Below are Hedgeye analysts’ latest updates on our seven current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*We also feature two pieces of content from our research team at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

Update from macro analyst Darius Dale:

Tales of the Long Bond Pain Trade

Consider the following return figures:

- iShares 20+ Year Treasury Bond ETF (TLT): +2.9% WTD, +3.1% MTD, +8.6% QTD and +24% YTD

- Vanguard Extended Duration Treasury ETF (EDV): +3.9% WTD, +5.1% MTD, +14.2% QTD and +40.8% YTD

- iShares National AMT-Free Muni Bond ETF (MUB): +0.3% WTD, +0.3% MTD, +0.5% QTD and +6.3% YTD

Now consider the most recently reported net speculative position of -214.8k futures and options contracts on 10Y Treasury notes. On a TTM Z-Score basis, that’s the most net SHORT the buy-side has been of the long bond since the week ended March 23rd, 2012.

Source: Bloomberg L.P.

It’s worth mentioning that the long bond rallied hard on that signal; from late-March of 2012 through late-July of that same year, the 10Y Treasury yield plunged -86bps to its all-time closing low of 1.38%.

Source: Bloomberg L.P.

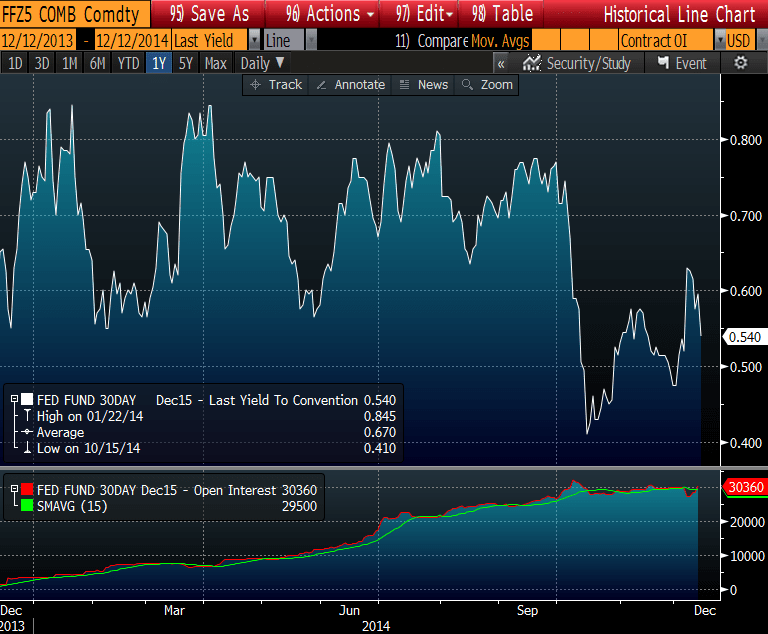

That current setup in the bond market rhymes with investors broadly continuing to anticipate “escape velocity” and a rate “lift-off” over the NTM – even if only a modest tightening: DEC ’15 Fed Funds Futures are pricing in a mere +25bps rate hike by the end of next year.

Source: Bloomberg L.P.

All told, the buy-side hasn’t capitulated on the short side of bonds yet.

They most likely will.

And when they do, you’ll be able to book some nice gains by selling into their mass short-covering – that is, of course, to the extent you’ve been following our recommendation to be long of long-term Treasuries and munis [and defensive equities that resemble this long duration exposure].

HCA

Update from Healthcare sector head Tom Tobin:

I have been watching the sudden and precipitous decline in LINE/LNCO, a favorite short of my energy sector colleague Kevin Kaiser, decline at an accelerating rate in recent months. It’s been a great call and he’s been stating it clearly for well over a year as the stock has declined from the $30s to $12.50 today. Part of the “sudden” decline in LINE/LNCO stock price has been due to the recent ~50% decline in crude oil prices. While it’s great for Kevin’s subscribers (and now admirers) who got out of the way, the current state of affairs was years in the making and the drop in crude oil prices wasn’t the only thing that has gone wrong.

Compliments aside for Kevin’s great work, I am sitting here looking at the companies in my Healthcare universe and feeling alert and scanning for potential problems. My experience has been that when big stuff is happening like a 50% decline across whole categories of market prices, the ripples can be felt in unexpected places. I am wondering what could possibly go wrong, and entertaining (in very small portions) the potential upside. After all, falling crude oil means lower gas prices at the pump and more consumer spending, or at least that is the prevailing wisdom.

