal of our firm was to make our work accessible and useful to investors of all types. As a result, we deploy our investment ideas in the non-security markets via ETF and ETN products, many of which have structural features that can be non-intuitive. We have recently received a number of inquiries regarding the products that we use to gain exposure to oil as a commodity.

The two most liquid products are the United States Oil Fund, and ETF that trades under the ticker USO, and the iPath Oil ETN, which trades with the symbol OIL.

USO, as an ETF, is a company that holds futures contracts on oil (primarily front month NYMEX and ICE contracts) as well as swaps and treasuries. The fund presents exposure to oil that can be traded like a stock inside a securities account. From a tax perspective, the fact that the company issues k-1 created tax complexities for some holders. OIL, on the other hand, is an Exchange Traded Note that provides a potentially simpler tax scenario for investors, but which also creates credit risk on investors since it is ultimately a debt security issued by a division of Barclays.

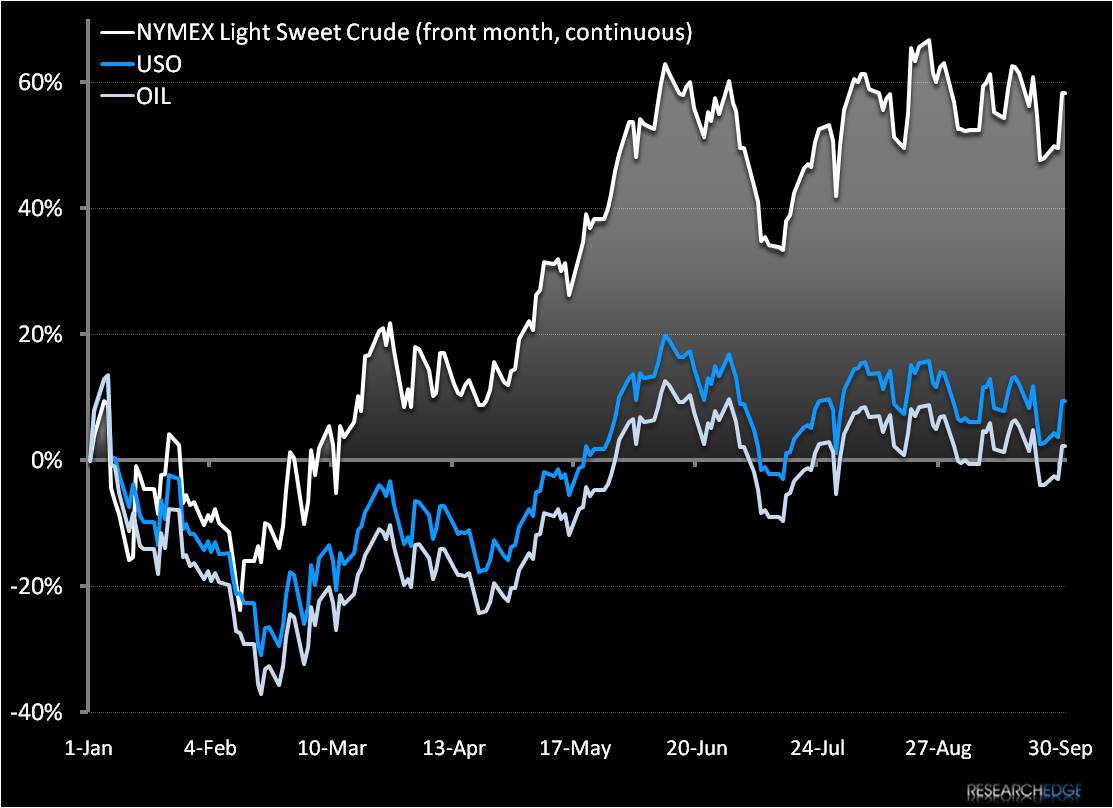

The chart below illustrates how significantly both products have underperformed the continuous front month contract for NYMEX Light Sweet Crude year-to-date --the benchmark they were created to emulate.

This divergence is a result of a structural feature: While the continuous front month contract is calculated hypothetically, both USO and OIL must roll into successive contracts on a monthly basis to replicate the economic exposure. As a result, period of steep contango –such as the market experienced during the start of the year in the wake of collapsing prices, will have a negative impact on USO and OIL as they roll into newer, more expensive contracts. In the charts below we illustrate the steep maturity curve which created a divergence in returns.

As the curve steepness moderated, the products began to trade with a close correlation again with an underperformance factor “baked in” going forward (unless of course the curve inverts, creating positive divergence for holders of USO and OIL).

We strive to provide actionable tactical ideas in our model portfolio and, as such, the liquidity of these products and near term correlation to front month futures makes them the best tools available. For subscribers who execute in non securities markets, either spot, futures or OTC swaps or for those who have a different investment duration than that of our model portfolio, these ETFs and ETNs may not be the best option.

Andrew Barber

Director