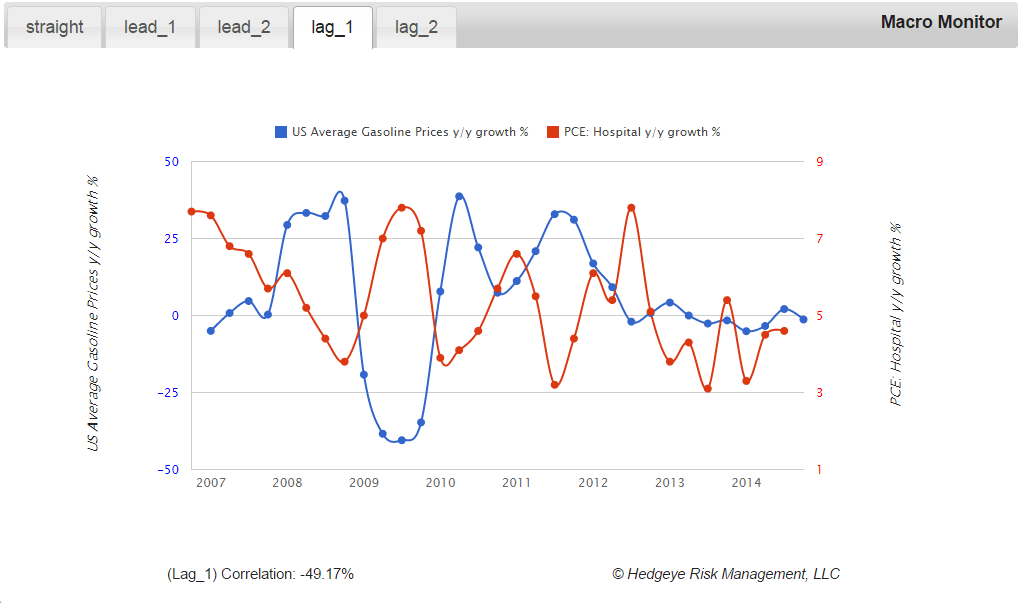

The impact of lower gas prices on Hospital consumption looks as it should, but the overall impact is weak, unfortunately. In the chart below, falling gas prices in one quarter appears to lead to positive growth on Hospital consumption in the next quarter. This is one of many small positives we are considering while we continue to recommend the HCA long position.

On the downside, however, we can see what the market downturn in crude oil and broadly weakening economic growth has had on the cost of corporate borrowing, particularly in the high yield market where HCA borrows it’s significant amount of debt. Borrowing costs in high yield corporate bonds have been creeping higher for several months likely due to concerns of slowing economic growth. While it is not apparent in HCA’s stock price, we can see the impact clearly filtering through to HCA’s bond yields. The relationship is more direct and much stronger than what we are seeing with the gas price chart. We’re not ready to change our positive view on HCA, but this could be the first ripple we are seeing radiate out from the performance problems we are seeing in crude oil and LINE/LNCO.

RH

(Editor's note: In last week's update Retail Sector Head Brian McGough wrote ahead of Restoration Hardware's earnings report released this past week, "This one should be a winner." Well, a winner it was as RH blew past estimates sending shares up approximately 14% for the week. Shares are up 30% since it was added to Investing Ideas, well ahead of the return for the S&P 500. McGough's latest thoughts appear below.)

This RH quarter was almost exactly what we wanted, and was precisely what the stock needed. We said on this week’s RH Flash Call that this is a Binary Quarter, and that when all is said and done there is really only one line that matters – revenue (and we were above consensus by 200bps with an 18% comp). RH has never missed an earnings number, but it missed 2 of the past 3 quarters on the top line. It’d be tough to argue that this is a transformational, ‘once in a generation’ retail story if it consistently misses on the top line.

The company set the record straight this quarter in many ways.

- As it relates to the top line, RH put up a crusher 22% comp vs our 18% estimate. This was a huge ramp from 21% on a 2-year basis in 2Q to 30% in 3Q.

- That includes 31% growth online – a 1,800bp sequential acceleration

- RH threw in an extra 100bp in gross margin expansion above our estimate for +164bps in total. This supports our view that one of the key underappreciated elements of the story is the occupancy leverage from new stores.

- RH also gave more clarity on the long-term margin equation, with a goal of 15-16% vs. 7.8% last year. (Note: we’ve been at 16% for a year). RH had previously alluded to ‘mid teens’ margins, but this time Karen Boone formally and confidently walked through the Gross Margin and SG&A levers that will get there.

This story is far from over.

yum

Both Wall Street and the media have been focused on McDonald’s as the next target of activism in the restaurant space. While it certainly could be, we believe the often overlooked Yum Brands is the more sensible target. Unlike McDonald’s, YUM’s multiple brands and new operating structure can, and should, be altered in a way to create significant shareholder value.

For the better part of the past two years, management has been asked about a potential spinoff of the struggling China business. This could be the first step in a series of potential transactions that would simplify the structure and improve the operating performance of the company. We find it likely that a group of influential shareholders begin to push the board in that direction.

CEO Greg Creed told investors and analysts yesterday that, although he has no current plans to make any structural changes, he would not rule anything out. We believe the intrinsic value of the stock is $90-110/share.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

Housing: moving from bad to decent

Purchase apps have been on the rise for a month now. Evidence continues to emerge that housing is inflecting from bad to decent.

lulu: long (but on a short leash)

We’ll take the market reaction, but this was actually a really lousy quarter – especially considering the pain it is lapping vs last year.